In the field of investing, few methods have lasted as long or shown as much success as value investing. Fundamentally, this method looks for companies selling below their inherent worth, decided by examining business fundamentals. The aim is to discover good firms the market has incorrectly priced for now, giving a "margin of safety" for the steady investor. One way to find these opportunities is by filtering for stocks with a good valuation score, meaning they are priced low compared to their finances, while also holding fair ratings in earnings, balance sheet strength, and expansion. This mix points to a company being not only low-priced by numbers, but operationally healthy, possibly sidestepping the risk of a "value trap."

Axalta Coating Systems Ltd (NYSE:AXTA) is a worldwide maker of coatings systems, working for the vehicle sector and many industrial clients. A recent review of the company's fundamentals proposes it might match the outline of a stock priced below its worth, deserving more attention from investors focused on value.

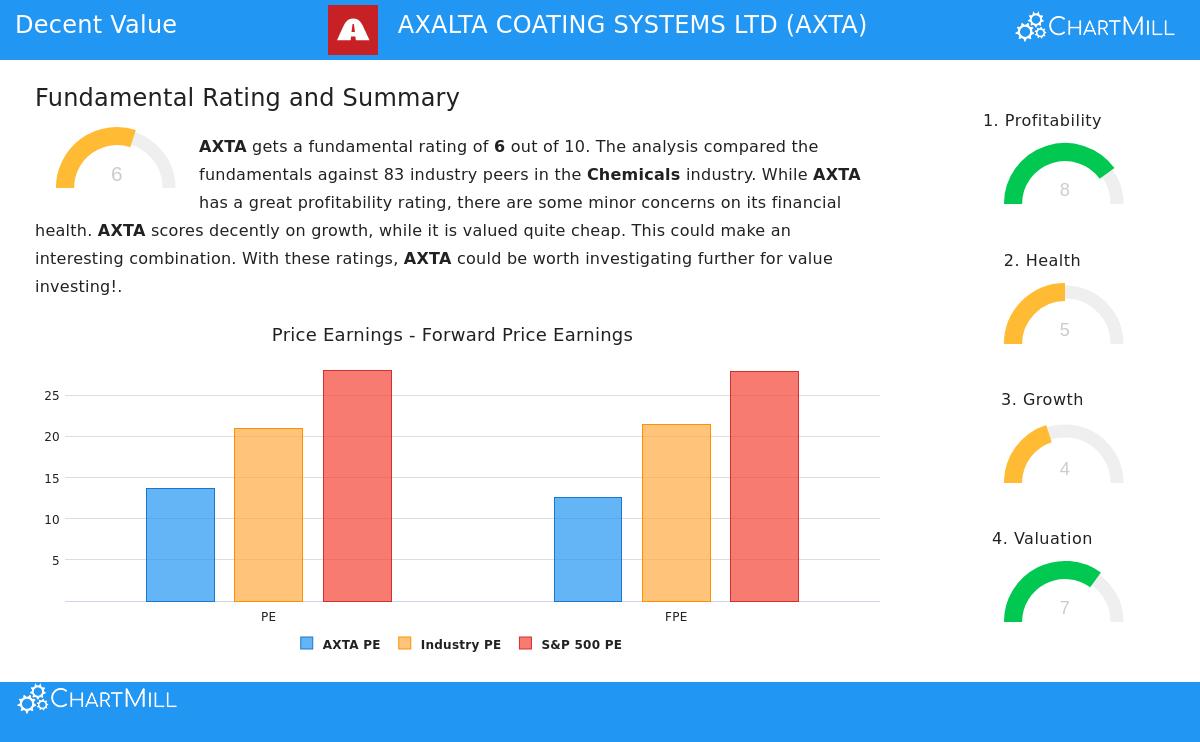

Valuation: The Foundation of the Idea

For a value investor, a good price is the main starting point. The review shows AXTA's valuation is a point of advantage, receiving a score of 7 out of 10. The stock seems low-cost on several important measures against its sector and the wider market.

- Its Price-to-Earnings (P/E) ratio of 13.68 is much lower than the S&P 500 average of 28.06, and it is less expensive than about 82% of similar companies in the chemicals sector.

- The forward P/E ratio of 12.56 shows the same pattern, also resting below the market and sector averages.

- More evidence for the low price are its Enterprise Value/EBITDA and Price/Free Cash Flow ratios, which are more favorable than nearly 70% of sector rivals.

This reduced price offers the possible "margin of safety" that value investors want. While a low multiple by itself is insufficient, it opens a chance if the core business is stable and earns money.

Profitability: Showing Business Strength

A low-cost stock is only a beneficial purchase if the company can produce steady earnings. This is where AXTA does well, scoring a high 8 out of 10 for profitability. The company shows good returns on capital and firm margins, which are vital signs of a lasting market position and effective leadership.

- Good Returns: The company's Return on Equity (ROE) of 19.96% and Return on Invested Capital (ROIC) of 9.96% are strong, doing better than over 90% and 81% of sector peers, in order.

- Firm Margins: AXTA keeps a solid Profit Margin of 8.81% and an Operating Margin of 15.97%, putting it in the higher rank of its sector. Notably, these margins have displayed pleasing improvement in recent years.

For a value investor, this degree of profitability is comforting. It implies the company's low market price is not a sign of weak performance, but instead a possible market mistake. A profitable company trading at a discount is the traditional value investment goal.

Financial Health: Reviewing the Balance Sheet

Financial strength is vital for surviving economic slowdowns and preventing trouble, a main factor for long-term value holdings. AXTA's health score is a middle 5 out of 10, showing a varied situation with both positives and points to watch.

- Liquidity is Sufficient: The company displays acceptable short-term financial room with a Current Ratio of 2.20 and a Quick Ratio of 1.59, suggesting it can manage its upcoming payments.

- Debt is a Factor: The review notes a high Debt-to-Equity ratio of 1.49, which is less favorable than about 76% of its peers. This higher debt is a recognized risk that investors must consider.

Value investing needs a detailed review of risk. While AXTA's liquidity is positive, its debt amount brings a point of care, highlighting the need for the "margin of safety" given by its low price.

Growth: The Route to Realizing Worth

For a stock priced below its worth to achieve its possibility, some expansion is frequently needed to prompt a revaluation by the market. AXTA's growth score is a moderate 4 out of 10, displaying a steady, though not remarkable, path.

- Earnings Growth is Up: The company reported a solid 20.77% rise in Earnings Per Share (EPS) over the last year, and experts predict EPS to keep growing at an average pace near 10% each year.

- Revenue is Steady: While revenue decreased a bit last year, it has shown a small average yearly rise of 3.31% over recent years, with limited growth predicted to continue.

This growth picture backs the value argument. AXTA is not a rapid-growth stock, but it shows an ability for consistent earnings increase, which could help narrow the difference between its present market price and its inherent worth with time.

Conclusion

Axalta Coating Systems offers a situation that fits a number of value investing basics. It is priced low compared to the market and its own sector, while also showing strong profitability and sufficient liquidity. The mix of a low P/E ratio, high returns on capital, and positive earnings growth forms a setting where the market could be valuing the company's lasting earnings capacity too low. The primary item for more examination is its higher debt level, an element value investors would need to watch.

For investors curious about using this "fair value" filter to find other chances, you can review more possible choices with the predefined filter on ChartMill. The complete fundamental review for AXTA, listing all the measures talked about, is found here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on data and ratings provided by third parties. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.