The search for growth stocks at reasonable prices remains a cornerstone of many investment strategies, particularly in a market environment where valuations can become stretched. One method to find such opportunities is through an "Affordable Growth" screening approach, which looks for companies demonstrating strong growth paths without demanding excessive valuation premiums. This strategy balances the pursuit of expansion with fiscal prudence, filtering for stocks with high growth ratings, solid profitability and financial health, and valuations that are not overly expensive. This framework aims to find companies that are growing their earnings and revenue at an attractive rate while still being sensibly priced relative to their prospects and fundamentals.

Wheaton Precious Metals Corp (NYSE:WPM) fits this search, recently appearing from such a screen. As a prominent precious metals streaming company, Wheaton provides upfront financing to mining companies in exchange for the right to purchase a portion of their future metal production at reduced prices. This unique business model provides leveraged exposure to commodity prices without the direct operational risks and capital expenditures associated with mining.

Growth Trajectory

A core belief of the affordable growth strategy is identifying companies with a demonstrably strong and sustainable growth profile. Wheaton Precious Metals Corp performs impressively on this front, earning a high Growth Rating of 8 out of 10. The company's recent performance confirms this strength, with substantial increases in both its top and bottom lines.

- Earnings Per Share (EPS) grew by an impressive 61.15% over the past year.

- Revenue expanded by 50.33% in the same period, indicating very strong operational momentum.

- Looking ahead, analysts project EPS to grow by an average of 18.80% annually, suggesting the positive trend is expected to continue.

This strong historical and projected growth is a primary driver for inclusion in a growth-oriented portfolio, as expanding earnings are a key catalyst for stock price appreciation over the long term.

Valuation Assessment

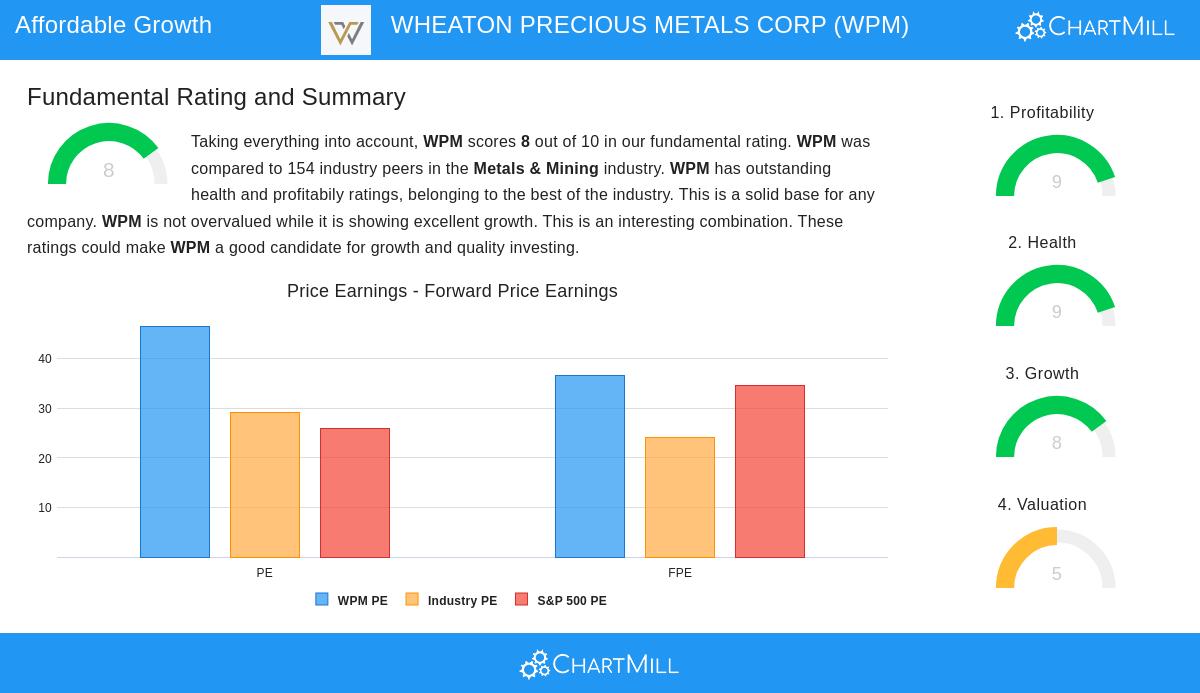

While growth is critical, the "affordable" component of the strategy requires a reasonable valuation. Wheaton Precious Metals Corp holds a Valuation Rating of 5, which positions it as fairly valued within its context. A superficial glance at the Price-to-Earnings (P/E) ratio of 46.50 might suggest expensiveness, especially when compared to the broader S&P 500 average. However, a deeper analysis reveals a more detailed picture that fits with the growth-at-a-reasonable-price philosophy.

- The company's PEG Ratio, which adjusts the P/E ratio for expected earnings growth, indicates a rather cheap valuation, justifying the higher multiple due to the high growth rate.

- Its Enterprise Value to EBITDA is in line with the industry average.

- A majority (62.99%) of its industry peers are more expensive based on the Price/Free Cash Flow ratio.

This valuation profile suggests that while the stock is not deeply undervalued, its price appears justified, and in some metrics, attractive, when its exceptional growth rate and high-quality fundamentals are considered.

Profitability and Financial Health

The affordable growth screen also requires decent profitability and health, which are essential for lowering risk and ensuring the company has the financial strength to sustain its growth. Wheaton performs very well in these areas, having a Profitability Rating of 9 and a Health Rating of 9. These high scores provide a solid foundation that makes the growth story more credible and less speculative.

-

Profitability Highlights:

- Exceptional Profit Margin of 54.72%, outperforming 96.75% of industry peers.

- Strong Return on Invested Capital (ROIC) of 12.78%, placing it in the top tier of its industry.

- Consistently profitable with positive cash flows over the past five years.

-

Financial Health Highlights:

- A clean balance sheet with virtually no debt, reflected in a Debt/Equity ratio of 0.00.

- A very high Current Ratio of 8.09, indicating ample liquidity to meet short-term obligations.

- An Altman-Z score of 89.64 signals extremely low bankruptcy risk.

These characteristics are crucial for the strategy because they indicate that the company's growth is built on a stable, efficient, and low-risk financial base, reducing the potential for unforeseen setbacks.

In summary, Wheaton Precious Metals Corp presents a strong case for investors seeking affordable growth. The company combines a powerful growth engine, evidenced by surging earnings and revenue, with a valuation that can be considered reasonable given its growth prospects and exceptional underlying quality. Its best-in-class profitability and very solid financial health further lower the risk of the investment, making it a notable candidate that fits the specific criteria of a growth-at-a-reasonable-price approach. A more detailed breakdown of these fundamental factors is available in the full fundamental analysis report.

For investors interested in finding other companies that meet similar criteria of strong growth, reasonable valuation, and sound fundamentals, further results can be explored using the Affordable Growth stock screen.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The opinions expressed are based on current data and may change. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.