For investors looking for a disciplined, long-term method to assemble a portfolio, few strategies are as respected as Peter Lynch’s approach. As described in his book One Up on Wall Street, Lynch’s thinking focuses on locating companies with good, lasting growth that are available at fair prices, a style often called Growth at a Reasonable Price (GARP). It is a basic, buy-and-hold method that does not try to time the market, concentrating instead on a company’s financial soundness, earnings, and price. The aim is to find businesses that are expanding in a controlled manner, and to keep them as they increase in value over many years.

One company that recently appeared from a filter using Lynch’s main principles is Fluor Corp (NYSE:FLR), a worldwide engineering, procurement, and construction company. Let’s see how FLR compares to the important checks of the Lynch method and what it could provide for long-term investors focused on GARP.

Meeting the Lynch Criteria

The Peter Lynch filter uses particular, number-based checks to find companies with the correct mix of growth, financial soundness, and good price. Based on the given data, Fluor Corp fits these basic needs:

- Sustainable EPS Growth: Lynch looked for companies with a demonstrated growth history, but was cautious of extreme growth that might not continue. The filter needs a 5-year average yearly EPS growth between 15% and 30%. Fluor’s EPS has increased at an average rate of 27.7% over the last five years, putting it well inside this target zone and pointing to a solid historical growth rate.

- Attractive Valuation via PEG Ratio: Possibly the central part of Lynch’s price assessment, the Price/Earnings to Growth (PEG) ratio compares a stock’s P/E ratio to its growth rate. A PEG ratio of 1 or less implies the stock could be fairly priced compared to its growth. Fluor’s PEG ratio, using its past 5-year growth, is 0.73, suggesting its current price may not completely account for its historical earnings growth path.

- Strong Profitability (ROE): Lynch preferred companies that produce high returns on shareholder equity, a signal of effective management and a lasting advantage. The filter requires a Return on Equity (ROE) above 15%. Fluor’s ROE of 65.3% is very high, well beyond the minimum requirement and indicating strong earnings from its equity.

- Conservative Financial Health: To limit risk, Lynch stressed companies with good balance sheets. The filter includes two important health tests:

- Debt/Equity < 0.6: Fluor’s Debt/Equity ratio of 0.21 shows a very careful capital structure, with funding relying more on equity than debt. Lynch himself liked a ratio under 0.25, which FLR meets.

- Current Ratio >= 1: This tests short-term liquidity. Fluor’s Current Ratio of 1.45 shows it has enough current assets to meet its upcoming liabilities, offering a safety buffer.

A Look at the Broader Fundamental Picture

While the Lynch filter gives a solid initial check, a closer look at the company’s full fundamentals is important. According to Fluor’s detailed fundamental analysis report, the view is balanced but has clear positives matching a value-aware growth strategy.

The report gives FLR a neutral total score, noting both positive points and areas for watchfulness. On the good side, Fluor’s earnings measures, like Return on Assets and Profit Margin, are some of the top in its Construction & Engineering industry. Its financial health is also seen positively, with the low Debt/Equity ratio and good liquidity measures doing better than many industry competitors.

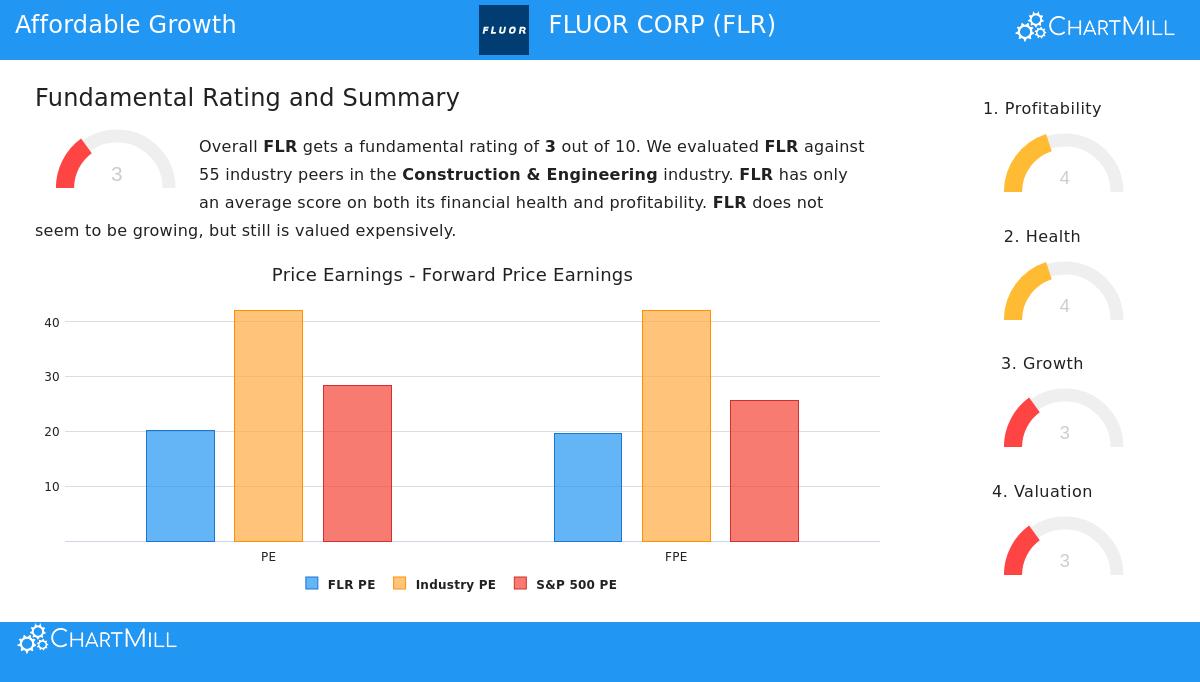

The main points of attention are in price and recent growth. The report states that based on its absolute P/E and Forward P/E ratios, FLR seems "rather expensive," though it is still priced lower than most of its industry. Also, the company has seen a drop in both earnings per share and revenue over the last year, a pattern investors will want to examine to see if it is a short-term pause or a more lasting concern.

Is Fluor Corp a Lynch-Style Investment?

Fluor Corp offers an interesting example for the Peter Lynch method. It satisfies the number-based filter very well, displaying the specific mix of high historical growth, excellent profitability (ROE), careful debt, and a good PEG ratio that Lynch supported. The company works in the necessary, if sometimes "ordinary," areas of infrastructure, energy, and government services, exactly the kind of understandable business Lynch told investors to find.

However, the Lynch method is not only about using a filter. It needs knowing the business behind the figures. The recent drops in EPS and revenue, as mentioned in the fundamental report, require careful study. An investor must evaluate if these are routine pressures in Fluor’s project-based operations or signals of a more serious issue. The high ROE and strong industry-relative price, however, imply the market may already be accounting for some of these current difficulties.

For investors who think Fluor’s central engineering and construction businesses are lasting and its present projects will lead to renewed growth, the stock represents a standard GARP chance: a historically solid grower with a strong balance sheet, available at a price that allows for its recent slowdowns.

Interested in seeing other companies that fit this disciplined growth method? You can find the full list of stocks passing the current Peter Lynch filter here.

Disclaimer: This article is for information only and does not form financial advice, a suggestion, or an offer to buy or sell any security. The Peter Lynch method is one of many investment approaches, and past results of a filtering technique do not guarantee future outcomes. Investors should do their own complete research and think about their personal financial position and risk comfort before making any investment choices.