For investors looking to balance the search for growth with some caution, the Growth at a Reasonable Price (GARP) strategy offers a practical middle path. This method looks for companies that are increasing their earnings and revenue faster than average but are not priced too high. The aim is to sidestep the high risk of paying too much for uncertain growth while still gaining from active businesses. One way to find these opportunities is through a structured filter for "affordable growth," which selects stocks with good growth scores, firm basic profitability and financial strength, and a valuation that is not extreme. Vertiv Holdings Co-A (NYSE:VRT) appears as a stock that matches this description, justifying more attention from investors using this method.

A Close Look at Growth Measures

The central part of any GARP investment is, expectedly, growth. Vertiv’s results here are strong, receiving a high Growth score of 8 out of 10 in its fundamental analysis report. The company is showing significant momentum in its recent performance and its future path.

- Past Results: Over the previous year, Vertiv recorded a notable 57.85% increase in Earnings Per Share (EPS), with a high five-year annualized EPS growth rate of 55.36%. Revenue increase has been similarly notable, rising 28.76% in the last year.

- Future Projections: Analysts forecast this solid performance to persist, with estimated annual EPS growth of 26.14% and revenue growth of 18.03% in the next few years. Importantly, the expected revenue growth rate is speeding up relative to its past rate.

This mix of excellent historical delivery and a positive forward view supplies the necessary "growth" part for the affordable growth filter. A company must first prove it is a genuine growth story before its price is even examined.

Evaluating Price Relative to Value

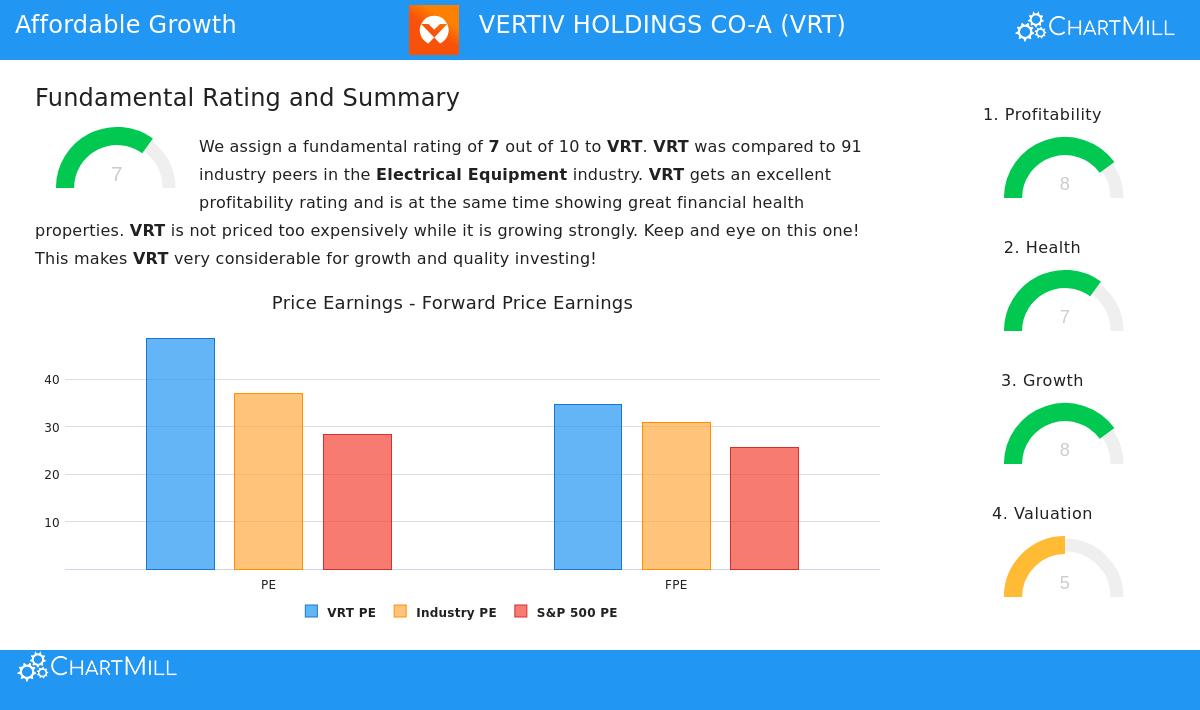

A high-growth profile frequently carries a high price, which is where the "reasonable price" part of GARP turns important. Vertiv’s Valuation score of 5 shows a varied situation that needs perspective. On the surface, standard measures seem high.

- The stock has a Price-to-Earnings (P/E) ratio of 48.74, which is costly compared to the wider S&P 500 average.

- Its Forward P/E ratio of 34.64 is also above the market average.

Yet, price assessment is seldom simple. When compared to its counterparts in the Electrical Equipment industry, Vertiv’s situation shifts. Its P/E and Forward P/E ratios are lower than about 67% to 69% of its industry peers. This comparative value is a main reason it clears the filter’s price check. Also, the market seems to be accounting for the company’s unusual growth and quality, as shown by a neutral PEG ratio—which modifies the P/E for growth—and notes in the report that the higher price may be acceptable given its excellent profitability and projected earnings growth.

The Base: Profitability and Financial Strength

Lasting growth cannot be sustained without a sound operational and financial base. This is why an affordable growth filter includes checks for profitability and financial strength, and Vertiv does well in both areas, each scoring an 8 and 7, respectively.

Profitability advantages include:

- Unusually high returns on equity (29.48%) and invested capital (18.23%), putting it in the best group of its industry.

- Solid and growing margins, with an operating margin of 18.03% that beats over 92% of industry counterparts.

Financial Strength points are:

- A very good Altman-Z score of 7.68, showing very low bankruptcy risk.

- A sound debt situation, with a low debt-to-free-cash-flow ratio of 2.14, indicating the company can repay its debts quickly from its cash flow.

These elements are not minor; they are essential to the GARP argument. High profitability confirms the business model and supports future growth from within, while a strong balance sheet offers stability during economic slowdowns and the ability to take on chances. A company with poor strength or profitability is a uncertain growth choice, no matter its price.

Final Thoughts and Next Steps

Vertiv Holdings Co-A presents a strong example for the affordable growth or GARP approach. It pairs very high historical and forecasted growth with a price that, while not low in absolute terms, is acceptable compared to its strong sector. Importantly, this growth is supported by a base of first-class profitability and sound financial strength, lowering the danger usually linked with high-growth stocks.

For investors wanting to examine other companies that meet similar standards of good growth, acceptable price, and firm basics, more investigation can be done using the set Affordable Growth stock filter.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions.