Investors looking for a disciplined, long-term method for choosing stocks frequently consider the ideas from legendary fund manager Peter Lynch. His method, explained in his book One Up on Wall Street, centers on finding expanding companies available at sensible prices, a concept often called Growth at a Reasonable Price (GARP). Lynch supported a fundamental, buy-and-hold method, highlighting lasting earnings expansion, sound financial condition, and appealing valuation measures like the PEG ratio. A filter using these central ideas recently highlighted a significant possibility in the metals and mining field: DRDGOLD LTD-SPONSORED ADR (NYSE:DRD).

Fit with Peter Lynch's Main Requirements

The Peter Lynch filter looks for companies that display a particular mix of expansion, value, and financial soundness. DRDGOLD seems to satisfy these strict requirements according to the given information, placing it as a possible choice for GARP-oriented investors.

- Lasting Earnings Expansion: A central part of Lynch's method is a steady and lasting expansion rate in earnings per share (EPS). He preferred companies expanding between 15% and 30% each year, as expansion above that can be hard to continue. DRDGOLD's five-year average EPS expansion of 26.15% sits directly within this desired range, showing a solid and possibly lasting upward path in earnings.

- Appealing Valuation Using PEG Ratio: Lynch was known for using the Price/Earnings to Growth (PEG) ratio to locate sensibly priced expanding stocks. A PEG ratio at or under 1 implies the stock's price may not completely account for its expansion potential. With a PEG ratio of 0.58, DRDGOLD is available at a notable discount to its past expansion rate, a main indicator for value-aware expansion investors.

- Outstanding Profitability (ROE): Return on Equity (ROE) calculates how well a company produces earnings from shareholder equity. Lynch wanted high ROE as a mark of a good business. DRDGOLD's ROE of 36.17% is outstanding, showing very efficient use of capital and solid competitive strengths in its field.

- Sound Financial Condition: Lynch required companies with firm balance sheets to endure economic declines. Two important measures here are the Debt-to-Equity and Current Ratios.

- The Debt-to-Equity ratio of ~0.001 is very low, indicating the company is financed almost completely by equity with very little debt load, matching Lynch's liking for careful financing.

- A Current Ratio over 1 shows enough short-term assets to meet short-term obligations. DRDGOLD's ratio of 2.28 shows solid liquidity and financial strength.

Fundamental Review Summary

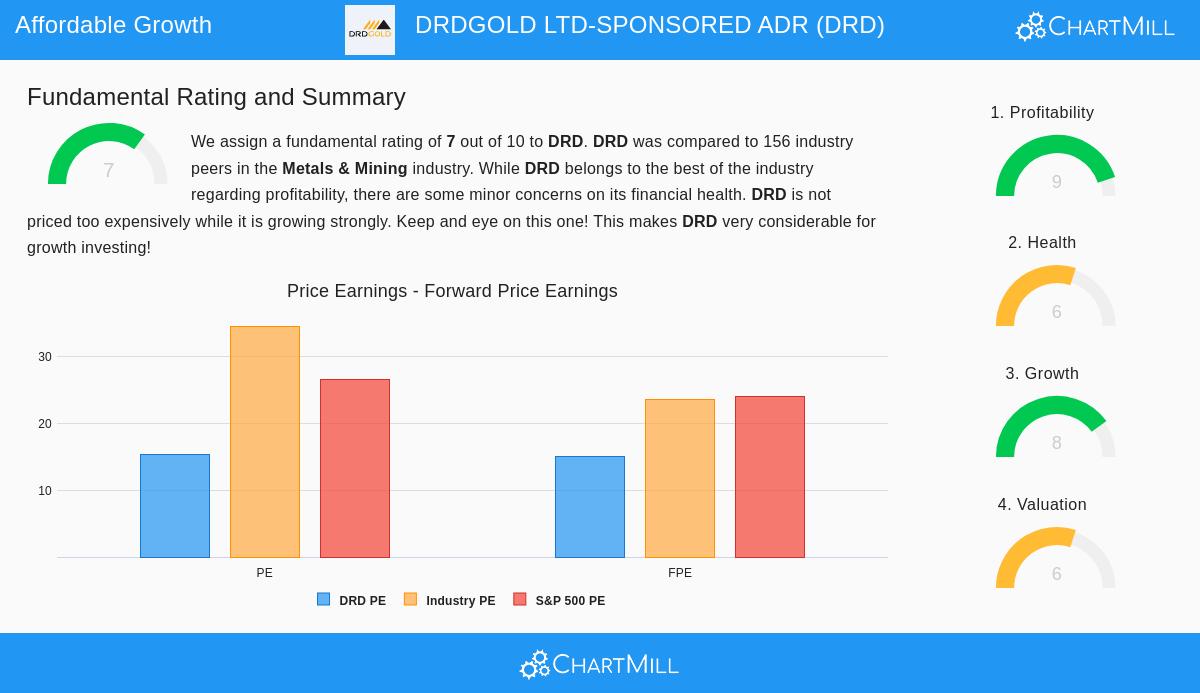

A closer examination of the full fundamental report for DRDGOLD supports the image shown by the filter. The company receives a solid total fundamental score of 7 out of 10.

- Profitability is a definite positive, scoring a 9 out of 10. The company performs well in main margin and return measures, including Profit Margin (27.51%), Return on Assets (26.24%), and Return on Invested Capital (26.85%), each placed in the high end of its field.

- Valuation seems sensible, scoring a 6 out of 10. While its P/E ratio of 15.30 is viewed as fair on its own, it is noticeably less expensive than 92% of its field rivals. The low PEG ratio further backs the argument for an appealing valuation compared to its expansion.

- Expansion measures are persuasive, with a score of 8 out of 10. The company has shown solid recent expansion in both EPS and Revenue, and analysts expect this good trend to carry on.

- Financial Condition is acceptable, scoring a 6 out of 10. The excellent debt situation and good liquidity are benefits, although the report mentions a past rise in shares outstanding over a five-year span, which is a small point for review for long-term shareholders.

You can examine the complete, itemized fundamental review for DRDGOLD here.

Investment Points and Setting

While the numerical filters match well, Peter Lynch also stressed qualitative knowledge. DRDGOLD's operation, the reprocessing of surface gold tailings in South Africa, is a specific activity. Investors should think about the natural parts of this model, including connection to gold prices, working risks in mining, and local political factors. The company's specialty concentrates on removing value from existing waste materials, which can be a low-cost and environmentally mindful way to produce gold, but its results stay linked to the commodity cycle.

For investors who have done their own study and are accepting of the business model, the numerical argument constructed on Lynch's ideas is notable. The mix of high profitability, solid expansion, a clean balance sheet, and a sensible valuation forms a clear investment case for a long-term portfolio.

Find Additional Possible Choices

DRDGOLD was found using a particular filter based on Peter Lynch's method. Investors curious about locating other companies that satisfy comparable requirements for lasting expansion at sensible prices can examine the filter personally. You can see the present outcomes and modify the settings of the Peter Lynch method filter here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. The analysis is based on data provided and a specific investment strategy filter. Investors should conduct their own due diligence and consider their individual financial circumstances and risk tolerance before making any investment decisions.