In the world of investing, the search for undervalued opportunities is a timeless pursuit. One systematic approach involves screening for companies that appear fundamentally cheap relative to their intrinsic worth, while still demonstrating solid underlying business health. This method focuses on stocks with strong valuation metrics, suggesting they may be priced below their true value, but also requires evidence of decent profitability, a firm financial position, and at least some growth trajectory. This combination aims to avoid the classic "value trap," where a low price is a symptom of permanent decline rather than a temporary market mispricing. Today, we examine Winnebago Industries (NYSE:WGO) through this lens to see if it presents such an opportunity.

A Closer Look at Valuation

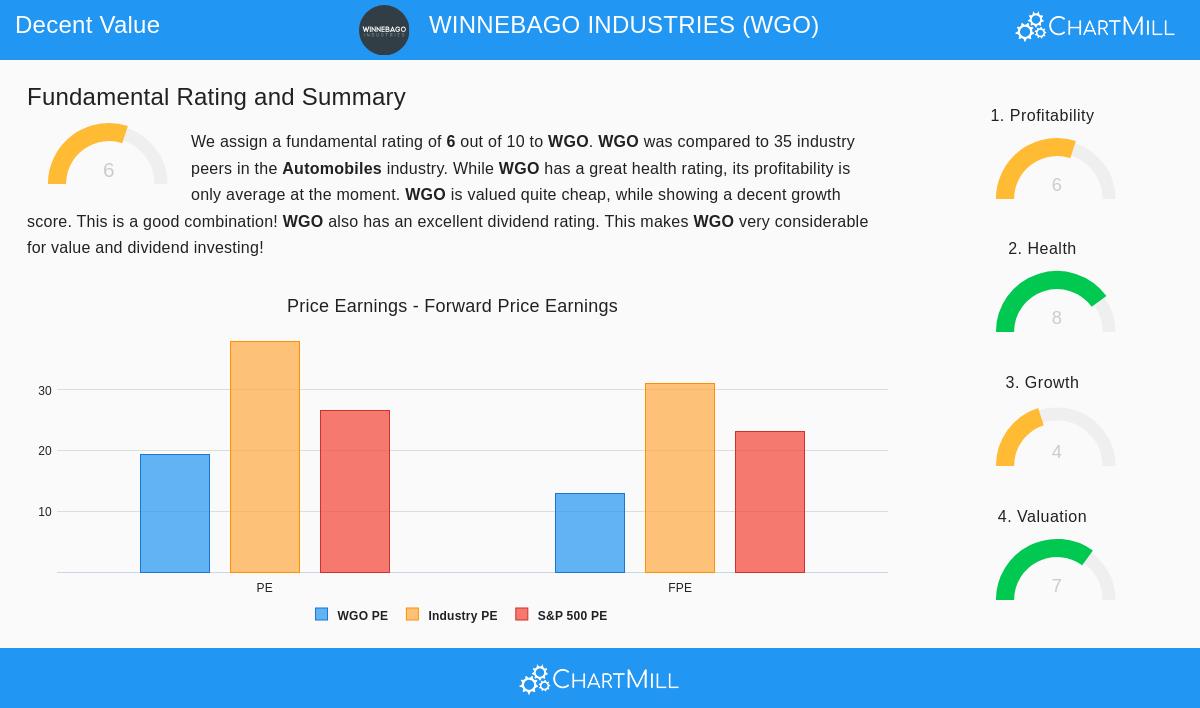

The core of any value investment thesis is valuation. For Winnebago Industries, the metrics suggest the market may be pricing the company at a discount, particularly within its own sector. According to ChartMill's fundamental analysis, WGO earns a Valuation Rating of 7 out of 10, indicating an attractive price relative to its financials.

- Industry Discount: While its standard Price-to-Earnings (P/E) ratio of 19.39 might seem elevated in a vacuum, it is significantly cheaper than 85.7% of its peers in the Automobiles industry, where the average P/E sits above 38.

- Forward-Looking Metrics: More telling is the Forward P/E ratio of 12.95, which is lower than 77% of industry competitors and well below the S&P 500 average of 23.13. This suggests analysts see earnings growth ahead that isn't fully reflected in the current share price.

- Cash Flow and Growth Adjustment: The stock also appears cheap based on its Price-to-Free Cash Flow ratio, outperforming 91.4% of the industry. Furthermore, a low PEG ratio, which factors in expected earnings growth, points to a valuation that may not be fully compensating for the company's future potential.

For a value investor, these figures are the starting point. A low valuation relative to both the market and industry peers creates the potential for price appreciation as the gap between market price and perceived intrinsic value closes.

Assessing Financial Health and Profitability

A cheap stock is only a good investment if the company is financially sound. This is where the "margin of safety" concept is critical. Winnebago's financial health provides a sturdy foundation, earning a high Health Rating of 8/10.

- Strong Balance Sheet: The company exhibits excellent liquidity, with a Current Ratio of 2.42 that outperforms 91% of the industry, indicating a strong ability to cover short-term obligations.

- Manageable Debt: With a Debt-to-Equity ratio of 0.44, Winnebago is less reliant on debt financing than many competitors, outperforming 65.7% of its industry peers. Its Altman-Z score of 3.49 also signals a low near-term risk of financial distress.

- Profitability Snapshot: The Profitability Rating is a neutral 6/10. Key return metrics like Return on Assets (1.19%) and Return on Invested Capital (1.87%) are decent and outperform over 74% of the industry. However, margins have faced pressure recently, with both Profit Margin (0.92%) and Operating Margin (2.04%) showing declines from previous years, a point for investors to monitor.

This financial health is vital for the value strategy. It suggests the company has the resilience to weather economic downturns and industry cycles, reducing the risk that its low valuation is a precursor to financial trouble.

Growth Prospects and Dividend Appeal

For a value stock to realize its potential, it needs a catalyst. Often, that is growth. Winnebago's Growth Rating is a modest 4/10, reflecting recent challenges but also pointing to a significant expected turnaround.

- Past Challenges: The company has faced headwinds, with EPS declining 9.5% over the past year and Revenue down 5.9%.

- Future Acceleration: The outlook, however, is markedly brighter. Analyst estimates project an average annual EPS growth of 43.5% and Revenue growth of 5.9% in the coming years. The report notes that both EPS and Revenue growth rates are accelerating, a positive inflection point.

- Income Component: Adding to its appeal for certain value investors, Winnebago carries a solid Dividend Rating of 7/10. It offers a yield of 3.29%, which is attractive compared to the industry average of 0.84% and the broader S&P 500. The company has a reliable 10-year track record of paying and growing its dividend, with an impressive annual growth rate of 25%.

This projected growth acceleration is the engine that could drive a re-rating of the stock. When combined with a low valuation, improving future earnings can be a strong driver of shareholder returns, supplemented by the income from its dividend.

Conclusion: A Candidate for the Value Watchlist

Winnebago Industries presents an interesting profile for investors screening for decent value. It trades at a discount to its industry based on several key valuation metrics, has a strong financial position that provides a margin of safety, and is projected to return to a meaningful growth path after a period of contraction. While its recent profitability margins warrant attention, the overall fundamental picture suggests the market may be undervaluing its future earnings potential and durable business model.

The combination of cheap valuation, financial health, and anticipated growth aligns with a disciplined value approach that seeks quality on sale. For investors interested in exploring similar opportunities, more potential candidates identified by this "Decent Value" screening methodology can be found here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any securities. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Past performance and forward-looking estimates are not guarantees of future results.