The investment philosophy of Peter Lynch, the famous manager of the Fidelity Magellan Fund, focuses on finding well-run, growing companies trading at reasonable prices. His method, often called Growth at a Reasonable Price (GARP), stresses sustainable growth, financial soundness, and a price that does not overpay for future potential. Investors using this method usually look for companies with strong but not extreme earnings growth, good profitability, controlled debt, and an attractive price when growth is considered. One company that recently appeared from such a search is Boot Barn Holdings Inc (NYSE:BOOT).

A Snapshot of the Business

Boot Barn Holdings Inc works as a top seller of western and work-related footwear, apparel, and accessories. With about 475 stores in 49 states and a larger online sales operation, the company has created an important niche. Its selection includes popular brands like Ariat, Wrangler, and Justin, serving both lifestyle and job needs. This concentration on a particular, dedicated customer group fits with Lynch’s idea of investing in businesses that are easy to understand and have products with steady demand.

Meeting the Peter Lynch Criteria

A search based on Lynch’s main ideas points out several important positives in Boot Barn’s financial picture. The method puts first sustainable growth, financial steadiness, and good price, all of which are clear in the company’s numbers.

- Sustainable Earnings Growth: Lynch preferred companies with a steady earnings growth history, usually between 15% and 30%, to stay away from unstable fast growth. Boot Barn’s earnings per share (EPS) have increased at a notable average yearly rate of 28.7% over the last five years, putting it well inside this wanted range. This shows a tested skill to enlarge profit over time.

- Strong Profitability: A high Return on Equity (ROE) is a key part of the method, showing good use of shareholder money. Boot Barn’s ROE of 17.3% easily passes Lynch’s suggested 15% level, proving that management is creating good profit from the money put into the business.

- Exceptional Financial Health: Lynch was cautious about high debt. Boot Barn’s balance sheet is very solid, with a Debt-to-Equity ratio of only 0.01. This very small debt amount gives important financial room and lowers risk in economic declines, a key point for long-term owners.

- Sound Liquidity: The method also tests for near-term financial steadiness using the Current Ratio. Boot Barn’s ratio of 2.35 shows it has more than enough short-term assets to pay its short-term bills, indicating a good cash position.

- Reasonable Price Relative to Growth: Maybe the most important Lynch number is the PEG ratio (Price/Earnings to Growth), which tries to find stocks where the price is fair given the growth rate. A PEG at or under 1.0 is seen as attractive. Boot Barn’s PEG ratio, based on its past five-year growth, is 0.97. This hints the market may not be completely counting its past growth path, giving a possible opening for GARP investors.

Fundamental Analysis Overview

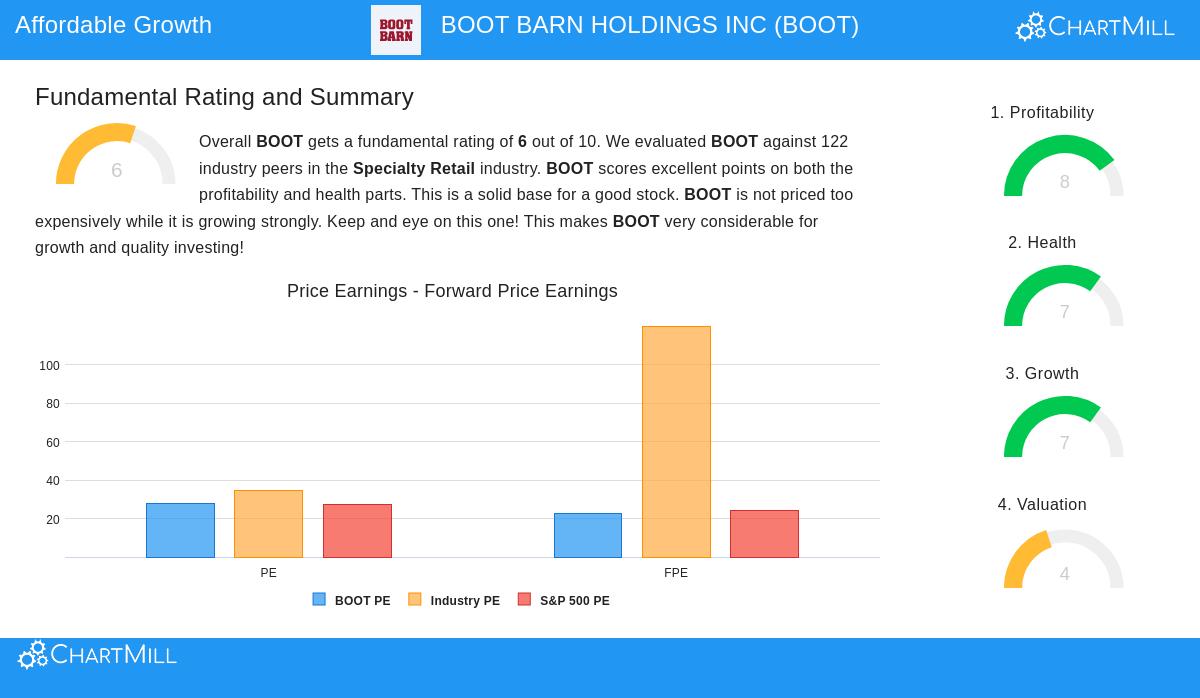

A wider fundamental analysis of Boot Barn supports the search’s results. The company gets a total rating of 6 out of 10, with specific positives in profitability and financial health.

- Profitability & Margins: Boot Barn gets high ratings for profitability (score 8/10). Its profit and operating margins are in the top group of the specialty retail industry and have gotten better in recent years. Good returns on assets, equity, and invested money further prove its efficient work.

- Financial Health: The company’s health score is good (7/10), pushed by an exceptional debt-free profile. Its low debt-to-FCF ratio and high Altman-Z score mean very low failure risk and a very solid ability to handle its debts.

- Growth Path: Boot Barn’s growth rating is positive (7/10), backed by notable past growth in both sales and EPS. While future growth guesses stay positive, analysts expect a slowdown from the very high past rates, which is normal as a company gets older.

- Price Context: The price score is neutral (4/10). While its P/E ratio seems high alone, it costs less than many industry competitors. When growth is counted using the PEG ratio, and thinking about the company’s high profitability, the price seems more acceptable for a long-term investor.

Conclusion and Further Research

For investors who follow the Peter Lynch idea of buying growing companies at fair prices, Boot Barn offers an interesting example. It shows the signs Lynch liked, a clear business model, a solid history of sustainable earnings growth, exceptional balance sheet strength, high profitability, and a price that seems fair when its growth is included. The company’s niche leadership in western and workwear gives a lasting competitive edge.

It is key to note that a search is a first step for more study. Possible investors should review the company’s competitive field, growth plans, and any industry-specific dangers. For those wanting to look at other companies that match this careful GARP method, you can see the full search here.

,

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.