For investors looking for chances where the market price may not completely show a company's basic value, a methodical screening process can help find possible candidates. One method is to search for stocks with good fundamental valuation scores, meaning they are priced cautiously compared to important financial measures, while also holding acceptable scores in profitability, financial condition, and growth. This mix tries to find companies that are not just low-priced, but low-priced without a clear cause, a possible sign of an undervalued case where good business basics are briefly not seen by the market.

Using this "acceptable value" screen highlights Winnebago Industries (NYSE:WGO). The recreational vehicle and marine products maker shows a case where good valuation measures meet a strong financial standing and forecasts for an earnings recovery, making it a stock deserving of more study for investors focused on value.

Valuation: The Foundation of the Idea

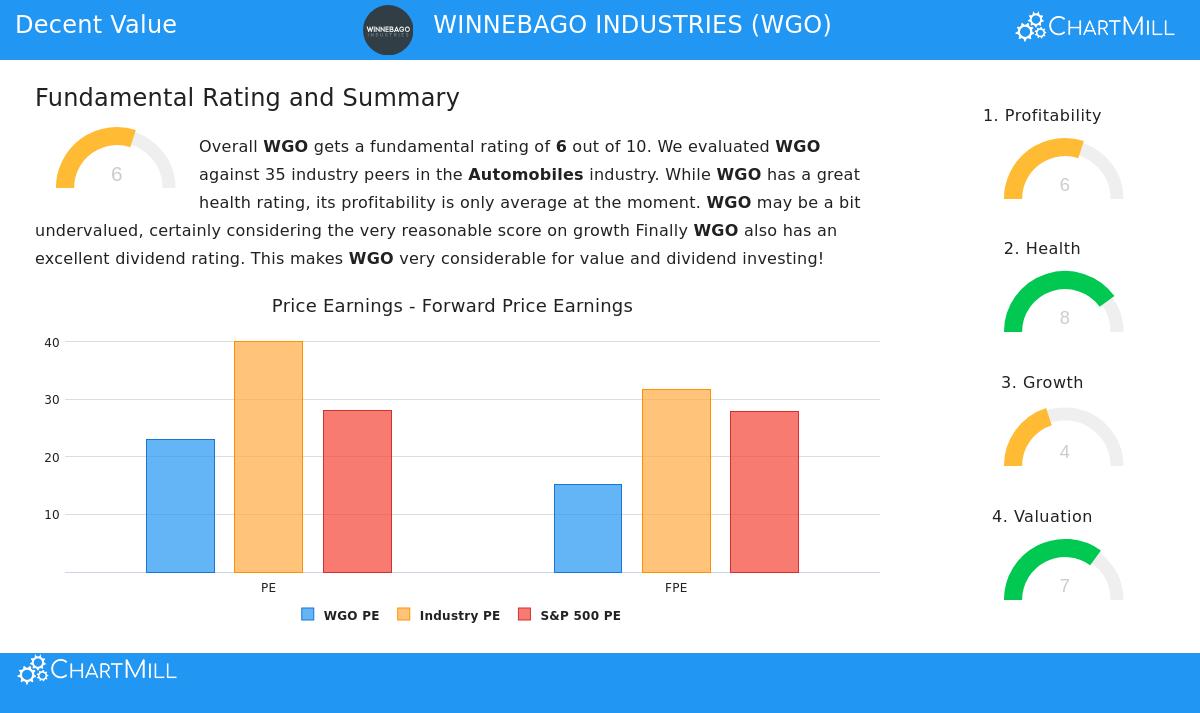

The main attraction of WGO is its valuation score of 7 out of 10, which is the main filter for this screen. A detailed view of the fundamental analysis report shows several measures backing this view:

- Good Relative Value: While its standard Price-to-Earnings (P/E) ratio of 22.94 may appear high alone, it is much lower than 82.9% of similar companies in the Automobiles industry, where the average P/E is above 40.

- Forward-Looking Measures Are Strong: More significantly, its Price-to-Forward Earnings ratio of 15.22 is lower than 80% of industry rivals and is well under the S&P 500 average. Its Enterprise Value-to-EBITDA and Price-to-Free Cash Flow ratios also compare well against most of the industry.

- Growth Adjustment: The low PEG ratio, which changes the P/E for estimated growth, shows the current price may not include expected future earnings increase.

For a value investor, these measures are important. They look for a margin of safety, a gap between the price paid and their calculation of real value. WGO’s valuation scores imply the market is valuing it at a reduction compared to both its industry and its own future earnings possibility, offering a possible beginning for that safety margin.

Financial Health: A Solid Base

A low-priced stock is only a beneficial opportunity if the company is financially stable. Value traps frequently come from purchasing troubled businesses with poor balance sheets. WGO’s financial condition score of 8 out of 10 reduces much of this worry.

- Good Solvency: The company has an Altman-Z score of 3.78, showing a very small short-term chance of financial trouble and doing better than over 91% of its industry. Its Debt-to-Equity ratio of 0.44 shows a careful balance sheet.

- Sufficient Liquidity: A Current Ratio of 2.69 indicates WGO has more than enough immediate assets to meet its immediate debts, a signal of operational strength.

- Controllable Debt: The Debt to Free Cash Flow ratio of 3.98 is seen as good, meaning the company could pay off all its debt with less than four years of cash flow.

This strong financial condition is necessary for the value investing plan. It gives the company the steadiness to handle economic changes and industry slowdowns, allowing time for the market to see its real value without the immediate danger of financial pressure.

Profitability and Growth: The Mechanism for Awareness

A value stock requires a way for the market to change its price. This often comes from continued profitability and future growth outlooks. WGO’s profitability score is a good 6, and its growth score is 4, with a clearly positive direction.

- Proven Profitability: The company has been regularly profitable with positive cash flow for more than five years. Its Return on Assets, Return on Equity, and Operating Margin all are in the top half of its industry, showing effective operations.

- An Important Growth Change: While recent years have seen pressure on earnings per share (EPS), the fundamental report points out a strong expected shift. Analysts estimate EPS to increase by over 43% on average in the next years, a "very strong growth" forecast. This speed-up from past patterns is a main factor that could lead to a new valuation.

- Dividend Backing: With a dividend yield of 3.04% that has increased steadily for ten years, WGO gives cash to shareholders. This yield offers a real return while investors wait for price increase, a trait often liked in value portfolios.

The mix of past profitability and a clear prediction for notable earnings speed-up meets a frequent value investing test: seeing when a time of little change might be finishing. The estimated growth gives a basic reason for the market to review the stock's price.

Conclusion and Next Steps

Winnebago Industries shows a picture that matches several value investing ideas: a valuation that seems careful compared to peers and future earnings, a very firm balance sheet that lowers risk of loss, and a clear factor in the shape of speeding estimated profit growth. While the company works in the changing recreational vehicle market, its financial strength places it to weather slowdowns, and its valuation seems to include much of the cyclical worry.

For investors wanting to study other companies that share this picture of acceptable valuation along with good basics, more study can be done. You can find more possible candidates by using the Decent Value Stocks screen on ChartMill.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investing includes risk, including the possible loss of principal. You should do your own study and talk with a qualified financial advisor before making any investment choices.