In the world of investing, the search for undervalued opportunities is a timeless pursuit. One systematic approach involves screening for companies that appear fundamentally cheap but are not necessarily broken. This method looks for stocks with good valuation ratings, indicating they trade at a discount to their intrinsic worth, while simultaneously maintaining acceptable scores in profitability, financial health, and growth. This combination seeks to identify businesses that are priced low relative to their earnings and assets, yet have the operational soundness and stability to possibly close that valuation gap over time. Such a profile can be especially attractive to value-oriented investors looking for a margin of safety.

A recent screen using this methodology has identified Cal-Maine Foods Inc (NASDAQ:CALM) as a candidate for more detailed review. As the largest producer and distributor of shell eggs in the United States, Cal-Maine runs a fully integrated business, from feed production and flock management to processing and distribution. The company's fundamental report, available here, shows a notable mix of deep-value traits and foundational financial soundness.

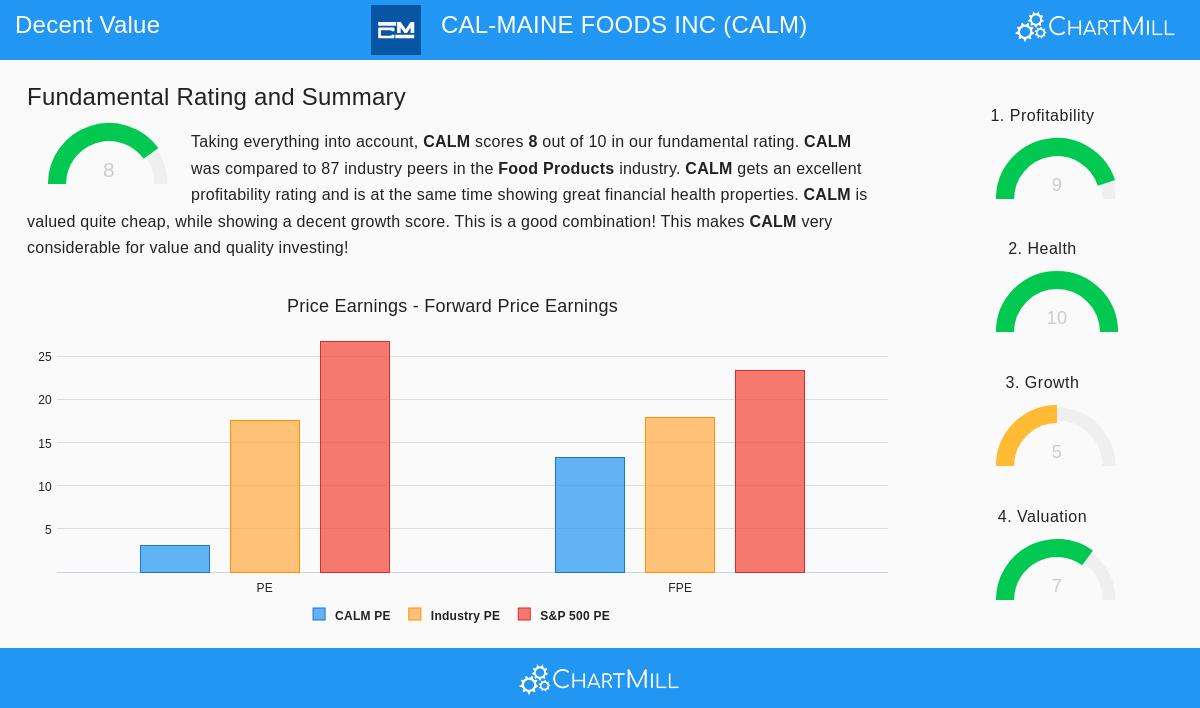

Valuation: A Clear Discount

The center of any value investment thesis is valuation, and here Cal-Maine is notable. The company's overall Valuation Rating of 7 out of 10 is supported by metrics that point to a large discount to both its industry and the wider market.

- Price-to-Earnings (P/E) Ratio: At just 3.10, CALM's P/E ratio is very low. This shows investors are paying only $3.10 for every dollar of the company's earnings over the past year. For comparison, this is lower than 98.85% of its peers in the Food Products industry and a small part of the S&P 500's average P/E of nearly 27.

