The investment philosophy of legendary fund manager Peter Lynch, detailed in his book One Up on Wall Street, focuses on finding well-run, growing companies trading at reasonable prices, a strategy often described as Growth at a Reasonable Price (GARP). Lynch supported a long-term, buy-and-hold method, concentrating on businesses with sustainable earnings growth, strong financial health, and valuations that do not overpay for future prospects. His process uses specific quantitative filters to find candidates, which investors can then study more to learn about the actual business. One company that recently appeared from such a filter is Boot Barn Holdings Inc (NYSE:BOOT).

A Peter Lynch Candidate: Breaking Down the Criteria

Boot Barn, a leading retailer of western and work-related footwear, apparel, and accessories, seems to fit several important filters in a Lynch-inspired screen. The strategy highlights sustainable growth, profitability, financial strength, and an appealing valuation when growth is considered. Here is how Boot Barn compares against some of the central Lynch criteria:

- Sustainable Earnings Growth: Lynch wanted companies with a steady history of growth, but he was cautious of extreme growth that could not be kept up. He usually searched for a 5-year earnings per share (EPS) growth rate between 15% and 30%. Boot Barn’s EPS has increased at a notable average rate of 28.7% over the past five years, putting it at the higher end of this sustainable range.

- Profitability (Return on Equity): A high Return on Equity (ROE) shows a company’s skill at creating profits from shareholder equity. Lynch liked companies with an ROE above 15%. Boot Barn’s ROE of 17.3% easily meets this level, pointing to capable management and a profitable business model.

- Financial Health (Debt & Liquidity): A conservative balance sheet was crucial for Lynch. He chose companies funded more by equity than debt, often searching for a Debt-to-Equity ratio below 0.6 (and preferably below 0.25). Boot Barn does very well here with an extremely low Debt-to-Equity ratio of 0.01. Also, Lynch appreciated companies with sufficient liquidity to meet short-term needs, typically requiring a Current Ratio of at least 1. Boot Barn’s Current Ratio of 2.35 shows a solid liquidity position.

- Reasonable Valuation (PEG Ratio): Maybe the most unique Lynch measure is the Price/Earnings to Growth (PEG) ratio, which compares a stock’s P/E ratio to its earnings growth rate. A PEG ratio of 1 or less implies the stock may be fairly priced for its growth. Boot Barn’s PEG ratio, based on its past five-year growth, is 0.92, meaning its valuation seems reasonable when its historical growth is considered.

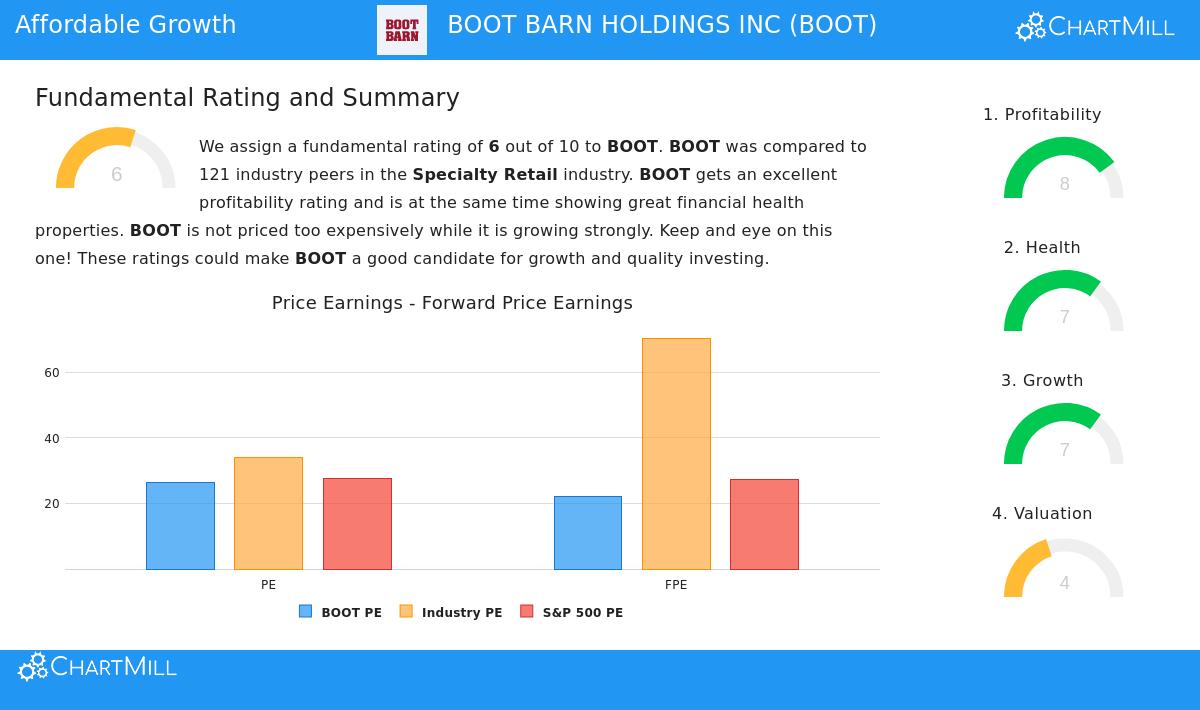

Fundamental Health and Growth Path

A wider view of Boot Barn’s fundamental profile supports the image shown by the Lynch screen. The company’s overall financial health is strong, marked by very good solvency measures and solid, getting better profit margins. Its growth narrative is persuasive, with notable rises in both revenue and earnings over recent years.

While future growth forecasts stay positive, analysts expect a slowdown from the outstanding speed of the past. This is not unusual as companies get older and is something Lynch recognized by filtering out unreasonably high growth rates. The important point is that growth is predicted to persist, though at a more moderate speed that could be maintained over the long term.

For a detailed view of Boot Barn’s profitability, health, valuation, and growth scores compared to its industry peers, you can examine the full fundamental analysis report.

Is Boot Barn a "Dull" Company Worth Watching?

Peter Lynch famously recommended investors search for chances in "dull" companies that are simple to understand. While the western wear niche has a loyal customer base and cultural attraction, Boot Barn works in the simple business of specialty retail. The company has effectively carried out a store expansion plan while increasing its e-commerce activity, a clear business model that is fairly easy to grasp. This fits with Lynch’s rule of investing in what you can understand.

For investors using a GARP or Lynch-inspired strategy, Boot Barn offers a case study of a company with a solid historical growth record, high profitability, a very strong balance sheet, and a valuation that accounts for its growth. It shows the kind of business Lynch might recommend adding to a watchlist for more study.

Interested in finding other companies that match this disciplined investment method? You can run the screen yourself and see the current results via the Peter Lynch Strategy stock screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. Always conduct your own thorough research and consider your individual financial circumstances before making any investment decisions.