The Rundown

- The Dow (DJI | +0.11%) eked out a modest gain while the S&P 500 (SPX | -0.39%) and Nasdaq (COMP | -0.73%) closed in the red, weighed down by tech and semiconductor weakness.

- WTI crude surged 3.25% to $102.88/barrel, its highest close since July 2022, as Middle East tensions showed no real sign of easing.

- Fed Chair Jerome Powell signaled a "wait and see" approach to oil-driven inflation, sending the 10-year Treasury yield down roughly 10 basis points to 4.34%.

- Memory chipmakers extended their brutal selloff tied to Google's TurboQuant compression breakthrough.

- Bill Ackman's Sunday night X post calling Fannie Mae and Freddie Mac "stupidly cheap" triggered one of the most dramatic single-day moves of the year.

The Iran Wildcard Refuses to Fold

Stocks kicked off Monday in positive territory, the Dow gained as much as 0.9% at the open, but those gains proved short-lived. The problem, as it has been for weeks, is the oil market and the geopolitical noise surrounding it.

President Trump has raised the prospect of the U.S. taking Iran's oil and seizing key fuel hub Kharg Island TheStreet, while simultaneously posting on Truth Social that serious negotiations with a "new, reasonable" Iranian regime are making progress. The mixed signals are exhausting and the market is pricing in every twist and turn.

WTI crude settled up 3.25% at $102.88 per barrel, its highest close since July 2022. Meanwhile, Brent futures, at $112.78, are now tracking toward what looks like the largest monthly rise ever, up some 55% in March alone.

I'll say it plainly: as long as the Strait of Hormuz remains a geopolitical football, energy is the only sector worth owning in the near term, and that's not a particularly comfortable place for diversified portfolios to be.

Powell Chooses Patience and Markets Mostly Liked It

The most market-moving non-event of the day was Federal Reserve Chair Jerome Powell's appearance at Harvard University. Powell said he thinks interest rates are appropriate given current conditions, noting that "we're facing events in the Middle East which will certainly affect gas prices," and that policy is "in a good place for us to wait and see how that turns out."

More importantly, he pushed back on the idea of raising rates to fight an oil shock. "By the time the effects of a tightening in monetary policy take effect, the oil price shock is probably long gone, and you're weighing on the economy at a time when it's not appropriate," he said, adding that the tendency is to "look through any kind of a supply shock."

That was exactly what the bond market needed to hear. The 10-year Treasury yield fell roughly 10 basis points to 4.34%. The probability of a rate cut by year-end also shifted meaningfully, Fed Funds futures for December are now pricing in a roughly 19.5% chance of one rate cut by year-end, compared to just 3% on Friday.

Powell's term expires in mid-May, and his nominated successor Kevin Warsh is widely seen as more rate-cut-friendly, which adds yet another layer of uncertainty to the Fed picture heading into Q2.

