For dividend investors looking for reliable income, a common method involves searching for companies that provide a good yield and have the financial capacity to maintain and raise their payments over time. This method values quality and long-term viability over seeking the highest yield. A practical technique is to select stocks with a high dividend rating, which assesses elements such as yield, growth, and payment sustainability, while also confirming the core business displays acceptable profitability and sound finances. This assists in steering clear of "yield traps," companies with excessively high dividends that are often a sign of a falling stock price due to business problems.

Quest Diagnostics Inc (NYSE:DGX) appears as a candidate from this careful search process. As a top provider of diagnostic testing and information services, the company works in the necessary healthcare field, which can provide some stability during different economic periods.

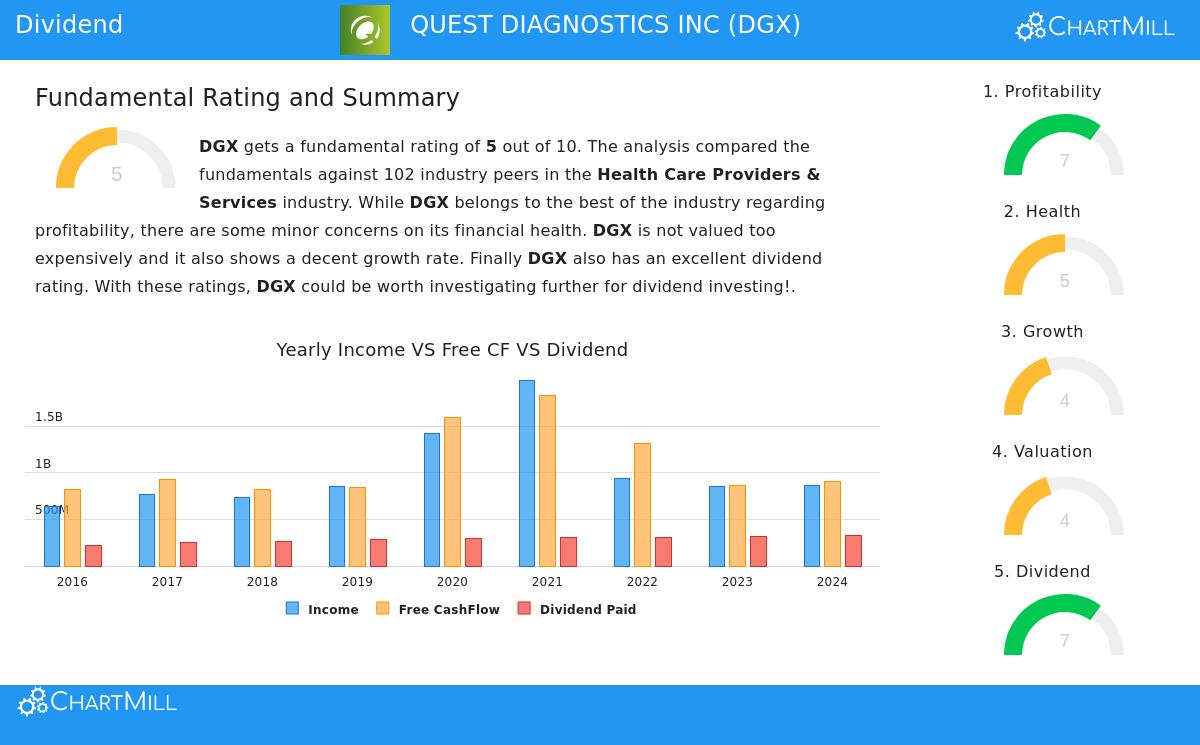

Dividend Profile: A Look at Reliability and Growth

The main attraction for dividend investors is Quest Diagnostics' dividend profile, which receives a firm 7 out of 10 on the ChartMill Dividend Rating. This rating combines several important measures that are key for a lasting income plan.

- Yield and Payout: The company provides a forward dividend yield near 1.75%. This is not the highest figure available, but it is notably above the industry average of 0.48% and compares well with the wider S&P 500. Significantly, the dividend seems secure. The payout ratio is at a manageable 36% of earnings, showing the company keeps enough money to fund its operations while paying shareholders, a sign of a lasting dividend practice.

- History of Growth: Quest Diagnostics shows a dedication to giving more capital back to shareholders over time. It has raised its dividend for at least ten straight years, reaching a five-year annualized dividend growth rate close to 7%. This reliable growth is a key part for income investors aiming to counter inflation over many years.

- Sustainability Match: The review states that the dividend is increasing at a pace similar to earnings growth. This match is important; it indicates the dividend raises are paid for by actual business growth rather than by straining finances, which supports the expectation for future, dependable raises.

Supporting Fundamentals: Profitability and Financial Condition

A good dividend depends on the company supporting it. The search criteria needed acceptable scores in profitability and financial condition, areas where Quest Diagnostics displays both positive aspects and acceptable points of attention.

Profitability is a definite positive, getting a rating of 7. The company produces strong margins and returns on capital that stack up well against others in the healthcare services field.

- Its profit margin of 8.88% and operating margin of 14.71% place in the top tier of its industry.

- Return on equity (13.27%) and return on invested capital (8.79%) are also good, showing effective use of shareholder money.

This steady profitability supplies the basic earnings capacity needed to pay for the dividend. A company with low margins or poor returns would have trouble keeping up, or increasing, its shareholder payments over many years.

Financial Condition gets a middle rating of 5, showing a mixed view. The company's ability to pay debts is not a primary worry, with an Altman-Z score in the "safe" range and a debt-to-equity ratio (0.71) similar to industry standards. However, liquidity measures like the current and quick ratios are seen as lower than many peers. For dividend investors, the main point is that while the company has a fair amount of debt, its good cash flow production, shown by an acceptable debt-to-free-cash-flow ratio of 4.07, offers a way to handle its debts without threatening the dividend. The search filter for acceptable condition helps identify companies that are not carrying too much debt, a necessary check to confirm dividend durability during economic slowdowns.

Valuation and Growth Setting

From a valuation viewpoint, Quest Diagnostics does not seem overly expensive. Its price-to-earnings ratio is lower than both the industry and S&P 500 averages, possibly providing a fair buying opportunity. Growth forecasts are moderate, with analysts expecting mid-single-digit percentage growth in both revenue and earnings per share. This stable, foreseeable growth pattern often fits with a good dividend investment plan, as it matches the company's capability to provide steady, small dividend raises.

For a complete look at all these basic factors, you can examine the full ChartMill Fundamental Analysis Report for DGX.

Conclusion

Quest Diagnostics offers an example of using a quality-centered dividend search plan. It fits the main requirements by providing a good and increasing yield supported by a sustainable payout ratio, a ten-year history of raises, and the backing of a profitable, essential-service business. The search filters for profitability and condition help find companies where the dividend is more probable to last and less probable to be temporary.

For investors wanting to examine other companies that meet similar filters for dividend quality, profitability, and financial condition, you can use the Best Dividend Stocks screen to create a new list of possible ideas for more study.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. Readers should conduct their own thorough research and consider their individual financial circumstances and risk tolerance before making any investment decisions.