- Price-to-Free Cash Flow: The company also trades at a large discount based on the cash it produces, ranking lower than 96.55% of its industry competitors on this metric.

- Forward-Looking Context: While the forward P/E ratio of 13.29 is closer to the market average, it remains lower than almost three-quarters of its industry peers. This forward multiple mirrors analyst expectations for normalized earnings, suggesting the current very low trailing P/E may be partly due to an exceptional, and possibly cyclical, peak in profitability.

For a value investor, these metrics are the beginning. A low P/E can indicate a bargain, but it is only a lasting opportunity if the company's earnings are supported by a sound and healthy business—a possible "value trap" must be sidestepped.

Financial Health: A Strong Balance Sheet

This is where Cal-Maine's profile becomes especially interesting. The company receives a perfect Health Rating of 10 out of 10, signaling very good financial stability—a key protection for value investments.

- Zero Debt: Maybe the most notable feature is that Cal-Maine has no interest-bearing debt on its balance sheet. This removes bankruptcy risk and gives great operational and strategic freedom.

- Strong Liquidity: The company's liquidity ratios are excellent, with a Current Ratio of 6.84 and a Quick Ratio of 5.62. This means it has more than enough short-term assets to meet its immediate obligations many times over, putting it in the best group of its industry.

- Altman-Z Score: A score of 9.48 solidly puts the company in the "safe" zone, showing very low near-term risk of financial trouble.

This flawless financial health supplies the "margin of safety" that value investors seek. It means the company can endure industry slowdowns, put money into operations, or return capital to shareholders without pressure from creditors, making the low valuation seem less hazardous.

Profitability: Exceptional Returns

A cheap stock is only a good investment if the underlying company is profitable. Cal-Maine does very well here also, scoring a 9 out of 10 for Profitability. The company is not just profitable; it is very efficient.

- Outstanding Margins: The company has a Profit Margin of 28.86% and an Operating Margin of 36.21%, doing better than over 98% of its industry. Its Gross Margin of 43.54% is also near the top of the sector.

- Superior Capital Efficiency: The Return on Invested Capital (ROIC) of 41.57% and Return on Equity (ROE) of 47.07% are remarkable, showing management is creating very high returns on the capital given to it.

These metrics are important because they prove that the company's earnings power is real and efficient. For a value investor, good profitability confirms the earnings used in valuation ratios and indicates the business has a lasting competitive edge, even in a commodity-like industry.

Growth and Dividend: A Mixed Picture with Income Appeal

The picture is more complex in the Growth category, where Cal-Maine scores a 5. The company has a strong recent history but confronts expected challenges.

- Past Performance: Over the past year, the company saw rapid growth, with Earnings Per Share (EPS) up 221% and Revenue up 66%. The multi-year averages are also very good.

- Future Expectations: Analysts forecast a decrease in the coming years, with EPS expected to fall by over 35% annually. This expected return to normal from recent highs is a main factor in the stock's low valuation.

- Income Component: Balancing some of the growth questions is a solid Dividend Rating of 6. The stock gives a significant yield of 6.65%, which is much higher than both the industry and S&P 500 averages. With a sustainable payout ratio of 32%, this income delivers a real return while investors wait for a possible valuation improvement.

This situation is typical in cyclical businesses. The value idea rests on buying when expectations are low and the price shows a downturn, provided the company's financial health (which Cal-Maine has in large measure) lets it endure and succeed through the cycle.

Conclusion

Cal-Maine Foods offers a standard value investment example: a company trading at a large discount based on traditional valuation metrics, yet supported by a strong balance sheet and historically high profitability. The low P/E ratio is explained by expectations of earnings returning to normal, but the perfect financial health score gives a large margin of safety against downside risk. The high dividend yield provides payment for the wait. For investors screening for reasonable value—stocks that are cheap but not broken—CALM's mix of a valuation discount, perfect health, and good profitability makes it a notable candidate for more fundamental research.

This review of Cal-Maine Foods was found using a specific fundamental screening method. If you want to find other companies that match a similar profile of acceptable valuation along with reasonable fundamentals, you can examine the screen more here.

Disclaimer: This article is for informational and educational purposes only and does not form a recommendation to buy, sell, or hold any security. The analysis is based on data and ratings given by ChartMill.com. All investing involves risk, including the possible loss of principal. Investors should do their own independent research and think about their personal financial situation before making any investment decision.