For investors looking for chances where the market price may not completely show a company's actual worth, a methodical value investing method can be a useful rule. This method focuses on finding stocks selling for less than their true value, frequently shown by good valuation measures, while confirming the business is fundamentally strong. A "decent value" screen uses this idea by selecting for companies with good valuation scores that also show acceptable health, profitability, and growth, a mix intended to steer clear of "value traps" where a low-priced stock is inexpensive for a bad reason.

One company that appears from this type of screen is Zimmer Biomet Holdings Inc (NYSE:ZBH), a worldwide head in musculoskeletal healthcare. The company's most recent fundamental analysis report indicates its stock makes a strong case for value-focused investors, mixing a very low price with a steady, profitable core business.

A Strong Valuation View

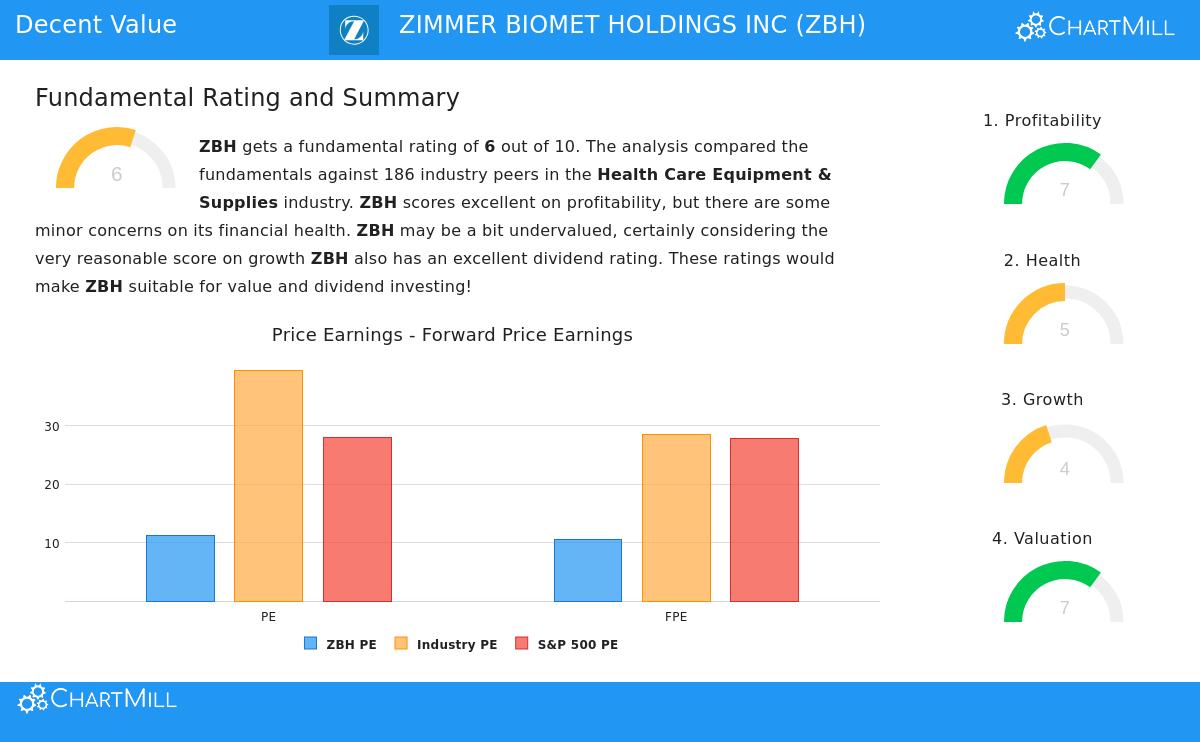

The central idea of value investing is buying a dollar of assets for fifty cents. Zimmer Biomet's valuation measures strongly hint such a discount could exist. The company's ChartMill Valuation Rating is a solid 7 out of 10, showing it is priced low compared to its financial situation.

- Price-to-Earnings (P/E) Ratio: At 11.11, ZBH's P/E ratio is much lower than both its industry average (about 39.5) and the wider S&P 500 average (27.92). It is less expensive than 94% of similar companies in the Health Care Equipment & Supplies sector.

- Forward P/E Ratio: The view stays good looking forward, with a forward P/E of 10.48, which also puts it in the least expensive part of its industry.

- Other Multiples: The valuation strength continues to other measures. The company's Enterprise Value to EBITDA and Price to Free Cash Flow ratios are more favorable than about 93% of industry rivals.

For a value investor, these numbers are the first point of interest. They show the market is using a cautious, possibly negative, multiple on the company's earnings and cash flow, possibly creating a margin of safety, a buffer between price and estimated true value that is key to the method.

Evaluating Financial Health and Profitability

A low valuation by itself is insufficient; Benjamin Graham stressed the need for a company's financial soundness. A low price combined with poor health can be a value trap. Zimmer Biomet's ChartMill Health Rating is an average 5, indicating a varied but acceptable financial state.

Positive points contain a good Current Ratio of 2.43, showing sufficient ability to meet near-term debts, and a Debt-to-Equity ratio of 0.59, which displays reasonable borrowing compared to some peers. However, the report mentions some points of attention, like a Return on Invested Capital (5.73%) that is now under the company's cost of capital, hinting at area for betterment in value creation efficiency.

The profitability picture, though, is where Zimmer Biomet stands out and helps address health points. With a ChartMill Profitability Rating of 7, the company shows its capacity to produce returns.

- Good Margins: The company keeps very good margins, with a Gross Margin of 71.44% (more favorable than 80% of peers) and an Operating Margin of 19.10% (more favorable than 91% of peers).

- Steady Returns: Its Return on Assets (3.43%) and Return on Equity (6.31%) both do better than almost 80% of the industry, showing efficient use of its asset and shareholder equity base.

- Cash Flow Positive: Importantly, ZBH has produced positive operating cash flow in each of the last five years, giving the means for operations, debt payments, and shareholder returns.

This profitability is vital for the value argument. It hints the company is not a failing business but a cash-producing operation that is being valued as if it were.

Growth and Income Points

Strict value stocks are occasionally linked with no-growth businesses. Zimmer Biomet's growth picture, rated a 4, shows small but positive movement. Revenue increased 5.47% over the last year, and earnings per share growth is projected to rise to about 5.5% each year in the next few years. This slow but consistent growth, especially in the stable healthcare sector, backs the idea of a steady true value.

Also, the company provides a dividend yield of 1.04%, which, while under the S&P 500 average, is meaningful next to its industry's 0.20% average. With a maintainable payout ratio of 23.70% and a 10-year history of consistent payments, it adds an income element that is interesting for value investors looking for total return and a real return of capital while anticipating a possible price adjustment.

Conclusion

Zimmer Biomet Holdings Inc shows a picture that matches important value investing ideas: it is valued at a large discount to the market and its industry, it runs a profitable business with good margins, and it keeps sufficient financial health while giving a consistent dividend. The small growth projections and minor financial points of attention are likely already factored into its low valuation multiples. For investors screening for "decent value", companies that are inexpensive but not unsound, ZBH justifies further review as a possible option where the market's present price may not completely reflect the company's lasting worth.

Find other stocks that fit this "Decent Value" picture by using the pre-configured screen on ChartMill.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion to buy or sell any security, or a support of any investment method. Investors should do their own study and talk with a qualified financial advisor before making any investment choices.