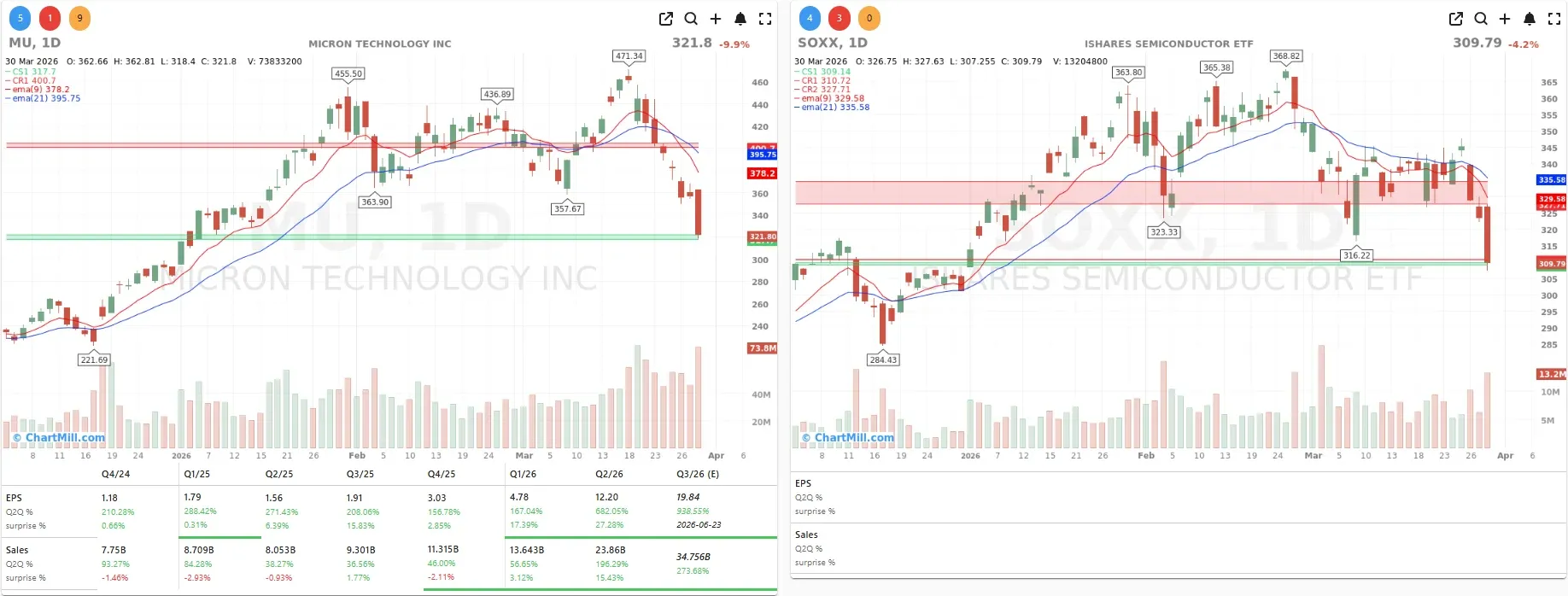

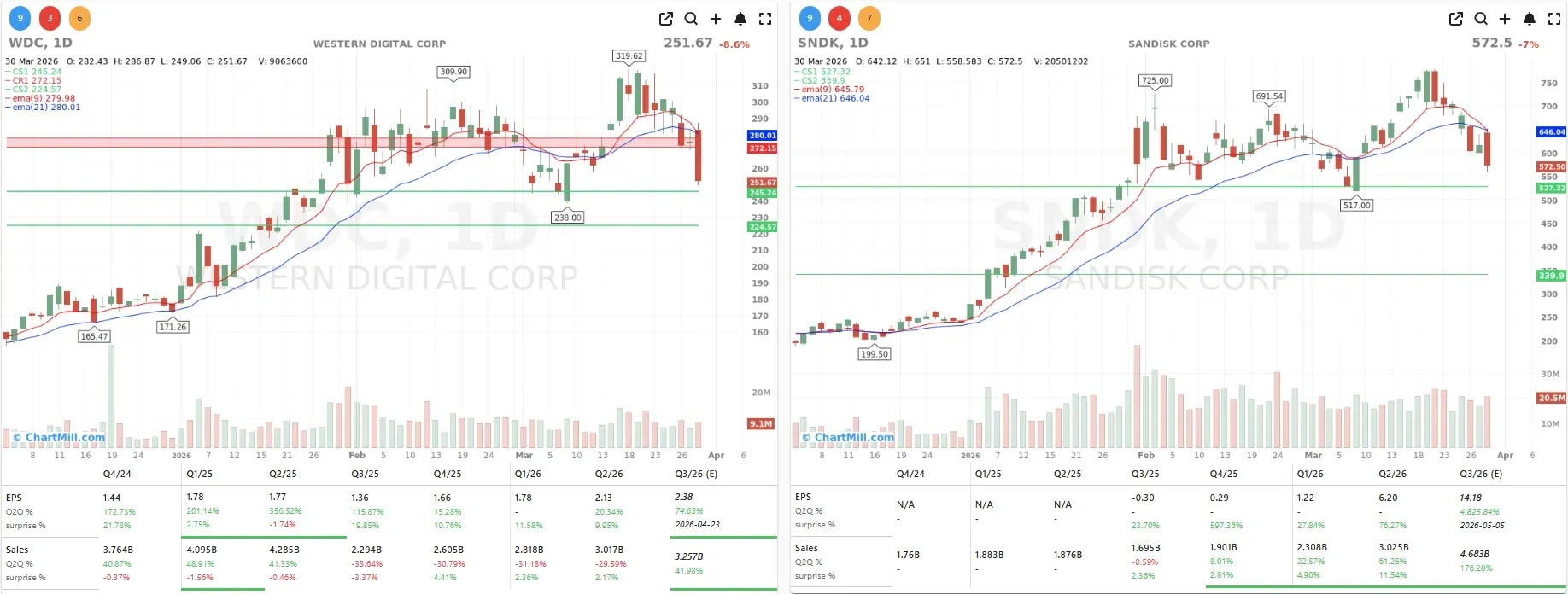

The Memory Chip Massacre Continues

Here's where it really gets painful if you've been riding the AI chip wave.

