For investors aiming to assemble a portfolio of durable, high-achieving companies for the long term, the ideas of quality investing offer a useful framework. This method looks for businesses with lasting competitive strengths, high profitability, sound financial condition, and steady expansion, traits that let them increase value over many years. One organized way to locate these companies is the "Caviar Cruise" stock screen, which uses measurable filters to find firms with better past results and solid financial measures. The screen looks for continued sales and profit increases, strong returns on invested capital, low debt, and good earnings that become free cash flow.

A recent use of this screen has pointed to Salesforce Inc. (NYSE:CRM) as a possible candidate for more review by investors focused on quality. The cloud software leader seems to fit many of the strategy's main requirements, indicating a company built on a base of operational skill and financial soundness.

Fitting the Core Quality Filters

The Caviar Cruise method uses a group of basic filters to judge a company's quality. Salesforce's shown measures indicate a good fit with these important standards:

-

Revenue and EBIT Growth: The screen asks for at least a 5% compound annual growth rate (CAGR) for both revenue and EBIT (earnings before interest and taxes) over five years. Salesforce goes well beyond this, with a 5-year revenue CAGR of 9.5% and a notable EBIT CAGR of 75.3%. Also, the EBIT growth is much higher than revenue growth, a sign of growing profitability and possible pricing strength, a key trait of a quality business with competitive edges.

-

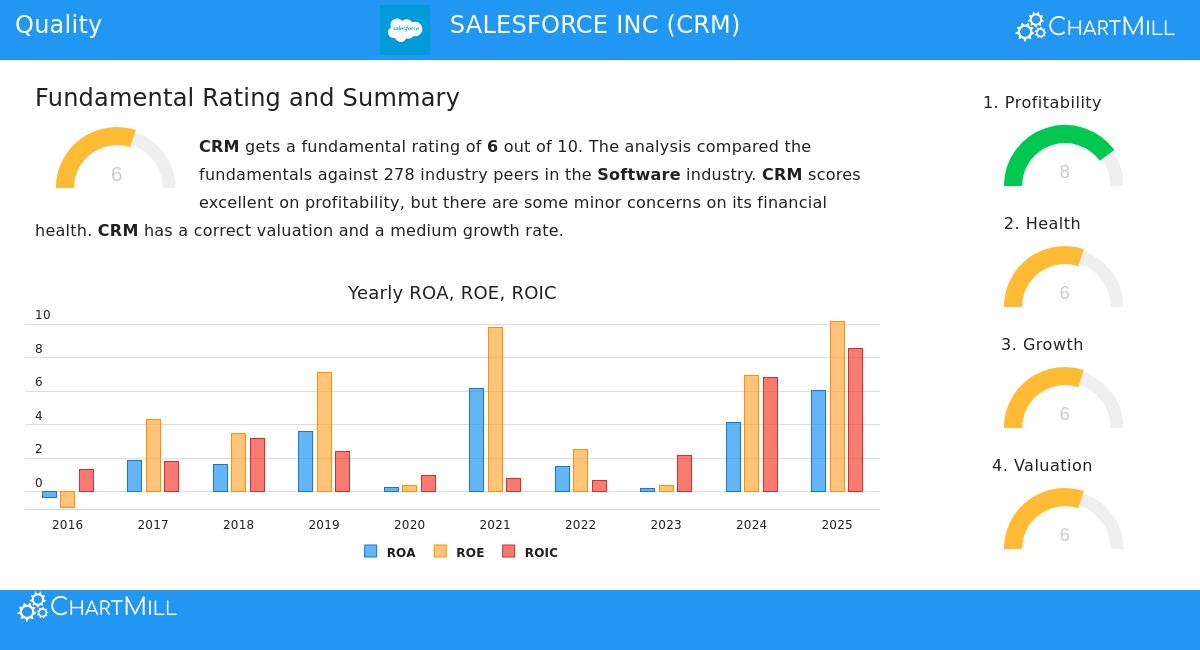

Return on Invested Capital (ROIC): A high ROIC is central to quality investing, showing a company's skill at making good profits from its capital. The screen filters for an ROIC (leaving out cash, goodwill, and intangibles) over 15%. Salesforce's number of 114.6% is very high, putting it at the top of its field and pointing to very efficient use of capital.

-

Debt Management: Financial durability is key. The screen uses a Debt-to-Free Cash Flow (FCF) ratio under 5 to make sure debts are low compared to the cash the business makes. Salesforce's ratio of 0.65 is very good, showing it could pay off all its debt in under a year using its current FCF, which points to a very strong balance sheet.

-

Profit Quality: This measure looks at how much net income becomes free cash flow. The screen wants a 5-year average over 75%, searching for companies whose accounting profits are supported by real cash creation. Salesforce's average profit quality of 786.3% is very high, though this exact number needs explanation. It suggests times where free cash flow creation has been much greater than reported net income, which can happen because of things like large non-cash costs (for example, stock-based compensation) or careful capital spending management. The main point is a shown high ability to create cash.

A Look at Fundamental Condition

Beyond the specific screen settings, a wider view of Salesforce's fundamental picture supports its quality traits. According to its detailed fundamental analysis report, the company gets an overall score of 6 out of 10, with clear positives and some points to note.

Main Positives:

- Profitability: Salesforce scores an 8 out of 10 here, with high margins. Its operating margin of 22.03% and profit margin of 17.91% do better than most of its software industry competitors. Both margins have gotten better in recent years.

- Growth: The company shows good past growth in revenue and earnings per share (EPS), with future projections pointing to continued, though slower, growth.

- Solvency: Its low debt-to-equity ratio (0.14) and high Altman-Z score (4.51) show a very small chance of financial trouble.

Points to Note:

- Liquidity: The report mentions a current and quick ratio below 1, which could point to closer control of working capital. However, it also explains this by noting the company's very good solvency and profitability.

- Valuation: The valuation score is neutral (6/10). While its Price-to-Earnings ratio is higher than the simple average, it is seen as less expensive than most software industry peers and the wider S&P 500 on several measures, including Price-to-Free Cash Flow.

Is Salesforce a "Buy-and-Hold" Quality Stock?

For an investor using a quality-focused, buy-and-hold method, Salesforce makes a strong argument. It works in the long-term growth field of enterprise cloud software, holds a leading competitive place in Customer Relationship Management (CRM), and has shown it can grow profitability greatly as it gets larger. The Caviar Cruise screen successfully finds these numerical traits: fast profit growth, top-level capital returns, a very strong balance sheet, and high cash creation.

The non-numerical aspects a quality investor would also check, such as lasting competitive advantages, a global presence, and importance in the time of AI, match Salesforce's business story. Its use of AI through its "Agentforce" platform seeks to strengthen its long-term importance.

Finding More Quality Candidates

Salesforce is one example found through a strict screening process. Investors wanting to find other companies that meet similar strict quality filters can review the standards themselves using the Caviar Cruise stock screener.

Disclaimer: This article is for information and learning only. It is not a suggestion to buy, sell, or keep any security, including Salesforce Inc. (CRM). All investment choices have risk, and readers should do their own complete research or talk with a qualified financial advisor before making any investment choices.