For investors looking to balance the search for growth with a degree of caution, the Growth at a Reasonable Price (GARP) method provides a solid middle path. This method tries to find companies that are increasing their earnings at a good rate, but whose stocks are not sold at very high prices. It avoids the high risk of speculative stocks while aiming for results that beat the general market. One useful way to apply this method is through organized filtering, searching for businesses that show good fundamental growth, sound financial condition, and high profitability, all while being sold at a price that does not completely account for that future possibility. This process helps find what can be called "affordable growth" chances.

Wheaton Precious Metals Corp (NYSE:WPM) recently appeared from such a filtering process, which demanded high marks in growth, profitability, and financial condition, along with a fair valuation mark. As a top precious metals streaming company, WPM gives early financing to mining businesses for the right to buy a part of their future metal output at low, set costs. This distinct business setup gives indirect exposure to commodity prices without the direct mining risks and large spending.

A Notable Growth Picture

The central idea of the GARP method is finding companies with a clear and lasting growth path. Wheaton Precious Metals does very well in this group, receiving a high Growth mark of 8 out of 10. The company's financial details show a strong speed-up in its operations.

- Strong Recent Results: Over the last year, WPM's Earnings Per Share (EPS) rose by a notable 61.01%, while Revenue increased 50.33%. This shows the company is not just growing but doing so more quickly, probably gaining from both more output from its streaming partners and good metals prices.

- Good Past and Expected Growth: The growth is not a single event. WPM has achieved an average yearly EPS growth of 21.22% over recent years. For the future, experts think this speed will keep going, with predicted yearly EPS growth of 22.17% and Revenue growth of 14.31% in the next years. This match between past results and future guesses is a main sign of dependable growth.

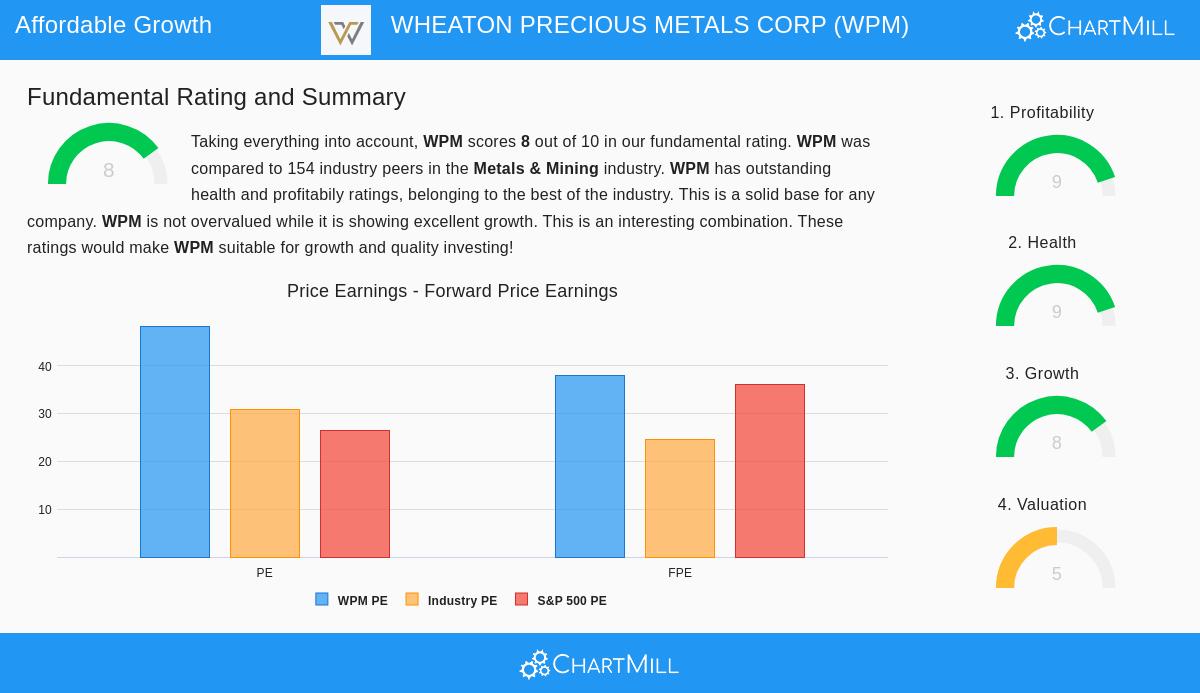

Valuation: A Varied but Fair View

A fair valuation is the important balance in the GARP method, making sure investors do not pay too much for future growth. WPM's Valuation mark of 5 shows a detailed view, with standard measures looking high but the situation giving reason.

- Apparently High Multiples: On first look, WPM sells at a Price-to-Earnings (P/E) ratio of 48.25, which is more than the wider S&P 500 average. Its Forward P/E of 37.94 is also high next to standard value measures.

- Growth Adjustment and Field Setting: The valuation seems more fair when growth is included. The company's low PEG ratio, which changes the P/E for growth, implies the stock could be more evenly priced. Also, WPM's P/E is similar to its field equals in the Metals & Mining group. Most significantly, its Price-to-Free Cash Flow ratio is actually less expensive than almost two-thirds of its rivals, an important note given the cash-producing style of the streaming model. For a GARP investor, this means the market is setting a price that includes growth, but not at an unreasonable high level.

The Base: High Profitability and Financial Condition

Lasting growth cannot be without a solid basic business. This is where WPM's fundamentals are strongest, giving the steadiness that makes its growth believable. The company has top-level marks of 9 for both Profitability and Financial Health.

Profitability Points:

- High margins, with a Profit Margin of 54.72% and an Operating Margin of 63.50%, putting it in the top part of its field.

- Good returns on capital, including a Return on Invested Capital (ROIC) of 12.78%, showing efficient use of shareholder money.

Financial Condition Points:

- A very strong balance sheet with almost no debt (Debt/Equity of 0.00).

- Excellent liquidity, with a Current Ratio over 8, meaning it can meet short-term needs many times.

- An Altman-Z score of 92.23 shows very low bankruptcy danger and better financial steadiness compared to equals.

This mix of high profitability and excellent condition means WPM pays for its growth from within using strong cash flows without needing too much debt or share dilution, a key point for long-term shareholder gains.

Conclusion

Wheaton Precious Metals Corp presents a solid example for the Growth at a Reasonable Price system. The company shows the necessary part of strong, speeding growth in both earnings and revenue, backed by positive expert forecasts. While its main P/E ratio looks high, it is explained within its field and, more importantly, seems fair when its high growth rate, profitability, and financial strength are thought about. The excellent health and profitability marks provide a lasting base, making sure the company has the financial toughness to follow its growth plan and handle economic changes. For investors looking for affordable contact with the precious metals field through a high-quality, growth-focused business, WPM deserves more study.

A full list of these fundamental marks is in the full ChartMill Fundamental Analysis Report for WPM.

Investors curious about finding other companies that match this "Affordable Growth" description can view the set filter here.

Disclaimer: This article is for information only and does not make financial advice, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own study and think about their personal money situation and risk comfort before making any investment choices.