For investors looking for chances where a company's market price may not completely show its basic business condition, a careful value investing method can be a practical structure. This plan involves finding stocks that seem priced low according to basic measures, while making sure the company has the financial soundness and earnings ability to back a possible price improvement. One way to find such options is by searching for companies with good valuation marks that also show acceptable basic qualities in expansion, earnings, and financial soundness.

Axalta Coating Systems Ltd (NYSE:AXTA), a worldwide maker of liquid and powder coatings for the car and factory fields, recently appeared through such a "Decent Value" search. This search focuses on a high basic valuation mark, suggesting the stock is priced cautiously compared to its financial numbers, while needing acceptable marks in other important zones to steer clear of possible "value traps." A look at Axalta's detailed basic report shows why it fits these needs and may deserve more attention from value-focused investors.

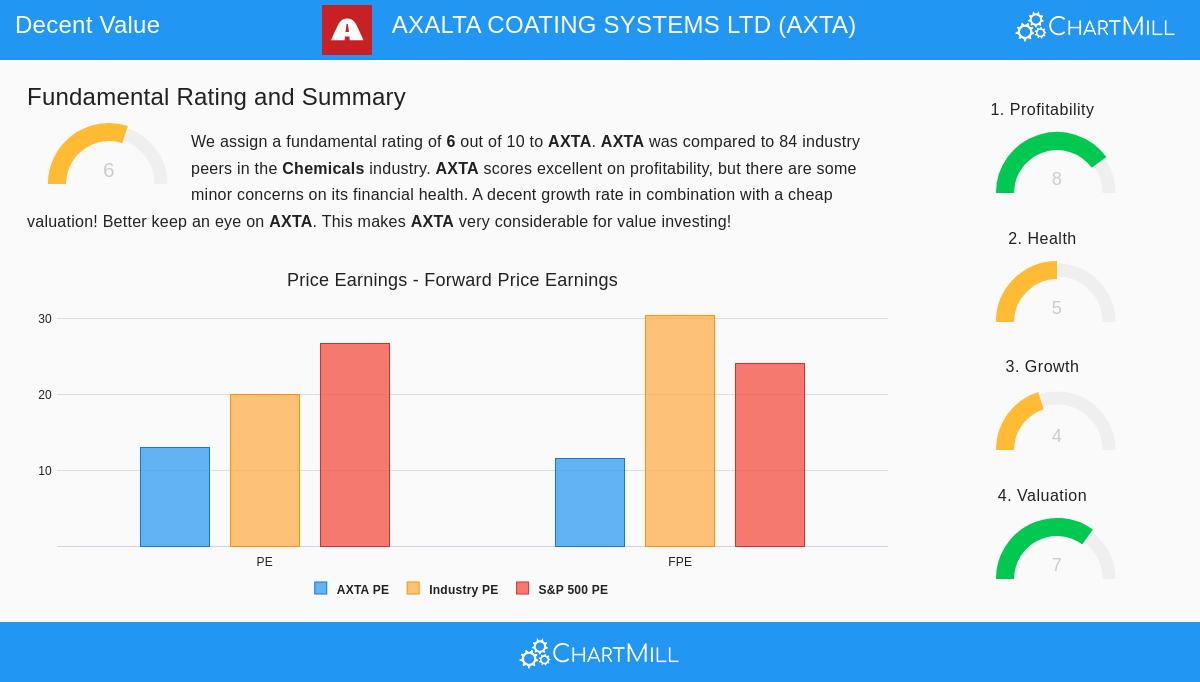

Valuation: The Base of the Idea

The main draw of AXTA for a value search is in its valuation measures, which are the foundation of the value investing idea. The aim is to find a notable difference between price and seen true value, giving a safety buffer. Axalta's basic numbers hint such a difference may be present.

- Good Earnings Multiples: The company's Price-to-Earnings (P/E) ratio of 12.92 is seen as fair on a plain level. More notably, it costs less than about 76% of similar companies in the chemicals field, where the average P/E is close to 19.9. This lower price applies to future measures, with its Price/Forward Earnings ratio of 11.53 also costing less than over 77% of field rivals.

