For investors aiming to create a portfolio centered on steady income, a systematic selection process is important. One useful technique includes searching for companies that provide a good dividend now and also have the basic financial soundness to maintain and increase those payments in the future. This method focuses on a high dividend score, which assesses yield, increase, and durability, while also needing acceptable marks in earnings strength and balance sheet condition. This layered technique helps sidestep the problem of high-yield stocks that could be in danger of reducing their distributions because of poor business foundations. A stock that appears from such a strict filter deserves more attention from investors concentrating on income.

Examining the Dividend Details

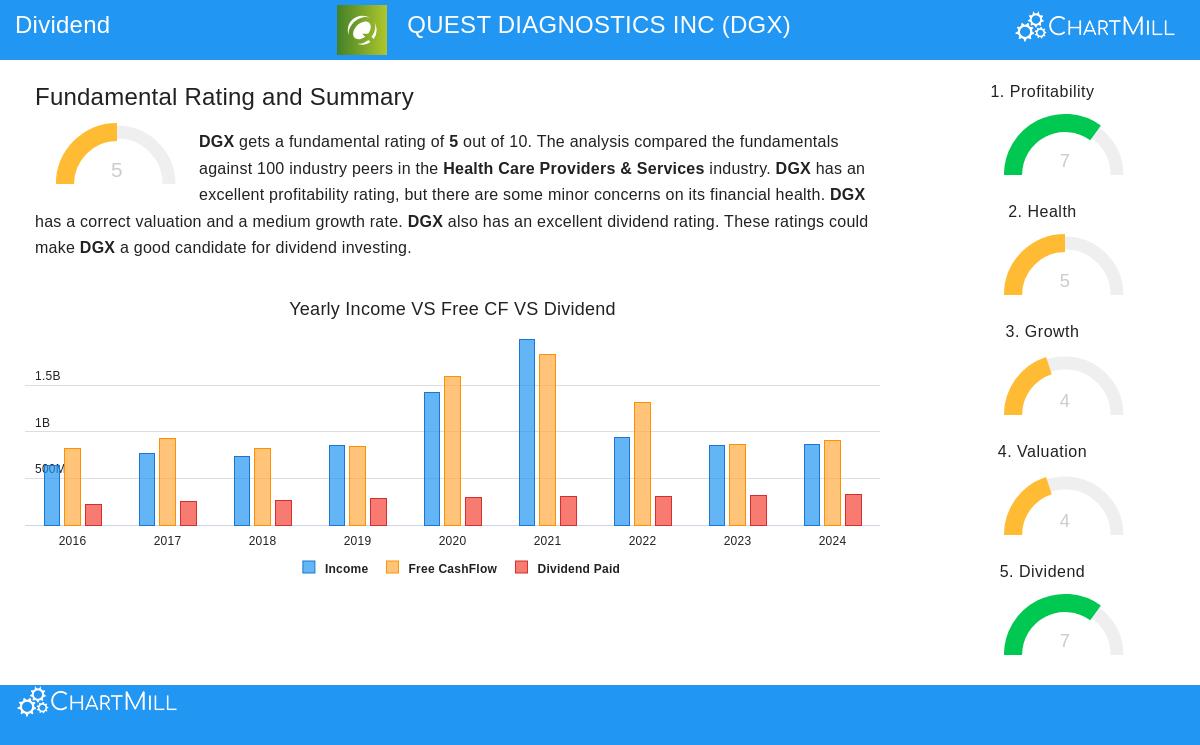

Quest Diagnostics Inc. (NYSE:DGX) appears as a result from this selection method, receiving a good ChartMill Dividend Rating of 7. The company's attraction for dividend investors rests on several main points:

- Steady and Increasing Income: DGX provides a dividend yield of 1.80%, which is notably higher than the industry average of 0.59% and compares well with the wider S&P 500. Significantly, the company has a history of steady increase, with a yearly dividend growth rate of 6.92% over the last five years. It has paid and, importantly, not reduced its dividend for at least ten years, showing a clear dedication to giving capital back to shareholders.

- Manageable Payout Ratio: A fundamental part of secure dividend investing is making sure the payout does not stress the company's finances. DGX does well here, with a payout ratio of only 36.03% of its earnings. This low ratio indicates the company keeps enough capital to put back into its operations, handle obligations, and endure economic slowdowns without threatening the dividend. The report states that earnings increase is matching dividend growth, further supporting the durability of the present policy.

Supporting Business Foundations: Earnings Strength and Condition

The selection method correctly highlights that a good dividend cannot stand alone; it must be backed by a profitable and financially stable business. DGX's basic report confirms this supporting framework.

- Good Earnings Strength (Rating: 7): The company's earnings measures are a main positive. It has a very good Return on Assets of 5.95% and a sound Return on Equity of 13.27%, both better than most of its competitors in the Healthcare Providers & Services industry. Also, its Profit Margin of 8.88% and Operating Margin of 14.71% are viewed as very good compared to the industry. This high degree of earnings strength supplies the necessary cash flow that pays for the dividend.

- Acceptable Balance Sheet Condition (Rating: 5): While not the top rating, a score of 5 shows acceptable financial condition with some points to note. On the good side, DGX's Altman-Z score of 3.26 indicates no short-term bankruptcy danger, and its debt amounts, shown in a Debt/Equity ratio of 0.71, match industry standards. The main areas for attention relate to cash availability, where its Current and Quick ratios are below many industry competitors. Still, the full evaluation suggests the company is financially steady enough to maintain its activities and duties, including its dividend.

Price and Increase Background

From a price standpoint, DGX shows a varied but generally fair view. Its Price/Earnings ratio of 19.14 is considered high on its own but is actually lower than 76% of its industry competitors and the wider S&P 500. This implies investors are paying for quality and steadiness. Increase is consistent rather than outstanding, with previous revenue and EPS growth in the mid-single digits and similar projections ahead. For a dividend investor, this stable, predictable increase pattern can be better than uncertain, high-increase situations, as it backs reliable dividend raises.

Summary

Quest Diagnostics illustrates the kind of company a systematic dividend selection process is meant to find. It joins a good and increasing yield with a very manageable payout ratio, all supported by strong earnings strength and acceptable balance sheet condition. The company's long record of reliable payments and its place in the necessary healthcare services field add to its attraction for investors looking for lasting income. While its price is not very low and cash availability measures need observation, the full basic view fits well with a method focused on safe, growing dividends.

For investors wanting to examine other companies that meet similar standards of high dividend quality, sound earnings strength, and acceptable balance sheet condition, you can see the full filter results here: Best Dividend Stocks Screen.

,

Disclaimer: This article is for information only and does not form financial guidance, a suggestion to buy or sell any security, or a support of any investment plan. The assessment is based on data and scores from ChartMill, which looks at past performance and analyst projections. Investors should do their own complete research and think about their personal money situation and risk comfort before making any investment choices.