For investors looking for a dependable source of passive income, a systematic selection process is needed to distinguish truly lasting dividend payers from risky high-yield stocks. One useful technique involves selecting for stocks that have a high dividend score and are also supported by good basic business condition and earnings. This method favors companies with the monetary resources to keep and possibly raise their payments over time, instead of only selecting for the largest stated yield. A stock that recently appeared from such a filter is Allison Transmission Holdings (NYSE:ALSN).

Dividend Profile: A Balance of Yield and Growth

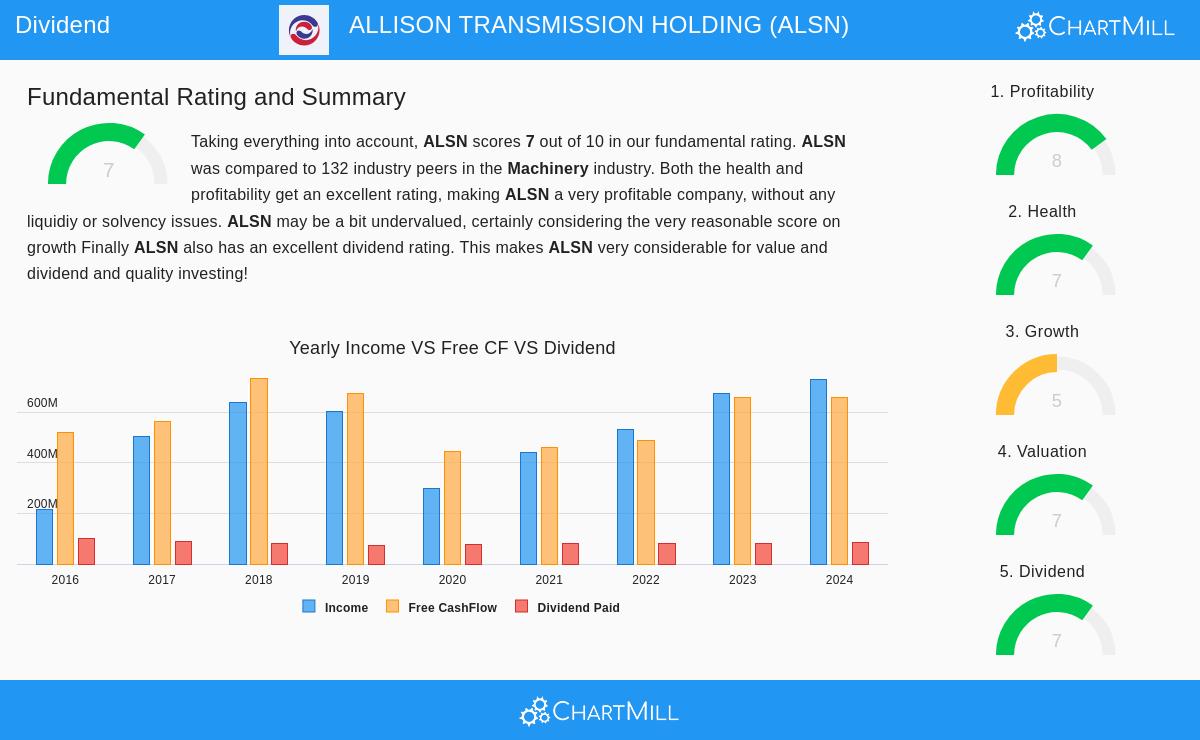

Allison Transmission makes a strong argument for dividend-oriented investors, receiving a solid ChartMill Dividend Rating of 7. The company's attraction comes not from a very large yield, but from a mix of consistency, increase, and durability.

- Yield and Comparison: The stock provides a yearly dividend yield of 1.07%. This is higher than the industry average of 0.98%, but it is lower than the wider S&P 500 average. This is an important detail for the selection method: it steers clear of the very high yields that can indicate basic business trouble or a payment ratio that is too high to maintain.

- Track Record and Growth: The company has an excellent dividend history, having paid and raised its dividend for at least ten straight years. This shows a dedicated practice of giving capital back to shareholders. More notably, the dividend has increased at a yearly rate of about 10.94% over this time, providing a strong mix of income and appreciation.

- Payout Durability: The durability of this dividend is likely its most notable characteristic. Allison Transmission uses only 12.88% of its earnings for dividends, a very low and careful payout ratio. This keeps most profits available to be put back into the business, used to reduce debt, or support future dividend raises. The basic report also states that earnings are increasing quicker than the dividend, supporting the lasting nature of the payment.

Basic Strength: Earnings and Monetary Condition

The selection standards need more than just a good dividend narrative; they require a sound base. Allison Transmission performs here too, with good scores in both earnings and monetary condition, which are vital for the dividend's continuation.

Earnings (Rating: 8) The company's activities are very efficient and profitable. Important measures are much better than industry counterparts:

- Return on Equity (ROE): 37.97%, better than 96% of the machinery industry.

- Profit Margin: 22.78%, higher than 98% of industry counterparts.

- Operating Margin: An industry-best 31.70%.

This excellent earnings ability creates the necessary cash to finance activities, invest for later, and, importantly, maintain the dividend without pressuring the monetary statement.

Monetary Condition (Rating: 7) A company's capacity to endure economic downturns is critical for dividend investors. Allison Transmission displays clear strength in cash availability, although it has a middling amount of debt.

- Good Cash Availability: The company performs well with a Current Ratio of 3.82 and a Quick Ratio of 3.06, showing more than enough means to meet immediate liabilities and doing better than almost 90% of its industry.

- Debt Handling: While the Debt/Equity ratio is somewhat high at 1.30, the company's large free cash flow offers a good offset. Its Debt to Free Cash Flow ratio of 3.82 is viewed as acceptable, indicating it could eliminate all its debt in less than four years using its present cash generation—a signal of good debt position.

Price and Growth Prospects

From a price standpoint, the stock seems fairly valued, trading at a P/E ratio of 12.00, which is less expensive than 94% of its industry and much lower than the S&P 500 average. This price, combined with its high earnings, can be interesting for investors focused on value and dividends.

The growth situation is varied but indicates encouraging speed. While recent year-over-year results for sales and EPS were a little negative, the longer-term direction is positive, with EPS increasing at an 11.1% yearly rate over recent years. More significantly, analysts forecast a notable improvement, with expected EPS growth of 14.03% and sales growth of 14.49% each year in the next few years.

Conclusion

Allison Transmission represents the kind of company a systematic dividend selection method tries to find. It passes over a conspicuous, high present yield for a more lasting set of features: an increasing dividend supported by a ten-year history, a very low and durable payout ratio, and, most critically, a base of excellent earnings and strong cash availability. This mix indicates the company is in a good position to keep providing returns to shareholders through different market conditions.

For investors wanting to examine other companies that fit similar standards of good dividends, earnings, and monetary condition, you can see the full selection results here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on data and fundamental reports provided by ChartMill, which relies on past performance and analyst estimates. Investors should conduct their own research and consider their individual financial circumstances before making any investment decisions.