Investors constantly manage the tension between a company's expansion potential and the price they pay for it. The "Growth at a Reasonable Price" (GARP) or "Affordable Growth" strategy works to resolve this by focusing on companies that show solid, lasting expansion but are not trading at high valuations. This method aims to avoid the significant risk of paying too much for future potential while still taking part in the gains of developing businesses. Screening for stocks requires a multi-faceted look at fundamentals, assessing not just expansion and valuation, but also the basic financial condition and profitability that make that expansion lasting.

COTERRA ENERGY INC (NYSE:CTRA) appears as a candidate from such a disciplined screening process. The Houston-based diversified energy company, with operations across the Permian Basin, Marcellus Shale, and Anadarko Basin, presents a profile that matches the central principles of affordable growth investing.

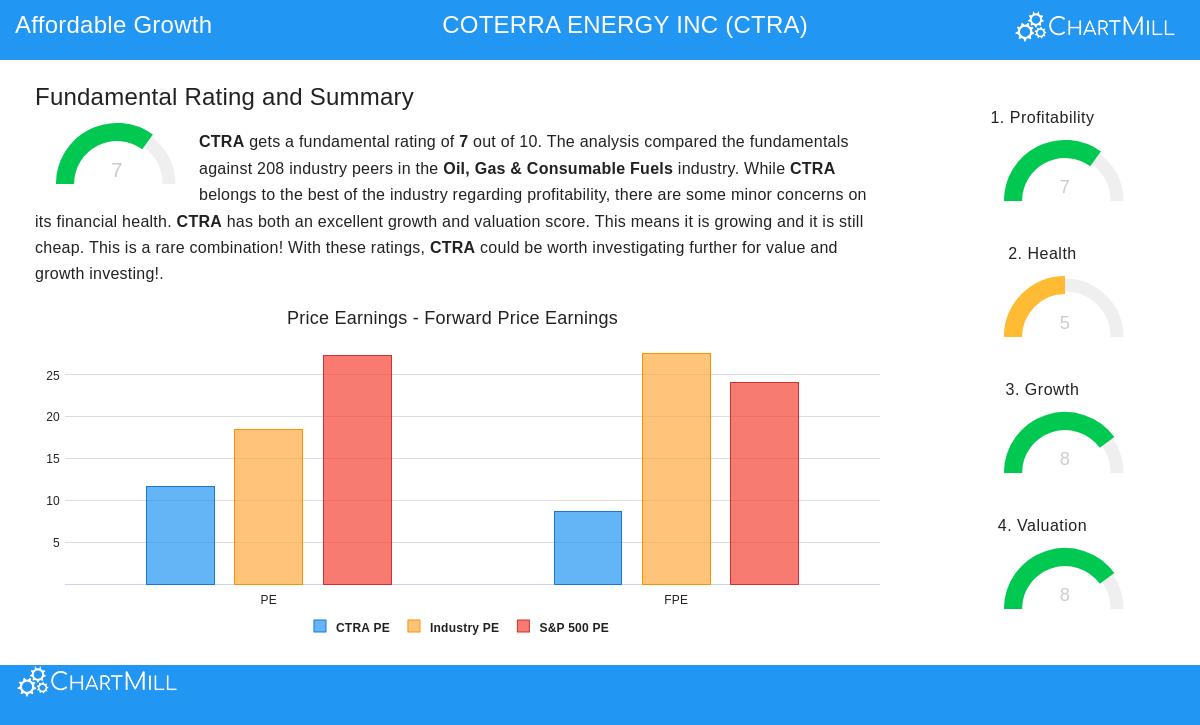

An Appealing Valuation Profile

The foundation of the affordable growth thesis for Coterra is its appealing valuation, which provides a margin of safety. The company's fundamental analysis report gives it a solid Valuation Rating of 8 out of 10. Key metrics support this assessment:

- Price-to-Earnings (P/E): At 11.63, CTRA's P/E ratio is much lower than the S&P 500 average of approximately 27.3. This shows the market is valuing its earnings at a large discount to the broader market.

- Industry Comparison: Within the competitive Oil, Gas & Consumable Fuels sector, CTRA is less expensive than approximately 74% of its peers based on its P/E ratio. Its forward P/E ratio of 8.68 is even more appealing, placing it in a less expensive valuation group than about 86% of industry competitors.

- Growth Compensation: The Price/Earnings to Growth (PEG) ratio, which adjusts the P/E for expected expansion rates, is also low for CTRA. This indicates the current stock price does not completely account for the company's projected earnings expansion, a key signal for GARP investors.

This sensible valuation is important for the strategy, as it helps reduce downside risk. Paying a high price for expansion can lead to large losses if expansion expectations weaken; CTRA's current multiples indicate the market has not included overly hopeful assumptions into its price.

Solid Expansion Path

A low valuation alone is not sufficient; it must be combined with real expansion. Coterra performs here as well, receiving a high Growth Rating of 8. The company shows strength in both recent performance and future expectations.

- Past Performance: In the past year, CTRA reported notable expansion with Revenue rising by 25.1% and Earnings Per Share (EPS) increasing by 26.7%. Over a longer five-year period, Revenue has expanded at an average yearly rate of over 21%.

- Future Expectations: Analyst projections show this momentum is anticipated to continue, though at a slower pace. EPS is forecast to expand at an average rate of about 15.8% yearly in the coming years, while Revenue is expected to rise by roughly 12% per year.

This pairing of strong historical expansion and good forward-looking estimates is exactly what affordable growth screens try to find. It shows a business that is not only a static value option but is actively increasing its operations and earnings capacity.

Supporting Fundamentals: Profitability and Condition

For expansion to be lasting and the valuation to be reasonable, a company must be profitable and financially stable. Coterra's scores in these areas give supportive context.

- Profitability (Rating: 7): The company receives a solid profitability score, supported by industry-leading margins. Its Gross Margin of 82.8% and Operating Margin of 31.3% do better than a large majority of its peers. Returns on assets, equity, and invested capital are all above the industry median, showing efficient use of capital to generate profits. High profitability pays for future expansion projects without heavy dependence on outside financing.

- Financial Condition (Rating: 5): This is the area with some minor points of caution, leading to an average score. On the positive side, Coterra keeps a conservative Debt-to-Equity ratio of 0.25, showing low use of debt financing, and its Debt-to-Free-Cash-Flow ratio is good. However, liquidity metrics like the Quick Ratio are less strong, staying near industry averages. For the affordable growth strategy, a fair condition rating suggests the company is not in financial trouble, which could interrupt its expansion plans, though investors may observe liquidity management.

Conclusion and Additional Research

COTERRA ENERGY INC presents a case study in the affordable growth screening philosophy. It has the dual engines of an appealing valuation, trading at a discount to both the market and its industry, and a confirmed, projected expansion path in both revenue and earnings. This is supported by high profitability and an overall acceptable, though not outstanding, financial position. The screen effectively found a company where the expansion story appears not to be completely accounted for in the market price.

For investors interested in examining other companies that match this profile of good expansion at a sensible price, you can review the full Affordable Growth screen results here. A more detailed look into Coterra's specific fundamentals, including detailed breakdowns of each rating category, is available in its full fundamental analysis report.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy, sell, or hold any security, or an endorsement of any investment strategy. Investors should conduct their own research and consider their individual financial circumstances and risk tolerance before making any investment decisions.