For investors looking to balance the search for growth with a degree of caution, the Growth at a Reasonable Price (GARP) method presents a persuasive middle path. This method looks for companies that are increasing their earnings and revenue faster than average but are not priced at the extreme levels often seen with aggressive growth stocks. The aim is to not pay too much for future promise while still taking part in a company's progress. Filtering for stocks that show good growth foundations, steady earnings, and sound finances, while also having a fair price, can point to these "affordable growth" possibilities.

Wheaton Precious Metals Corp. (NYSE:WPM), a top precious metals streaming company, recently appeared from this kind of filtering process. The company's approach involves giving early funding to mining companies for the ability to buy a part of their future precious metal output at set, low prices. This framework gives WPM notable exposure to commodity prices without the direct operational hazards and large costs of mining. An examination of its fundamental analysis report shows a picture that fits the affordable growth idea well.

Strong Growth Path

The center of any growth investment is a clear and lasting increase in business size and earnings. Wheaton Precious Metals does very well here, receiving a high Growth score. The company is not just stating future growth, it is achieving it now.

- Notable Recent Results: In the last year, WPM posted strong growth, with Earnings Per Share (EPS) rising 61.01% and Revenue going up 50.33%. This shows solid operational speed.

- Steady Past Growth: Reviewing the last several years, the company has built a good history, with EPS increasing at a typical yearly rate of 21.22%.

- Positive Future Forecasts: Analyst projections indicate this growth is likely to persist. EPS is forecast to rise more than 22% each year in the near future, while Revenue growth is expected to rise to about 14.31% per year.

This mix of good past results and an optimistic future view is key for a GARP method, as it gives proof that the company's growth is part of its business approach, not a short-term event.

Price Assessment

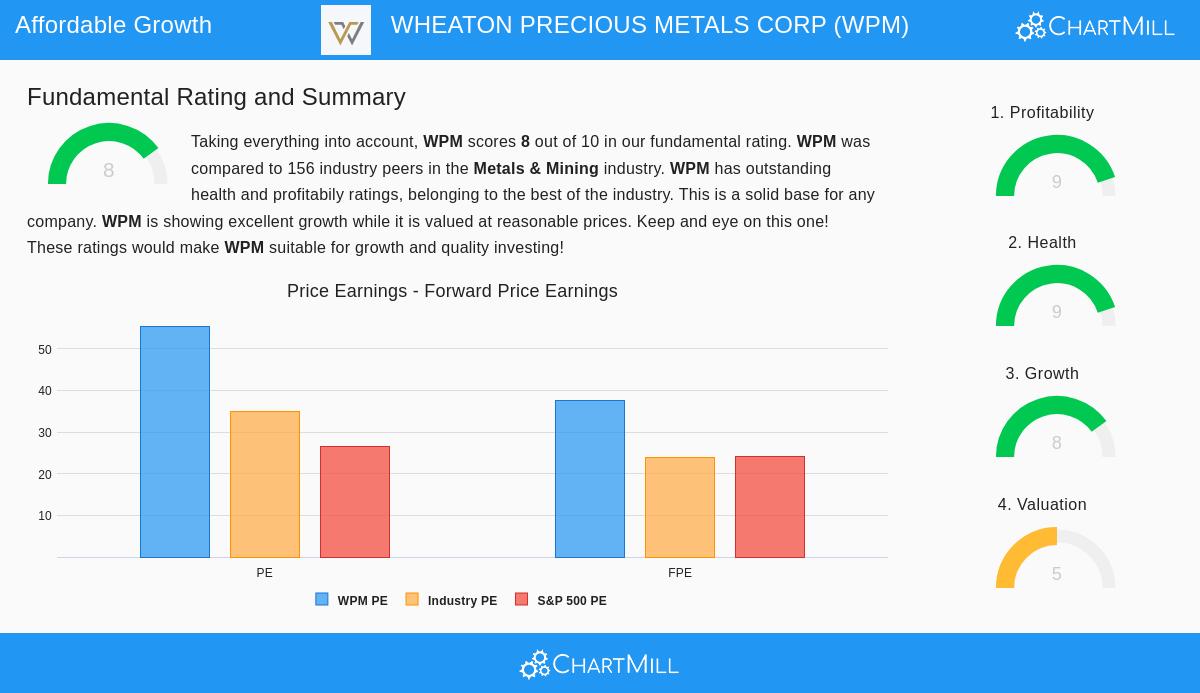

While growth is important, paying a suitable price for it is what makes growth "affordable." WPM's Price score shows a detailed view. On its own, common measures suggest the stock is not low-cost. Its Price-to-Earnings (P/E) ratio is high next to the wider S&P 500. However, price must be judged alongside the company's standout traits.

- Growth Adjustment: The important measure here is the PEG ratio, which changes the P/E ratio for projected earnings growth. WPM's low PEG ratio shows its current price may be fair when its high growth rate is considered. The market is paying for growth that is still ahead, not growth that is finished.

- Sector and Quality Comparison: WPM's P/E ratio is similar to other companies in the Metals & Mining sector. Also, its higher price can be partly explained by its better business approach and financial measures compared to standard miners. The company's very good earnings and clean financial standing (covered next) often receive a higher multiple, as they lower investment risk.

- Cash Generation View: From a cash production angle, the stock seems more fairly priced. Its Price-to-Free Cash Flow ratio is lower than most of its sector peers, emphasizing how well its streaming model turns revenue into cash.

Supported by Sound Foundations

A growth narrative is only lasting if based on a firm base. This is where WPM's picture becomes especially interesting for careful growth investors. The company has top scores for both Earnings and Financial Standing.

Earnings: WPM works with very high margins, a direct advantage of its low-cost streaming contracts. Its Profit Margin of 54.72% and Operating Margin of 63.50% are in the highest group of its sector. Returns on Assets, Equity, and Invested Capital are all good and getting better, showing effective use of money to produce profits.

Financial Standing: The company's balance sheet is very strong, with almost no debt. Important liquidity ratios, like the Current Ratio and Quick Ratio, are very high, giving major financial room and stability. This sound financial condition helps the company's capacity to finance new streaming deals, the driver of its future growth, without excessive pressure.

Conclusion

Wheaton Precious Metals Corp. is a clear example of the kind of company an affordable growth filter seeks. It combines a clear, high-growth path, backed by both recent performance and future projections, with a price that, while not bargain-low, can be understood given its growth speed, better earnings, and very strong balance sheet. For investors, this mix tackles a major problem of growth investing, paying too much for excitement. WPM gives access to the precious metals sector through a high-caliber, growth-focused business without the operational hazards of mining, all while keeping financial measures that reduce potential loss.

The hunt for companies mixing growth and price continues. You can review other possible options that fit similar standards using our Affordable Growth stock screener.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation to buy or sell any security, or an endorsement of any investment strategy. Investors should conduct their own research and consider their individual financial circumstances before making any investment decisions. The fundamental data and ratings referenced are provided by ChartMill and are subject to change.