Shares of Micron were off nearly 10% on Monday and are now barely in positive territory for the year after being up more than 60% as of mid-March. In the last eight trading sessions, Micron has fallen over 30%.

The culprit is Google's TurboQuant algorithm, a compression breakthrough that, at least in theory, could slash the amount of memory needed to run large language models. The PHLX Semiconductor Index (SOXX | ▼4.23%) closed below its 100-day moving average for the first time since last spring's tariff "liberation day" selloff.

Micron (MU | ▼9.92%) is now trading at $357.22 against a Wall Street consensus price target of $527.60, a gap of roughly 47%, while 38 of 43 analysts still rate the stock Buy or Strong Buy. The company has guided for $33.5 billion in Q3 FY2026 revenue and has its entire 2026 HBM supply already sold out.

At 7x forward earnings with that kind of backlog, the selloff looks to me like a fear trade that's overshot the fundamentals. But sentiment is a powerful force, and for now the tape doesn't care about fundamentals.

Western Digital (WDC | ▼8.67%) and SanDisk (SNDK | ▼7.04%) suffered similar damage.

Lam Research (LRCX | ▼5.43%) also declined sharply as the semiconductor sector broadly absorbed the pressure.

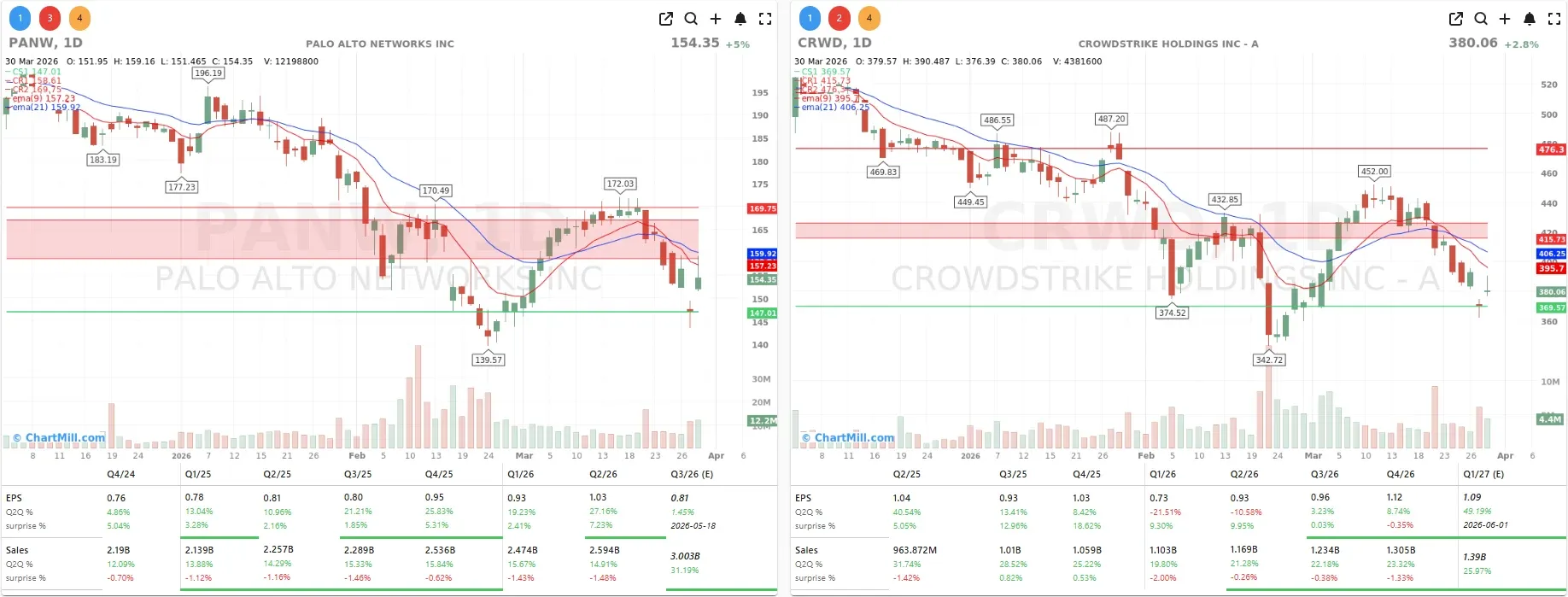

Palo Alto Gets a CEO Boost and Drags Cybersecurity Higher

There's a notable contrast developing within tech right now. While memory names are getting hammered, the cybersecurity space is quietly finding its footing.

CrowdStrike (CRWD | ▲2.84%) rose more than 4% after Wolfe Research upgraded the stock to outperform, arguing that CrowdStrike will benefit from increased cyber risks from AI rather than have its business model disrupted by it.

Morgan Stanley also named the stock a top pick. CrowdStrike had been down more than 21% year-to-date heading into Monday.

The bigger story in the sector is Palo Alto Networks (PANW | ▲4.99%). After getting caught in last week's Anthropic-related AI selloff, CEO Nikesh Arora disclosed he personally purchased $10 million worth of company stock on Friday.

That kind of insider conviction is a hard signal to ignore, and the market agreed, shares bounced 5% on the news.

