For investors looking for a disciplined, long-term way to build wealth, few strategies are as respected as Peter Lynch’s method. The famous manager of Fidelity’s Magellan Fund supported a "growth at a reasonable price" (GARP) idea, concentrating on companies with good, lasting growth, sound financial condition, and appealing prices. His strategy, outlined in One Up on Wall Street, stresses fundamental study over guessing market movements, urging investors to locate businesses they can grasp with clear earnings and controlled debt before keeping them for many years. A filter using Lynch’s main rules recently found Baker Hughes Co (NASDAQ:BKR) as a possible option for more examination.

Matching the Lynch Rules

Baker Hughes, a worldwide energy technology firm, seems to fit many of Peter Lynch's important investment tests. The method looks for companies increasing earnings at a good but maintainable rate, are financially secure, earn money, and are not priced too high compared to that growth. A look at the given numbers shows BKR passes these initial tests:

- Maintainable Earnings Growth: Lynch liked companies with a 5-year earnings per share (EPS) increase between 15% and 30%, quick enough to be interesting but not so fast it might not last. Baker Hughes states a 5-year EPS growth rate of 23.35%, putting it directly within this desired zone.

- Sensible Price (PEG Ratio): A key part of the GARP idea is the PEG ratio, which changes the common P/E ratio for growth. Lynch wanted a PEG of 1 or lower, meaning the market might not completely account for the company's growth path. BKR's PEG ratio, using past 5-year growth, is 0.84, hinting the stock may be fairly priced relative to its historical earnings increase.

- Good Profitability (ROE): Return on Equity (ROE) shows how well a company creates profits from shareholder money. Lynch needed an ROE above 15%. Baker Hughes passes this with an ROE of 15.92%, showing capable management and a lasting edge.

- Cautious Financial Setup (Debt/Equity): To confirm stability, Lynch chose companies supported more by equity than debt, with a Debt/Equity ratio below 0.6 (and preferably below 0.25). BKR's D/E ratio of 0.33 shows a careful balance sheet, offering safety from economic drops or higher interest costs.

- Sufficient Short-Term Condition (Current Ratio): The last basic test is cash availability, making sure a company can pay its upcoming bills. A Current Ratio of 1 or more is the standard. Baker Hughes meets this with a ratio of 1.41.

A Wide Fundamental View

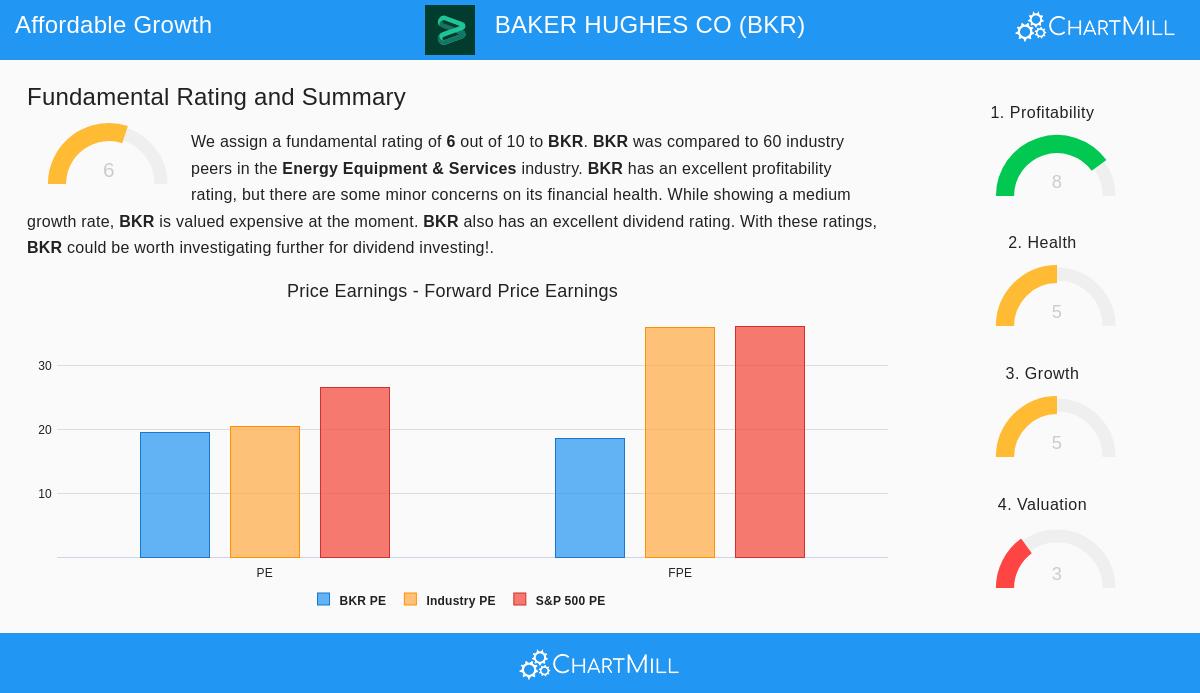

Outside the exact Lynch filter numbers, a wider view of Baker Hughes' fundamental picture gives background. As stated in the detailed fundamental study report, the company gets a total score of 6 out of 10 inside the tough Energy Equipment & Services field.

The report points out several positives that match a long-term investment view:

- Very Good Profitability: BKR gets an 8 out of 10 for profitability, with high scores for its Return on Invested Capital (11.19%) and getting better profit margins.

- Reliable Dividend Picture: The company earns a 7 out of 10 for dividends, backed by a steady 10+ year history of payments, a maintainable payout ratio, and a yield that matches well with the wider market.

- Sufficient Financial Condition: The health score is a middle 5. While the company keeps a careful debt amount (supporting the strong D/E ratio), experts see some small points about its cash ratios next to field competitors.

The main point for care is price, which scores a 3. The report notes BKR trades at a somewhat high level on some plain measures, though its Price/Earnings ratio is lower than many field rivals and the S&P 500 average. This detailed view highlights the Lynch rule that price is relative and must be studied together with growth and quality.

Fit for GARP Investors

For investors who follow Peter Lynch's growth-at-a-reasonable-price idea, Baker Hughes offers an interesting example. It is not a risky, fast-rising company but a settled industrial firm showing the sort of steady, double-digit earnings growth Lynch valued. The company’s careful balance sheet and high profitability numbers suggest this growth has come from a place of financial soundness, not extreme risk.

The appealing PEG ratio is especially notable, as it suggests the market may not completely credit the company for its past growth results. When joined with a dividend policy that benefits shareholders, the picture is of an established yet expanding business that might build value for steady investors. As Lynch often said, the point is to know the business—here, a top firm in energy technology operating in the global shift to both conventional and new energy supplies—and keep it for the long term.

Finding More Investment Options

The Peter Lynch filter is made to methodically find companies that pass these strict fundamental tests. Baker Hughes is one of the names that currently fits these rules. Investors wanting to see the complete list of passing companies can use the Peter Lynch Strategy filter themselves to find other possible options for a long-term, GARP-focused portfolio.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or an offer to buy or sell any security. The study uses data and a particular investment strategy model; it does not account for your personal financial position, risk comfort, or investment goals. You should do your own complete research and talk with a qualified financial advisor before making any investment choices.