For investors looking for a dependable source of passive income, a methodical screening process is needed to distinguish solid dividend payers from possible value traps. A frequent method uses filters for companies that provide a good dividend now and also have the basic financial capacity to maintain and increase those payments in the future. This usually requires examining more than just the current yield to evaluate earnings, balance sheet condition, and the payment's own sustainability. Using this kind of multi-factor filter, investors can create a list of prospects that mix income production with basic quality.

One company that emerges from this kind of review is East West Bancorp Inc (NASDAQ:EWBC), the California-based bank holding company. The stock is found by a filter set up to find high-quality dividend stocks by needing a high ChartMill Dividend Rating, along with at least satisfactory scores for earnings and balance sheet condition. This pairing seeks to find companies where the dividend is backed by a sound business, not just a high yield caused by a low stock price.

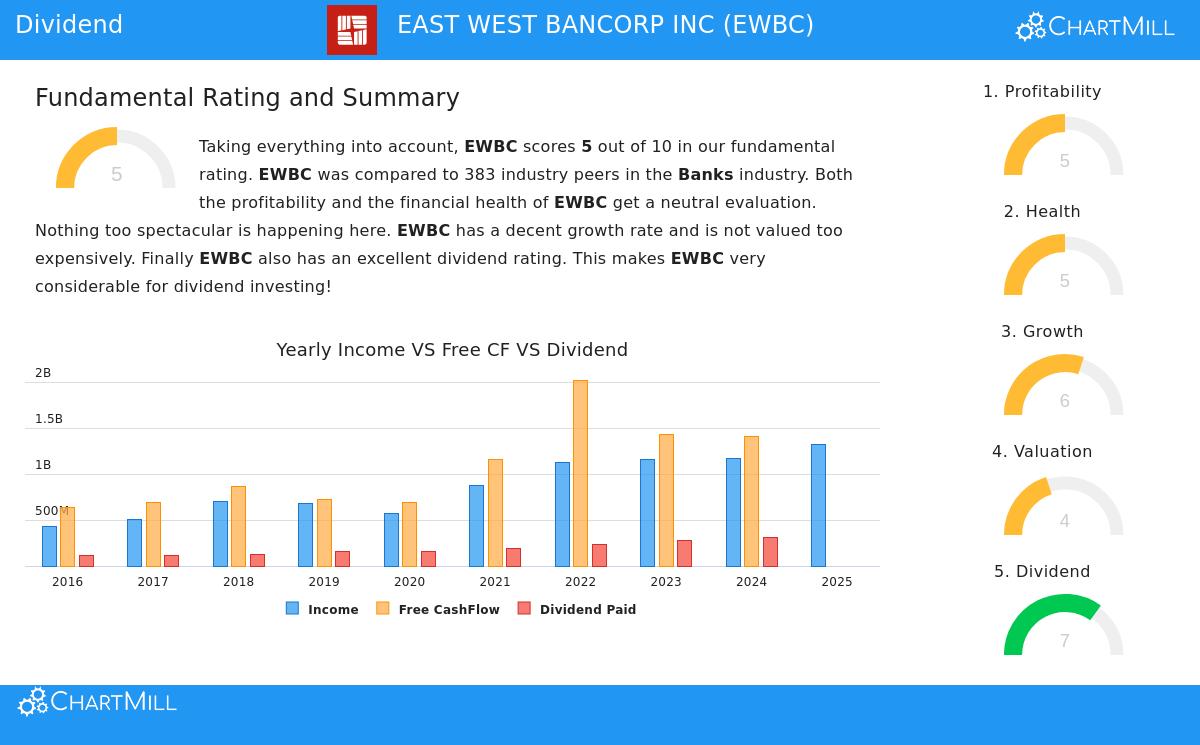

Dividend Strength and Sustainability

The main attraction for income investors is in EWBC's dividend characteristics, which receive a good rating of 7 out of 10. The review shows several favorable points that match a long-term dividend investment plan.

- Dependable History: The company has paid and, importantly, has not reduced its dividend for at least ten years. This record of consistency offers some assurance of management's focus on giving capital back to shareholders.

- Notable Increase: The dividend is rising at a good yearly rate of about 15.76% over the last five years, greatly exceeding inflation and improving the income for long-term owners.

- Maintainable Payment: A crucial measure for dividend security is the payout ratio. EWBC uses only about 26% of its earnings for dividend payments, seen as a low and very maintainable amount. This gives plenty of capacity to put money back into the business, handle economic slowdowns, and keep increasing the dividend.

Still, a point of attention from the basic report shows that EWBC's earnings are now increasing more slowly than its dividend. While the payout ratio stays low, this situation needs watching to confirm the high increase rate can continue without pressuring finances.

Supporting Basics: Earnings and Condition

A maintainable dividend needs a profitable and financially stable business. This is why the filter conditions require satisfactory ratings in these areas, and EWBC meets this with a score of 5 for both Earnings and Balance Sheet Condition.

Earnings (Rating: 5) The bank shows solid profit generation. Its Return on Equity (ROE) of 14.70% and Return on Assets (ROA) of 1.58% are some of the top in its industry, doing better than over 90% of banking peers. Also, its profit margin of over 44% is very good. These numbers show that EWBC is effectively creating profits from its assets and equity, which is the final source of dividend money.

Balance Sheet Condition (Rating: 5) The balance sheet review shows a careful method to debt. EWBC's Debt/Equity ratio is a very small 0.01, and its Debt to Free Cash Flow ratio is a very good 0.08, meaning it could pay off all its debt in a short time using its cash flow. These numbers, which do better than a big majority of industry peers, indicate high solvency and low financial risk. This stable base is important for a dividend stock, as it gives a cushion during economic strain when earnings could be challenged.

Valuation and Increase Background

With a combined basic rating of 5, EWBC shows a varied but fair view. Its valuation gets a 4, mainly because of its very sensible Price-to-Earnings (P/E) ratio of 11.89 and Forward P/E of 10.96. These ratios match the banking industry but are much lower than the wider S&P 500 average, indicating the stock is not priced too high.

Increase gets a score of 6, backed by a good past record in both Earnings Per Share and Revenue. Looking forward, while EPS increase is predicted to slow, revenue increase forecasts stay sound. This overall increase picture supports the possibility of ongoing dividend raises.

A Prospect for More Review

For dividend-centered investors, East West Bancorp Inc. offers a strong example of how a filter system can find quality prospects. It mixes a good, increasing dividend with a low payout ratio, supported by strong industry-leading earnings and a very stable, low-debt balance sheet. The valuation seems fair, giving a safety buffer not always present in high-yield companies.

It is necessary to do complete personal research beyond the ratings. Investors should think about the bank's specific loan portfolio, exposure to economic cycles, and interest rate setting. The full ChartMill Fundamental Analysis Report for EWBC gives a complete look at all these points and is a good first step for more detailed research.

EWBC was found using a particular dividend stock filter. If you want to review other companies that meet similar conditions of high dividend quality, satisfactory earnings, and balance sheet condition, you can use the "Best Dividend Stocks" filter yourself to see the complete list of present results.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investing has risk, including the possible loss of principal. You should do your own research and talk with a qualified financial advisor before making any investment choices.