Investors looking for a disciplined, long-term method for choosing stocks frequently use the ideas of famous fund manager Peter Lynch. His approach, outlined in his book One Up on Wall Street, centers on finding companies with good, lasting growth that are available at fair prices, a thinking often called Growth at a Reasonable Price (GARP). The heart of the method uses fundamental analysis, preferring companies with sound profitability, firm financials, and a simple business model an investor can grasp. The aim is not to follow the most popular trends, but to create a varied collection of good companies that can increase returns over many years.

One company that recently appeared from a filter using Lynch's rules is DRDGOLD LTD-SPONSORED ADR (NYSE:DRD). The South African company works in the metals and mining industry, focusing on the retreatment of surface gold tailings. This means removing gold from old mining waste materials, a process that can be viewed as both good for the environment and steady in operation. For an investor using Lynch's style, this matches the concept of putting money into a business that is easy to understand, even if it works in an area not usually linked with fast, attention-getting growth.

Matching the Lynch Rules

A Peter Lynch filter usually looks for companies showing a particular mix of growth, value, and financial soundness. DRDGOLD's basic numbers match these points closely, giving a numerical reason for its review.

- Lasting Earnings Growth: Lynch preferred companies with good but not extreme growth, which is more probable to continue. The filter asks for a 5-year Earnings Per Share (EPS) growth rate between 15% and 30%. DRDGOLD's EPS has increased at an average yearly rate of 26.15% over this time, putting it well inside this target range. This shows a record of solid, yet possibly maintainable, profit growth.

- Fair Valuation (PEG Ratio): Maybe the most important Lynch number is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks that might be priced low compared to their growth path. Lynch wanted a PEG of 1 or lower. DRDGOLD's PEG ratio, using its past 5-year growth, is 0.74. This indicates the market may not completely account for the company's past growth, a main sign for investors focused on value and growth.

- Good Profitability (ROE): Return on Equity (ROE) calculates how well a company creates profits from shareholder equity. Lynch looked for companies with an ROE above 15%. DRDGOLD's ROE of 25.25% is very high, showing very capable management and a strong profit-making business model.

- Financial Soundness (Debt & Liquidity): A careful balance sheet is critical for long-term strength. The filter requires a Debt/Equity ratio below 0.6 and a Current Ratio above 1. DRDGOLD does very well here, with a Debt/Equity ratio of nearly 0.00, meaning it works with almost no debt. Its Current Ratio of 2.28 indicates more than enough cash to meet near-term needs, giving a good cushion of safety.

Basic Financial Review

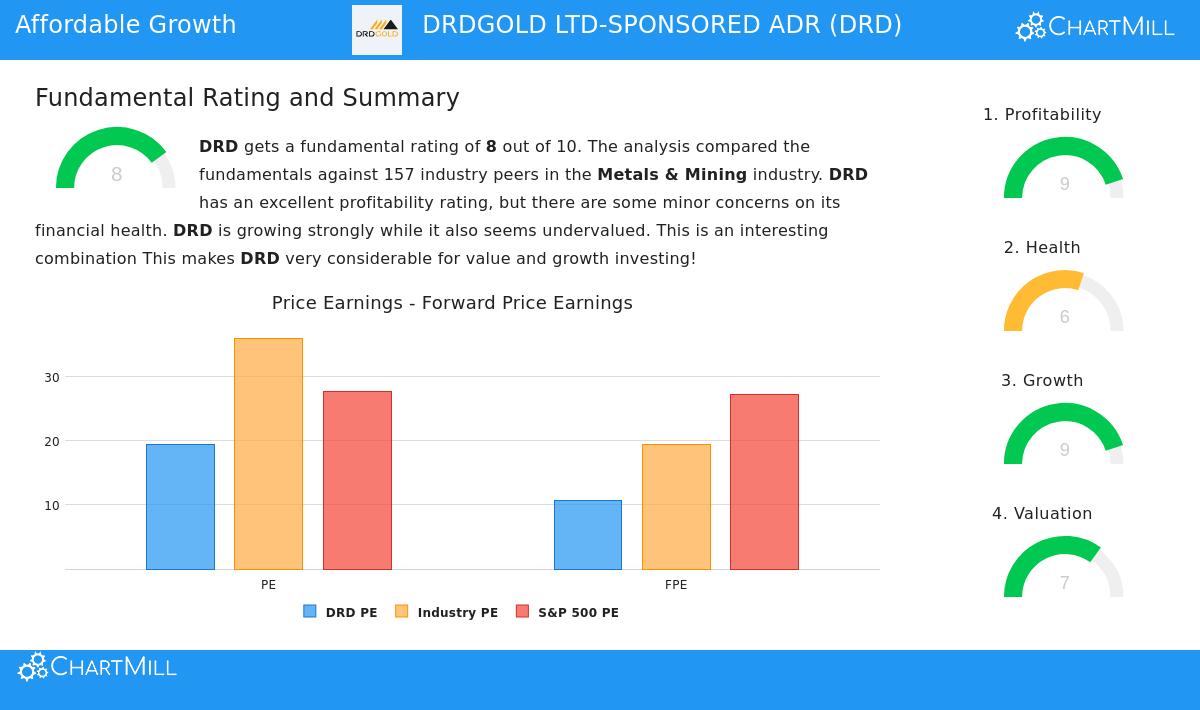

A wider view of DRDGOLD's basic financial picture supports the image shown by the Lynch filter. The company's total basic financial score is a good 8 out of 10. The details show clear strong points:

- Profitability is a key strong point, scoring 9/10. The company has excellent margins and returns (ROE, ROIC) that place it among the best in its field. Its profit and operating margins have gotten steadily better.

- Growth is also very good, scoring 9/10. Besides its strong past EPS growth, sales have also grown at a good double-digit rate. It is important to note, analysts predict a faster pace, with future EPS growth estimated to average above 50% each year.

- Valuation shows a varied but positive image, scoring 7/10. While its standard P/E ratio seems high, its forward P/E and, most significantly, its low PEG ratio indicate the stock is fairly priced, particularly when measured against both industry competitors and the wider S&P 500.

The main point to watch is financial health, which scores a 6/10. While the company's ability to pay debts is outstanding because of its minimal debt and good cash flow, the score is lowered by a past rise in shares available over a five-year span.

For a complete look at these numbers, you can examine the full fundamental analysis report for DRDGOLD.

A Prospect for the Long-Term Collection

For an investor following Peter Lynch's thinking, DRDGOLD offers a strong example. It runs a clear business, recovering gold from existing waste, that produces high returns on equity and works with a very strong balance sheet. Its growth has been significant but within the limits Lynch saw as maintainable, and it now trades at a price that pays investors for that growth, as shown by its below-1 PEG ratio.

While the company's dividend payment is small and its history of shares available needs watching, its main operational strong points match closely with the ideas of looking for quality growth at a fair price. It represents the kind of company a long-term, buy-and-hold investor might study more after it comes from a strict filtering process.

Interested in discovering other companies that match the Peter Lynch investment method? You can use the filter yourself and view the most recent outcomes here: Peter Lynch Strategy Stock Screen.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investing has risks, including the possible loss of the original investment. You should do your own complete research and think about talking with a qualified financial advisor before making any investment choices.