The investment philosophy of Peter Lynch, famously detailed in his book One Up on Wall Street, centers on identifying companies with strong, sustainable growth that are trading at reasonable valuations. This method, often called Growth at a Reasonable Price (GARP), avoids the extremes of speculative high-growth bets and deep-value turnarounds. Instead, it looks for established, profitable businesses with a clear growth path that the market may be undervaluing. A central tool for this method is the PEG ratio, which compares a stock's price-to-earnings (P/E) ratio to its earnings growth rate, aiming for a value of 1 or less to point to a possibly attractive valuation.

ENPHASE ENERGY INC (NASDAQ:ENPH) appears from a screen based on Lynch's criteria, presenting a case for long-term GARP investors. The company designs and manufactures integrated microinverter-based solar and battery systems, providing intelligent energy management for homes. Its technology exists where renewable energy adoption and home electrification meet, long-term trends that support its business model.

Meeting the Lynch Criteria

A Peter Lynch screen filters for companies with a specific mix of growth, financial health, profitability, and value. Enphase Energy's key metrics align closely with these ideas:

- Sustainable Growth: Lynch preferred earnings growth between 15% and 30% each year, seeing it as sustainable. Enphase's Earnings Per Share (EPS) has grown at an average rate of 20.06% over the past five years, placing it inside this target range. This shows a history of solid, but not excessive, increase.

- Attractive Valuation via PEG: The central part of the GARP method is the PEG ratio. Enphase's PEG ratio, based on its past five-year growth, is 0.61. A number below 1 implies the stock's price may not fully account for its historical earnings growth, a main signal for value-minded growth investors.

- Strong Profitability: Return on Equity (ROE) measures how well a company creates profits from shareholder equity. Lynch looked for ROE above 15%. Enphase's ROE of 19.66% is above this level, pointing to effective management and a profitable business.

- Financial Health: Lynch stressed a strong balance sheet.

- The Debt-to-Equity ratio of 0.57 is below the screen's upper limit of 0.6, showing a moderate use of debt. Lynch himself liked an even lower ratio, but this level indicates the company is not overly indebted.

- The Current Ratio of 2.04 shows the company has more than twice the current assets required to cover its short-term debts, indicating good liquidity and financial strength.

Fundamental Health Check

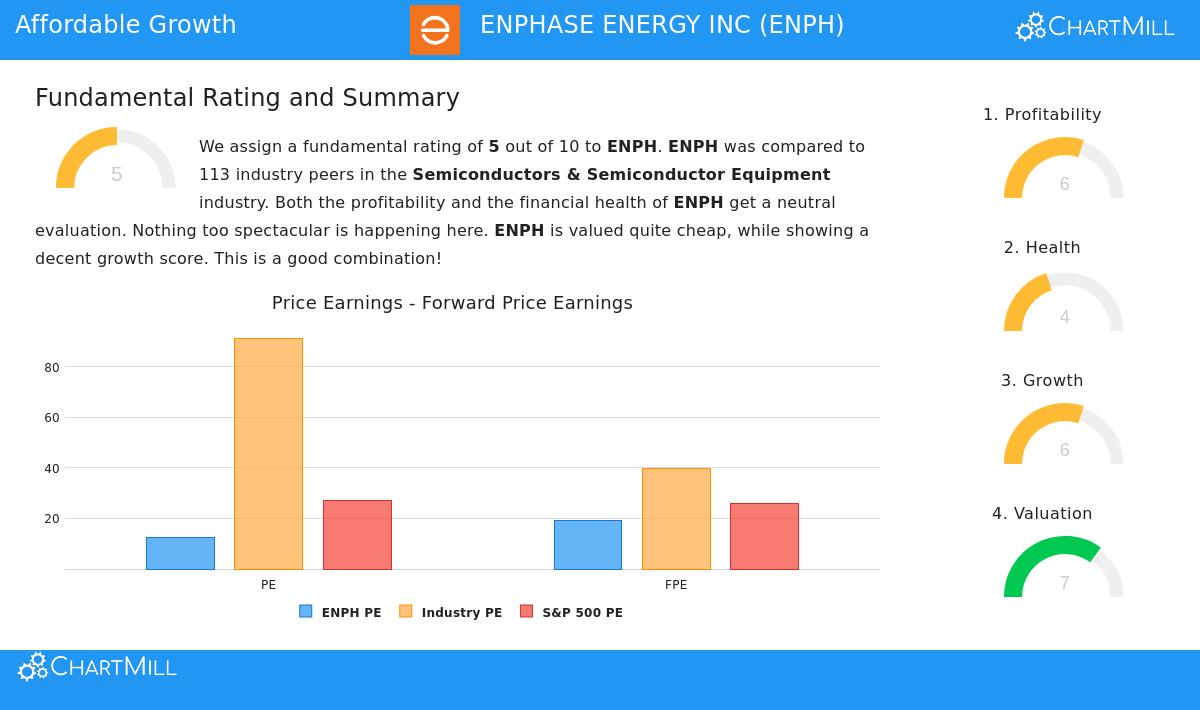

A wider view of Enphase's fundamental profile, as detailed in its analysis report, provides a mixed but generally supportive picture. The company receives an overall fundamental rating of 5 out of 10, which is average compared to others in the Semiconductors & Semiconductor Equipment industry.

Strengths are clear in its growth and valuation metrics. The company has shown very strong past growth in both revenue and earnings. From a valuation viewpoint, its standard P/E ratio of 12.29 is seen as low relative to both the industry and the wider S&P 500. Profitability ratios like Return on Assets and Return on Invested Capital also score well within the industry.

Areas for investor attention include financial health and future growth expectations. The health score is a 4, with notes that the Debt-to-Equity ratio is not as good as many industry peers and the Altman-Z score points to limited, but present, bankruptcy risk. Also, while past growth has been notable, analysts expect a large slowdown in both revenue and earnings growth for the coming years. This forward-looking decrease is an important factor for any growth-focused method and needs careful thought.

Is Enphase a Lynch-Style Investment?

For an investor using Peter Lynch's ideas, Enphase Energy presents a strong profile. It works in a concrete, understandable area—home energy solutions—that fits with Lynch's "invest in what you know" principle. The company meets the quantitative filters for sustainable historical growth, reasonable valuation (as shown by the low PEG ratio), good profitability, and acceptable financial health.

However, the Lynch method is not only mechanical. The screen gives a beginning point for more study. The central question for a long-term holder is whether the company's competitive strengths in microinverter and home energy system technology can protect its market position and maintain a new period of growth, even if at a more measured speed than the large gains of recent years. The expected slowdown points to the need to evaluate the sustainability of the business model, which is core to Lynch's philosophy.

Interested in finding other companies that fit this disciplined growth-and-value method? You can find the full list of stocks passing the current Peter Lynch screen here.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.