- Low Cost Compared to the Wider Market: When measured against the S&P 500's average P/E of 26.59 and forward P/E of 24.03, Axalta's valuation looks clearly low cost. This wide-market difference points out its possible place as a missed or low-priced company.

- Good Cash Flow and EBITDA Valuation: The study goes past earnings. Axalta's Enterprise Value to EBITDA and Price/Free Cash Flow ratios are also viewed as costing less than most of its field peers, supporting the idea of a cautious market price.

Profitability: Showing Business Condition

A low-cost stock is only a sound investment if the basic business is healthy. Value investing needs this rule to avoid companies that are low cost for a cause. Axalta's firm profitability mark of 8 out of 10 gives key support for the valuation idea, showing the company is basically profitable and effective.

- Steady Earnings Creation: The company has been profitable with positive operating cash flow for the last five straight years, showing business model strength.

- Better Returns on Capital: Important effectiveness measures are solid. Axalta's Return on Equity (ROE) of 19.96% and Return on Assets (ROA) of 5.86% do better than over 90% and 84% of field peers, in that order. Its Return on Invested Capital (ROIC) of 9.96% is also firm and has been getting better.

- Sound and Growing Margins: The company keeps a profit margin of 8.81% (better than 82% of peers) and an operating margin of 15.97% (better than almost 80% of peers), with both margins showing good growth patterns in recent years.

Financial Health: Reviewing the Balance Sheet

Financial health is vital for a value option, as a poor balance sheet can weaken any seen valuation benefit during economic drops. Axalta gets a medium health mark of 5, showing a varied but workable picture. For a value investor, the point is making sure the company is not in trouble, which Axalta's measures mostly affirm.

- Firm Short-Term Cash Availability: The company shows good near-term financial room with a Current Ratio of 2.20 and a Quick Ratio of 1.59, suggesting it can easily meet its short-term debts.

- Controlled Debt with Some Notes: The study notes a high Debt-to-Equity ratio of 1.49, which shows a large use of debt financing and is a zone for watching. However, this is somewhat usual in its capital-heavy field. On the good side, the company has been lowering its share count and bettering its debt-to-assets ratio over time.

- Bankruptcy Risk Seen as Small: An Altman-Z score of 2.38, while not top, suggests small short-term risk of financial trouble and is better than 70% of field peers.

Growth: The Driver for Value Achievement

For a value investment idea to succeed, there needs to be a driver or basic growth to help close the difference between price and value. Axalta's growth mark of 4 is limited but shows hopeful parts that could push future earnings.

- Firm Recent EPS Movement: Earnings Per Share grew by a strong 20.77% over the past year, a good sign of recent business performance.

- Good Future Earnings Path: Experts think EPS growth will keep going at an average rate of about 10% each year in the coming years, showing a speed increase from its longer past pattern.

- Sales Hurdles: The growth picture is balanced by a small year-over-year sales drop of 1.83% and only limited expected future sales growth. This points out that near-term effectiveness gains and margin growth are now bigger drivers than sales increase.

Conclusion

Axalta Coating Systems shows a profile that matches several rules of value investing: it is priced at a lower cost than both its field and the wider market, it runs a steadily profitable business with high returns on capital, and it keeps enough financial health to handle cycles. While its sales growth is low, speeding EPS growth and sound future earnings views give a reasonable way for the market to re-price the stock. It shows the kind of company a "Decent Value" search tries to find, one where low valuation is joined with basically sound business, not basic drop.

For investors curious about seeing other companies that fit similar needs of good valuation along with acceptable basic qualities, you can see the full Decent Value Stocks search on ChartMill.

Disclaimer: This article is for information only and does not make financial advice, a suggestion, or a deal or request to buy or sell any securities. The study is based on data and marks given by ChartMill, and investors should do their own study and talk with a qualified financial advisor before making any investment choices.