Sysco's Mega Deal Sends Shares Into Freefall

Not all acquisitions are greeted with applause. Sysco (SYY | ▼15.28%) was Monday's most notable loser in the S&P 500, falling more than 15% after announcing the $29.1 billion acquisition of privately held Jetro Restaurant Depot.

The deal is expected to close in Sysco's fiscal third quarter of 2027 and was described by management as "immediately accretive."

The problem? Sysco itself has a market cap of around $39 billion, and it plans to finance the deal with $21 billion in new and hybrid debt, that's an enormous leverage load for a food distribution business operating in an already-margin-thin industry. Investors focused on the balance sheet risk, and I think that's the right call here.

Ackman Moves Fannie and Freddie, But Read the Fine Print

The most dramatic individual stock story of the day was actually in the OTC market.

Fannie Mae surged 51% in Monday trading, its steepest one-day jump since August 2009, while Freddie Mac rallied 47%, its biggest single-day climb since March 2013.

The catalyst? A late Sunday post on X from Pershing Square's Bill Ackman, who called both mortgage giants "stupidly cheap" and suggested they could rise tenfold and potentially do so quickly. Fortune "The Big Short" investor Michael Burry promptly amplified the message.

There's context here that's worth unpacking. Ackman's firm is the single largest common shareholder in both companies, holding more than 210 million shares combined. Fortune Monday also happened to be the last trading day of Q1, which is when hedge fund performance numbers get locked in. Despite Monday's rally, the two stocks remain down around 60% from a mid-September peak and the path to privatization remains murky at best.

Michael Burry himself doesn't see an IPO for these mortgage companies until at least 2027.

The potential upside case is real if the conservatorship ever ends. The asymmetry argument has merit. But this is event-driven speculation more than conventional investing. Anyone chasing the Monday pop without understanding the regulatory and political complexity involved is taking on risks they may not fully appreciate.

