For investors looking for chances where the market price may not completely show a company's inherent strength, a methodical value method can be a helpful beginning. One frequent tactic involves searching for companies that seem basically undervalued by common measures while still showing good financial condition, earnings, and acceptable expansion potential. This process tries to find possible discounts—stocks selling for less not due to bad business quality, but possibly because of short-term feeling or industry difficulties. CarGurus Inc (NASDAQ:CARG) comes from such a search, showing a picture that calls for more examination from value-focused investors.

A More Detailed Examination of Price

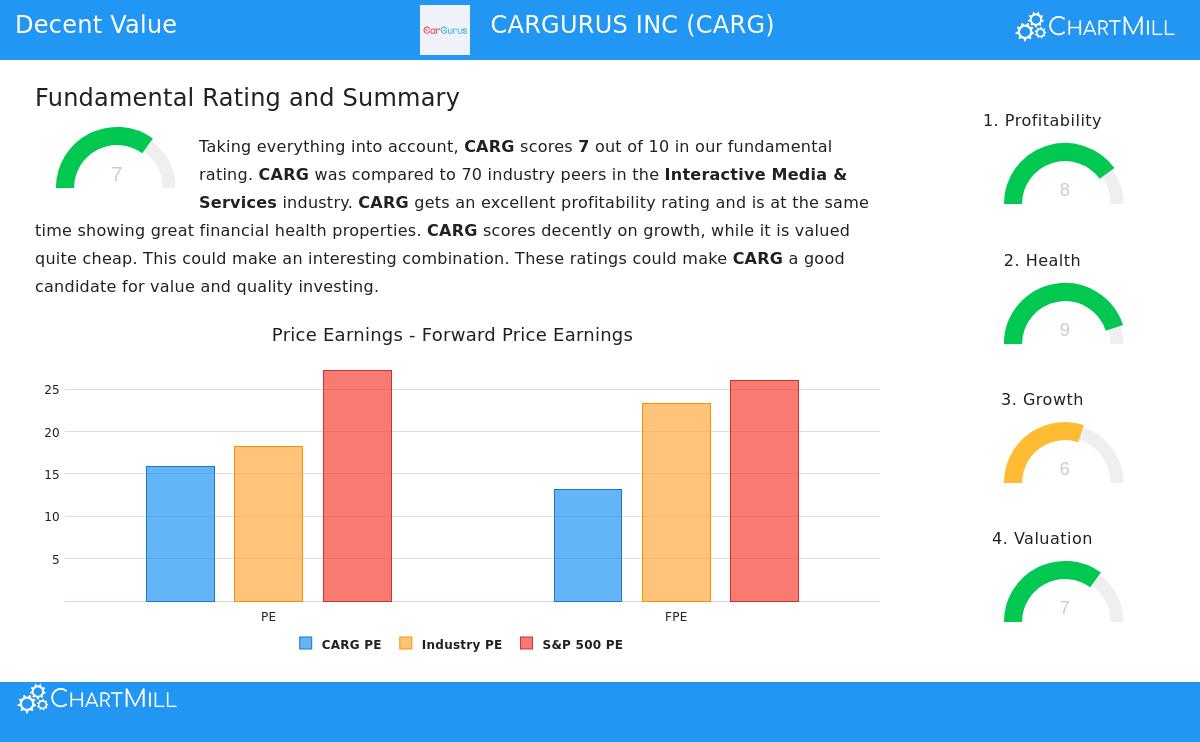

The central idea of value investing is buying a dollar's worth of assets for fifty cents. For CarGurus, the price measures indicate the market may be valuing the company cautiously. According to the fundamental analysis report, the stock gets a Valuation Rating of 7 out of 10, meaning it is valued lower than many similar companies.

- Price-to-Earnings (P/E): At 15.85, CarGurus' P/E ratio is clearly below the S&P 500 average of 27.25. It is also less expensive than almost 73% of companies in the Interactive Media & Services field.

- Forward P/E: The forward P/E of 13.14 adds to this view, selling at a lower price than both the wider market and most of its industry rivals.

- Price-to-Free-Cash-Flow & EV/EBITDA: These numbers also point to a price that is relatively low compared to the industry, with the company being less costly than more than 77% and 67% of peers, in turn.

For a value investor, these measures are the first step. A low price alone can be misleading, but when combined with good fundamentals, it becomes a more interesting case.

Reviewing Financial Condition and Earnings

A company's financial strength is key for a value investment idea. A good balance sheet offers stability in hard economic times and pays for future expansion without too much danger. CarGurus does very well here, having a top-level Health Rating of 9.

- Debt-Free Balance Sheet: The company has no interest-bearing debt, putting its Debt/Equity and Debt/FCF numbers at zero. This is a rare situation that removes default danger and interest cost loads.

- Good Liquidity: With a Current Ratio and Quick Ratio both at 2.87, the company has enough liquid assets to meet near-term debts, doing better than about three-fourths of its field.

- High Earnings: Supporting its condition is a Profitability Rating of 8. Important measures are strong:

- Return on Equity (ROE) of 40.48% puts it in the highest 1% of its field.

- Return on Invested Capital (ROIC) of 23.46% is much higher than its cost of capital, proving the company is building real owner value.

- Operating and Profit Margins are solid, doing better than over 87% and 82% of peers, in turn.

This pairing is strong. The safety buffer that value investors want is increased not just by a low cost, but by a business that is very profitable and works from a place of rare financial soundness.

Considering Expansion Path

While strict value stocks sometimes include slow businesses, the most appealing finds often have an expansion part. CarGurus has a Growth Rating of 6, meaning acceptable, though not fast, increase.

- Past Results: The company has shown good historical profit growth, with EPS rising by 41.18% over the past year and at a typical yearly rate of 26.69% over recent years. Sales growth has been a more steady but still acceptable 8.72% on average.

- Future Predictions: Experts forecast continued EPS growth averaging 21.55% yearly, though sales growth is thought to ease to about 5.88%. This forward-looking steadiness, not a fast drop, is significant; it implies the company's central profit ability is not at risk.

For the value plan described, this amount of growth is enough. The aim is not to find the quickest-increasing company, but one increasing steadily while being priced as if it were not increasing. The predicted growth helps support the company's inherent value and gives a possible reason for the market to revalue the stock.

Final Thoughts: An Interesting Picture for More Study

CarGurus shows a consistent investment picture that matches a methodical value-finding approach. The stock is priced lower than the market and its field, giving the price appeal central to the plan. Importantly, this lower price is not joined with fundamental problems. Instead, it comes with a clean, debt-free balance sheet, excellent profit measures, and a record of good earnings growth that is thought to persist. This gap between price and inherent business quality is exactly what value searches try to find.

It is significant to state that the automotive marketplace field deals with its own recurring and rival pressures, which might add to the stock's low price. However, for investors who trust in the lasting strength of CarGurus' system, the present price may show a chance to get a high-grade business at a fair price.

Interested in finding other stocks that match this "acceptable value" picture? You can look for more possible chances using the same search rules here.

,

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion to buy or sell any security, or a support of any investment plan. The examination is based on data and ratings from ChartMill, and investors should do their own complete study and think about their personal money situation before making any investment choices.