For investors looking for chances where a company's market price may not match its basic business condition, a methodical value investing method can be a practical structure. This plan centers on finding stocks that seem priced low according to fundamental measures, such as earnings, cash flow, and financial condition, while still showing acceptable operational results. The aim is to locate good companies selling for less, providing a possible "margin of safety" as famously supported by Benjamin Graham. A useful way to use this technique is by filtering for stocks with good valuation marks along with acceptable scores in profitability, financial condition, and growth.

One stock that recently appeared from such a "Decent Value" filter is BorgWarner Inc (NYSE:BWA), an important provider of developed technology parts for combustion, hybrid, and electric vehicles. The company's fundamental picture indicates it may deserve more attention from investors focused on value.

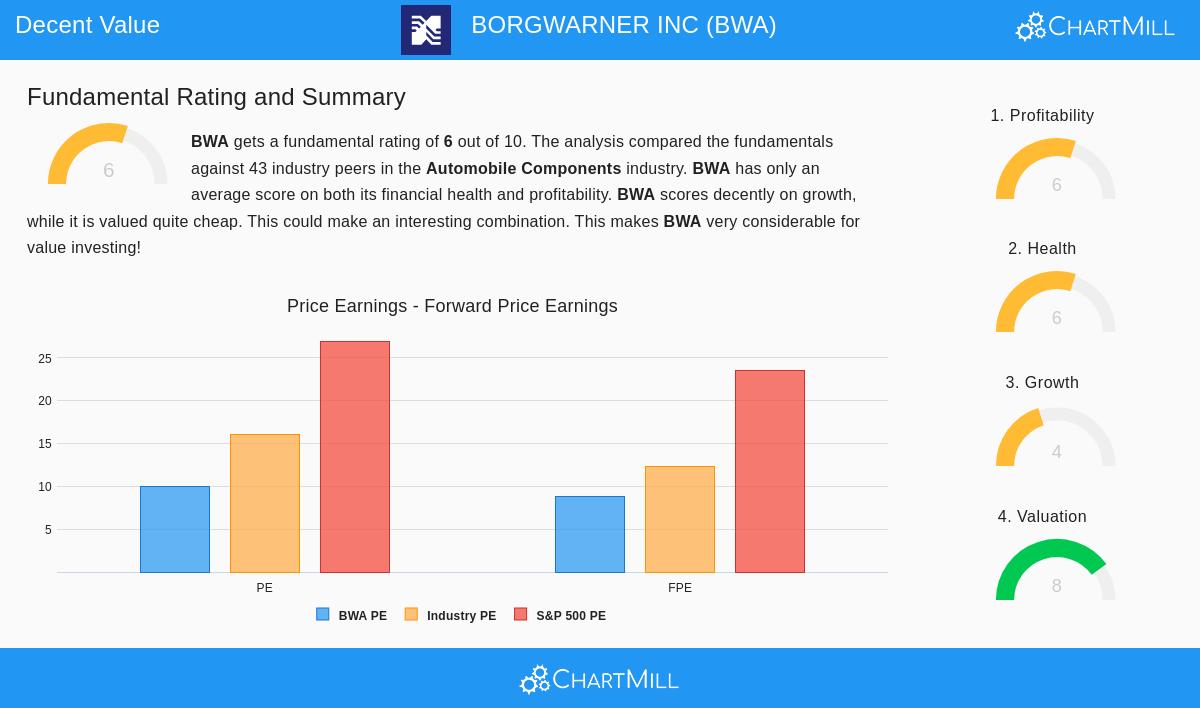

Examining Valuation

The most interesting beginning for BWA is its valuation. According to its fundamental analysis report, BorgWarner gets a high ChartMill Valuation Rating of 8 out of 10. This mark comes from several important measures that show a stock priced cautiously compared to its earnings and cash flow.

- Price-to-Earnings (P/E) Ratio: At 9.97, BWA's P/E ratio is much lower than the S&P 500 average of about 26.9. This shows the market is paying less for each dollar of BorgWarner's earnings compared to the wider market.

- Industry Comparison: The valuation seems even more appealing within its own field. BorgWarner is valued lower than 86% of similar companies in the Automobile Components industry based on its P/E ratio, and lower than 88% based on its forward P/E ratio of 8.77.

- Cash Flow and EBITDA: The company's price-to-free-cash-flow and enterprise-value-to-EBITDA ratios are also marked as "rather cheap" compared to industry peers, doing better than over 83% of them.

For a value investor, these measures are important. A low valuation relative to earnings and cash flow can mean the market has missed the company's possibility or is accounting for too much negative outlook, creating the possible difference between market price and inherent value that value plans try to use.

Evaluating Financial Condition and Profitability

A low valuation by itself is not sufficient; it must be combined with a fundamentally stable business to prevent a "value trap." BorgWarner's financial condition and profitability marks give this important background.

The company receives a firm ChartMill Financial Health Rating of 6. Its balance sheet indicates condition in liquidity, with a strong current ratio of 2.05, showing a good ability to meet near-term needs. The debt-to-free-cash-flow ratio of 3.15 is viewed as acceptable, suggesting it would take just over three years of current cash flow to settle all debt, a ratio more favorable than almost 80% of its industry peers. While the company holds a medium amount of debt (Debt/Equity of 0.65), its overall stability picture is viewed as satisfactory within the industry.

On profitability, BorgWarner gets a rating of 6. Its Return on Invested Capital (ROIC) of 9.21% is notable, doing better than 84% of industry rivals. This measure is important as it shows how effectively the company is using its capital to produce profits. Also, its operating margin of 9.59% is also good relative to the sector. These elements show that in spite of the stock's low price multiples, the basic business is creating acceptable returns on capital, a central idea for value investors who look for quality at a lower price.

Growth Path and Dividend

While not a rapid-growth case, BorgWarner shows steadiness with a ChartMill Growth Rating of 4. Recent results include an 8.55% growth in Earnings Per Share (EPS) over the last year. Looking ahead, analysts predict modest average yearly EPS growth of about 6%. The company also gives a dividend yield of 1.50%, which is above the industry average, though investors should note the payout ratio is currently elevated.

For a value plan, medium, steady growth is often enough. The focus is on buying a profitable and condition-strong business at a low price; fast growth is less of a concern than reliable cash creation and financial strength.

Final Thoughts: A Possibility for Value Review

BorgWarner Inc presents a picture that matches several value investing ideas: it is priced at a clear discount to both the wider market and its industry peers, yet it keeps a profitable operation with a condition-strong balance sheet and an acceptable return on capital. The mix of a high valuation score with satisfactory marks in condition and profitability suggests the market may be setting too low a price on its steady business model as it operates within the automotive industry's shift to electrification.

Naturally, this examination is a beginning. Value investors must think about wider elements like competitive risks, management performance, and industry cycles before making any investment choice. The "margin of safety" comes not only from the figures, but from a full understanding of the business.

Interested in filtering for more stocks that match this "Decent Value" picture? You can use the same filter used to find BWA and find other possible chances here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.