Investors looking for a disciplined, long-term method for choosing stocks frequently consider the ideas of famous fund manager Peter Lynch. His method, explained in his book One Up on Wall Street, centers on finding companies with durable growth, good financial condition, and fair prices, a philosophy often called Growth at a Reasonable Price (GARP). It stresses fundamental study over predicting market movements, urging investors to create a varied collection of comprehensible businesses that can be owned for many years. A primary instrument for using this philosophy is a stock screener that sorts for particular measures Lynch considered vital for long-term achievement.

One company that recently appeared from using a screen modeled on Lynch's ideas is Dorman Products Inc (NASDAQ:DORM), a provider of automotive replacement parts and fasteners. The company works in what Lynch could name a "simple" but necessary field, the motor vehicle aftermarket, serving passenger cars, heavy-duty trucks, and specialty vehicles. For investors following the GARP philosophy, Dorman offers an interesting example of how Lynch's numerical filters and descriptive ideas can come together.

Matching the Lynch Measures

The center of the Peter Lynch screen includes a number of strict financial filters made to remove excessively promoted growth narratives and find companies with durable growth selling at acceptable prices. Dorman Products seems to satisfy these primary checks:

- Durable Earnings Growth: Lynch wanted companies increasing earnings per share (EPS) between 15% and 30% each year over five years, thinking numbers outside this range were troublesome. Dorman's five-year EPS growth rate of 20.7% sits directly within this preferred range, showing a steady, reliable, and manageable growth path.

- Fair Valuation (PEG Ratio): Possibly the most well-known Lynch measure is the Price/Earnings to Growth (PEG) ratio, which tries to price a stock in relation to its earnings growth. A PEG of 1 or below is usually seen as good. Dorman's PEG ratio, calculated from its past five-year growth, is about 0.63, implying the market might be pricing its historical growth too low.

- Good Profitability (Return on Equity): Lynch demanded an ROE of at least 15% to make sure shareholder money was being used productively. Dorman's ROE of 16.7% clearly passes this level, indicating capable management and a successful business plan.

- Sound Financial Condition: The screen also requires a good balance sheet. Dorman's Debt-to-Equity ratio of 0.28 is much lower than the screen's maximum of 0.6 (and even Lynch's more rigid liking for below 0.25), showing little dependence on debt funding. Also, its Current Ratio of 2.94 is much higher than the needed 1.0, showing sufficient cash to meet near-term responsibilities.

These numbers together describe a company that has increased earnings at a good rate, keeps a solid balance sheet, and is valued in a manner that does not require flawless future growth, a central idea of the GARP method.

Fundamental Condition Review

A wider view of Dorman's fundamental picture, as described in a detailed study, mostly supports the screen's results while providing more detail. The company receives a good total fundamental score, with specific high points in profitability, where it gets a 9 out of 10. Its profit, operating, and gross margins are some of the top in the automobile components field. Financial condition is also scored well, backed by the good solvency and cash metrics mentioned before.

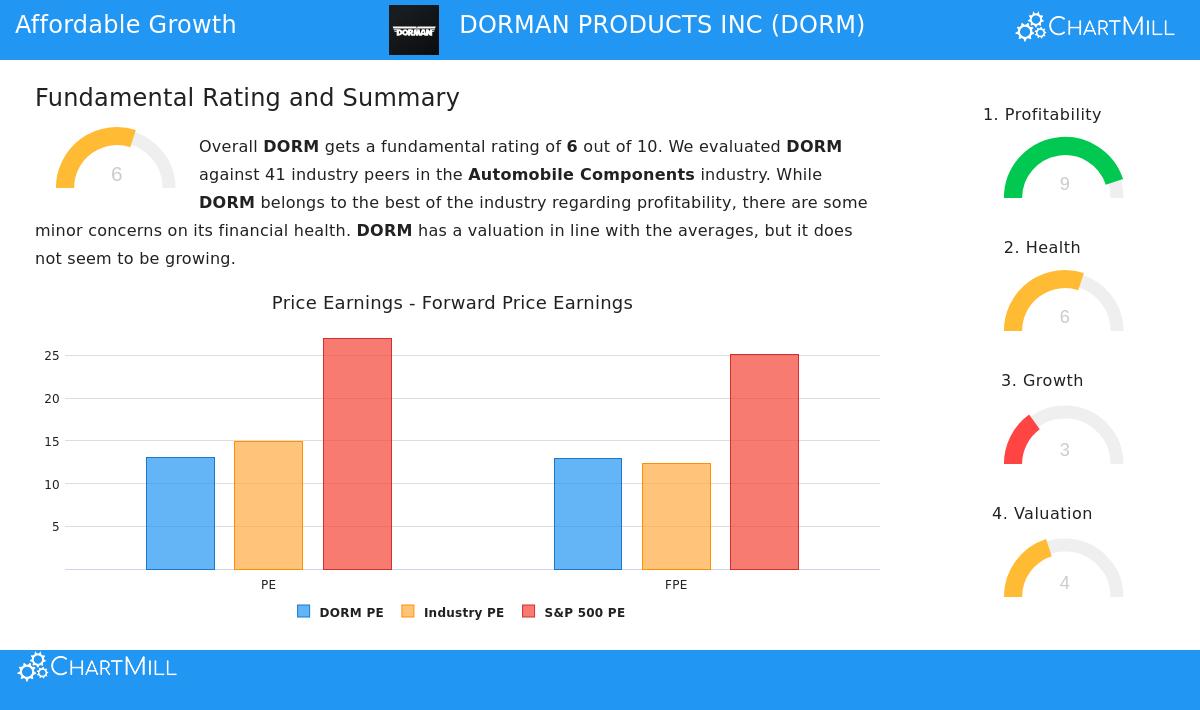

The main points of care noted in the report connect to growth and valuation. While past growth has been good, analysts predict a notable slowdown in EPS growth to about 6.5% each year in the future. This reduced anticipated growth rate leads to a less good forward-looking PEG ratio, which the report marks as a point to watch. From a strict valuation view, Dorman's P/E ratio is similar to field averages and inexpensive compared to the wider S&P 500, but the high profitability might support this valuation.

A View from Lynch's Ideas

Using Lynch's descriptive view, Dorman works in a steady, ordinary field that consumers and businesses need despite the economic climate, the requirement to fix vehicles continues. This matches his suggestion to invest in what you know and comprehend. The company's focus on supplying replacement parts and fasteners is a clear case of a "simple" business that can build value over time. Its high ROE and clean balance sheet give the financial strength Lynch valued, letting a company survive slow periods and keep funding its activities and growth from its own resources.

For investors constructing a long-term, varied collection based on GARP ideas, Dorman Products stands as a candidate deserving more examination. It meets the first numerical tests of a disciplined screen and works in a steady field. The central question for more detailed study, as Lynch would suggest, is if the company can keep a competitive position and move back to a higher growth path, or if the market's present valuation correctly accounts for its future as a stable, slower-growing company.

Interested in finding other companies that match the Peter Lynch investment model? You can review the complete screen and its present findings here.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or an offer to buy or sell any securities. The information shown is from supplied data and should not be the only reason for an investment choice. Investors must do their own complete research and talk with a qualified financial advisor before making any investment.