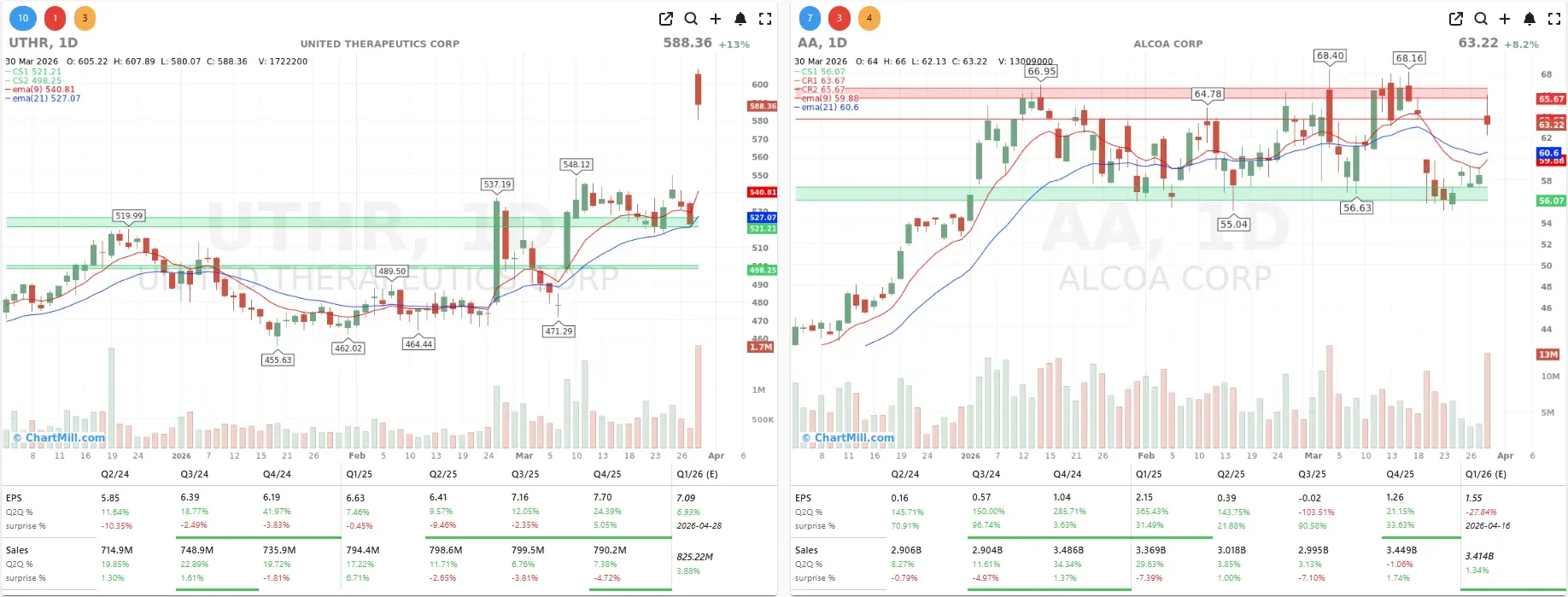

lcoa and United Therapeutics: Bright Spots Worth Noting

Alcoa (AA | ▲8.23%) rallied more than 8% as aluminum prices surged more than 4.5% after Iranian missile strikes hit critical aluminum production infrastructure in the Middle East. This is a clear example of the war's second-order commodity effects, we're not just talking about oil anymore.

United Therapeutics (UTHR | ▲12.53%) also had a standout session, hitting a 52-week high on positive Phase 3 results for Tyvaso, its lead drug currently approved for two forms of pulmonary hypertension. The company is seeking an accelerated FDA review to expand the drug's label into idiopathic pulmonary fibrosis, a progressive and currently underserved condition. A successful label expansion here would be a significant commercial event.

Looking Ahead: A Week Packed with Labor Data

The week ahead carries additional weight.

Nike and McCormick & Company are both reporting earnings on Tuesday, followed by Conagra Brands (CAG) on Wednesday.

The JOLTS job openings data drops Tuesday, ADP private payrolls on Wednesday, and the official nonfarm payrolls report on Friday, though markets will be closed for Good Friday.

That means today's close (Tuesday, March 31) effectively ends the trading week for practical purposes before the big macro number lands.

The labor market data will be closely watched for any signs that the oil shock and broader uncertainty are beginning to filter through into hiring decisions. So far, the data has held up, but that was before $100+ crude became the baseline.

Conclusion

Monday's session was a microcosm of everything that's been wrong with this market in March: conflicting geopolitical signals, a Fed stuck in wait-and-see mode, tech getting repriced lower, and sentiment swinging violently on a single social media post. The S&P 500 has now logged its fifth consecutive weekly decline, its longest losing streak since early 2022.

The market's fate remains tethered to the Strait of Hormuz. A genuine ceasefire or de-escalation would likely trigger a sharp relief rally across most sectors.

Until then, I'd expect continued volatility, with energy and utilities as relative safe harbors and the semiconductor sector remaining a show-me story until the TurboQuant narrative either fades or gets confirmed by data. Tuesday's open and today's final Q1 close will be the next test.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Market Breadth Update: Selling Pressure Eases, but Internal Damage Keeps Building