For investors aiming to assemble a portfolio of durable, long-term holdings, the ideas of quality investing offer a useful framework. This method centers on finding companies with lasting competitive strengths, reliable and steady profitability, sound finances, and the capacity to produce increasing returns on capital. The "Caviar Cruise" stock screening system turns these ideas into measurable filters, aiding investors in sorting the market for businesses that are not only profitable, but also exceptionally well-managed and financially healthy. The system stresses historical revenue and profit increase, high returns on invested capital, good free cash flow conversion, and a reasonable amount of debt.

One company that now meets this strict screening process is DARDEN RESTAURANTS INC (NYSE:DRI), the parent company of well-known full-service dining brands such as Olive Garden and LongHorn Steakhouse. We can look at how Darden fits with the main points of the Caviar Cruise method.

Matching the Main Quality Filters

The Caviar Cruise system uses several basic filters to find quality. Darden's financial picture shows it meets or passes these important levels:

- Revenue and Profit Increase: The system needs a minimum 5% compound annual growth rate (CAGR) for both revenue and EBIT (earnings before interest and taxes) over five years. Darden does well here, with a 5.76% revenue CAGR and a solid 26.36% EBIT CAGR. Also, a central point of the method is that EBIT increase should be greater than revenue increase, pointing to better operational efficiency and possible pricing ability. Darden's clear passing on this measure is a good sign.

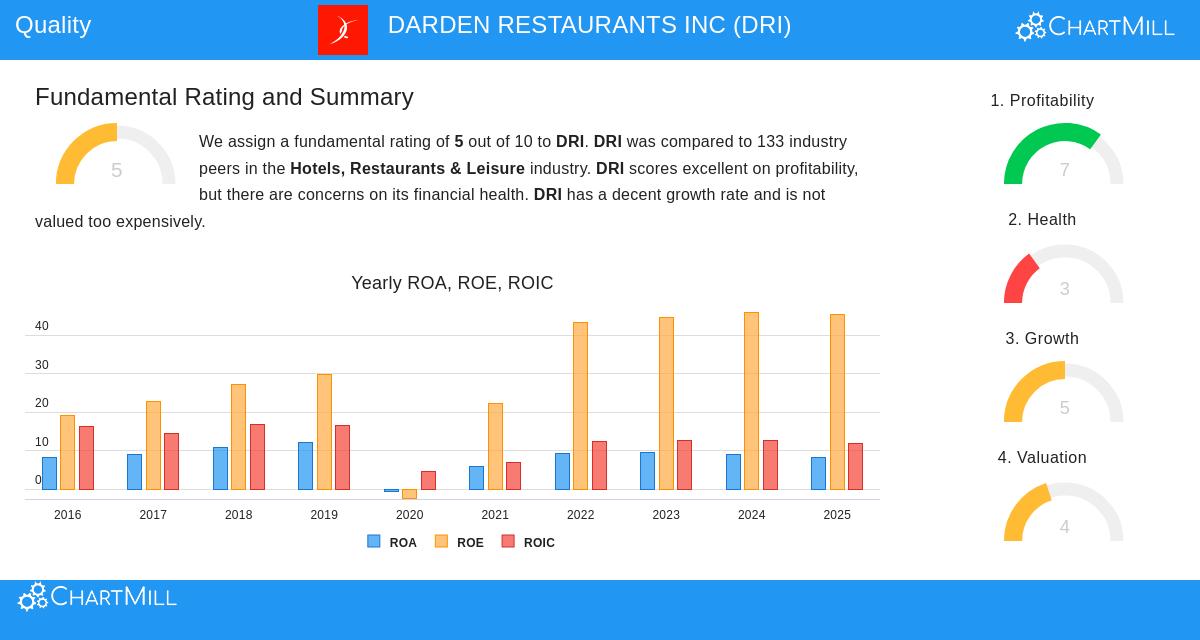

- High Return on Capital: A return on invested capital (ROIC) over 15% is a sign of a quality company, showing management's ability to use capital profitably. The system uses a form that leaves out cash, goodwill, and intangibles to look at central operations. Darden's ROIC on this basis is a good 17.20%, easily passing the requirement and indicating the company produces real economic value.

- Good Cash Flow and Reasonable Debt: Quality companies change accounting profits into real cash and are not weighed down by debt. The system looks for a Debt-to-Free Cash Flow ratio under 5, meaning all debt could be paid off with less than five years of current cash flow. Darden's ratio of 4.42 is within this acceptable area. Also, its five-year average Profit Quality, which measures how much net income changes to free cash flow, is a very good 105.36%, much higher than the 75% minimum. This shows earnings are high-quality and supported by cash.

Basic Health and Valuation Setting

A wider view of Darden's basics gives setting. According to its detailed basic analysis report, the company shows a mixed but generally healthy picture, in line with a mature, cash-producing business.

Strengths are clear in profitability and increase:

- The company has very good returns on equity and assets, doing better than most others in its industry.

- It has a steady history of yearly profitability and positive operating cash flow.

- Past increase in both earnings per share and revenue has been good.

Important points for investors to note include:

- Financial Health: The report notes questions about liquidity, with low current and quick ratios. This is usual in the restaurant industry because of inventory and payables cycles but needs watching. Solvency measures are more neutral, with a Debt-to-Equity ratio that is high in simple terms but similar to others.

- Valuation: Darden's stock is not seen as low-cost in simple terms, but it seems fairly valued compared to both its industry and the wider S&P 500. The dividend yield is appealing, though the report states the payout ratio could be nearing levels that are hard to maintain if earnings increase slows.

- Future Increase: Analysts expect a slowing in increase rates for both revenue and earnings compared to the past five years, which is normal as companies become mature.

Is Darden a "Caviar Cruise" Choice?

For a quality investor, Darden Restaurants displays many of the wanted traits. It runs settled, familiar brands in a stable industry. Its finances show a company that has increased profitably, produces significant free cash flow, and earns a good return on its capital, all central goals of the Caviar Cruise system. The ability to steadily change profits into cash (as seen by its 105% Profit Quality) is especially interesting, as it gives options for dividends, debt payment, or new investment.

Yet, the quality investing view also includes judging less measurable factors and long-term strength. Investors would need to judge Darden's competitive place facing shifting dining trends, its pricing ability in a time of inflation, and the performance of its multi-brand plan. The system finds a financially sound company; the investor's task is to determine if it also has the lasting competitive strengths needed for a very long-term holding.

The Caviar Cruise system can aid investors in finding other companies that have these quality features. You can see the current system results and method here.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investing has risk, including the possible loss of the amount invested. You should do your own research and talk with a qualified financial advisor before making any investment choices.