The search for undervalued companies is a central part of disciplined, long-term investing. This method, often called value investing, involves finding stocks that seem to trade for less than their actual worth, based on a full review of their financial condition, earnings, and future possibilities. One way to simplify this search is by using fundamental rating systems that grade companies on important areas. A "Decent Value" screen, for example, looks for stocks with a good valuation rating, meaning they are priced well compared to their fundamentals, while also needing acceptable grades in earnings, financial condition, and expansion. This multi-part review helps sidestep the typical "value trap," where a low-priced stock is inexpensive for a bad cause. Allison Transmission Holdings (NYSE:ALSN) results from such a screen, offering a subject for investors examining the industrial sector.

A Closer Look at Valuation

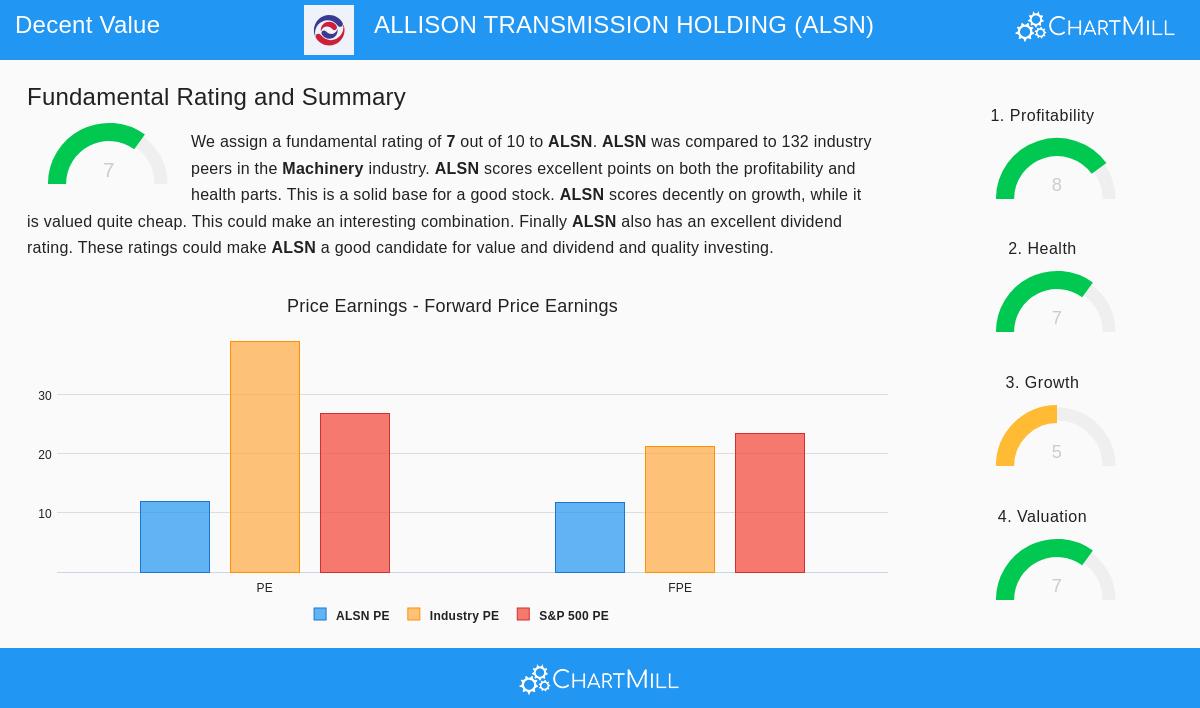

The main attraction for any value investor is a good price. Allison Transmission’s valuation numbers are notable, especially within its field. The company’s fundamental report shows a Valuation Rating of 7 out of 10, pointing to a good price when considered next to its financial results.

- Price-to-Earnings (P/E) Ratio: At 12.01, ALSN’s P/E ratio is much lower than the S&P 500 average of about 26.9. More notably, it is less expensive than almost 95% of similar companies in the Machinery industry, where the average P/E is above 39.

- Forward P/E and Cash Flow: The forward P/E ratio of 11.78 and a good Price-to-Free Cash Flow ratio further support the valuation case, with the company trading at a lower price than most of its industry rivals on these counts.

For a value plan, a low valuation is the starting place, but it must be supported by basic business quality to last. An inexpensive stock with weak fundamentals is a value trap; an inexpensive stock with sound fundamentals may be a chance.

Assessing Financial Condition and Earnings

A solid balance sheet and high earnings are important cushions that give a company the ability to handle economic shifts and pay for future expansion, key points for a long-term value investor. Allison Transmission does well here, with a Health Rating of 7 and a high Profitability Rating of 8.

Financial Condition Points:

- Strong Liquidity: The company shows very good short-term financial strength, with a Current Ratio of 3.82 and a Quick Ratio of 3.06, doing better than nearly 90% of its industry. This shows enough ability to meet its near-term needs.

- Manageable Debt: While the Debt-to-Equity ratio is somewhat high, the more important Debt-to-Free Cash Flow ratio is a sound 3.82, meaning the company could clear all its debt with its cash flow in less than four years, a mark of good solvency.

Earnings Strength:

- High Margins: Allison works with industry-best margins. Its Operating Margin of 31.7% is above every peer in its industry, and a Profit Margin of 22.78% is better than over 98% of rivals.

- Efficient Capital Use: The company creates notable returns on its investments, with a Return on Invested Capital (ROIC) of 15.6% and a Return on Equity (ROE) of almost 38%, both placed in the top group of its field.

This pairing of a strong liquidity position and top-level earnings means the company’s low valuation is not a sign of operational problems. Instead, it hints the market may not fully value a very efficient and financially good business.

Expansion Path and Dividend

Value investing is not only about fixed numbers; it also includes a review of a company’s future possibility. Allison’s Growth Rating is a neutral 5, but a closer view shows a good speed-up. While the last year saw a small drop in revenue and EPS, the longer-term pattern and, more critically, the future view are positive.

- Past & Future EPS: The 5-year historical EPS growth averages a solid 11.1% per year. Analysts expect this to speed up to over 14% each year in the coming years.

- Revenue Speed-Up: In the same way, after modest historical revenue growth, future guesses call for a strong 14.5% yearly rise.

This expected speed-up in both earnings and sales growth is a key part. It suggests the company is not a still value choice but one with a forward motion that could help narrow the difference between its market price and actual worth. Also, the company adds to this with a steady dividend, having a 10-year history of yearly raises and a workable payout ratio, including a part of shareholder return while investors wait for a possible valuation change.

Conclusion: A Good Value Case

Allison Transmission offers a multi-part case for investors using a disciplined value method. It is not just a numerically inexpensive stock. It is a company trading at a large discount to both the wider market and its own industry, yet it is supported by high earnings, good financial condition, and a speeding-up expansion outline. This match, where good valuation meets fundamental quality, is exactly what screens like the "Decent Value" filter try to find.

For investors wanting to review other companies that fit similar standards of sound valuation, condition, earnings, and expansion, more study can be done using the Decent Value Stocks screen on ChartMill.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented is based on data provided and should not be the sole basis for an investment decision. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.