For investors looking to balance the search for growth with some caution, the "Growth at a Reasonable Price" (GARP) method presents a solid middle path. This tactic tries to find companies increasing their earnings and sales faster than normal, but whose stock prices are not excessively high. It is a way to steer clear of paying too much for uncertain high-growth while still participating in positive business trends. One instrument for using this tactic is an "Affordable Growth" stock filter, which selects for companies with good growth basics, firm profit and financial condition, and a stock price that is not excessive. A present example from this filter is Vertiv Holdings Co-A (NYSE:VRT).

Vertiv, a worldwide supplier of important digital infrastructure technology for data centers and communication networks, is positioned within several major long-term trends, like the growth of cloud computing and artificial intelligence. The company's recent fundamental analysis report, available here, shows a picture that matches the affordable growth idea closely.

Strong Growth Path

The central idea of any growth tactic is, expectedly, growth. Vertiv does very well here, receiving a high ChartMill Growth Rating of 8 out of 10. The company is not only suggesting future growth, it is producing notable results now and in the recent period.

- High Earnings Growth: Over the last year, Vertiv's Earnings Per Share (EPS) increased by 57.85%. The average yearly EPS growth over recent years is a notable 55.36%.

- Firm Revenue Growth: Revenue rose by 28.76% in the last year, with a firm multi-year average growth rate of 12.57%.

- Positive Future View: Analysts project this trend to persist, with predicted average yearly EPS growth of 26.08% and revenue growth of almost 18% in the next few years.

This mix of firm past performance and a positive future view gives a solid base for the growth part of the investment case. For a GARP tactic, such shown and expected growth is necessary to support the current stock price.

A Valuation Perspective

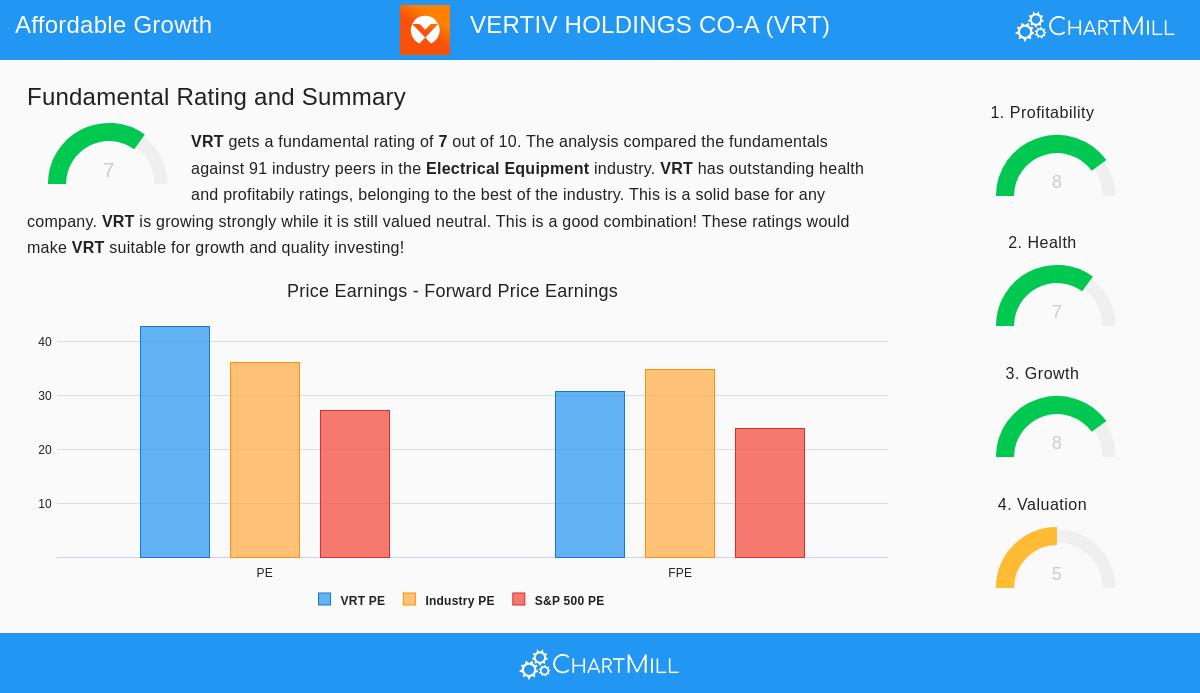

A stock with excellent growth can still be a bad investment if the cost is too steep. This is where the "reasonable price" part is important. Vertiv's ChartMill Valuation Rating is a neutral 5, which, considering its high growth and sector, points to a balanced view instead of clear overpricing.

The report shows a varied set of standard valuation measures:

- Its Price-to-Earnings (P/E) ratio of 42.82 seems high both on its own and next to the wider S&P 500.

- However, almost 70% of similar companies in the Electrical Equipment industry have higher P/E multiples, meaning Vertiv is less costly within its high-growth field.

- More significantly, its Price-to-Earnings Growth (PEG) ratio, which includes earnings growth projections, is noted as low, meaning the valuation could be fair when growth is considered.

- Other measures like Enterprise Value to EBITDA and Price to Free Cash Flow also position Vertiv as less expensive than most of its industry rivals.

For an affordable growth filter, a valuation score above 5 is used to remove the most extremely overpriced options. Vertiv’s rating shows a market that is including its growth in the price, but not to a severe extent when seen with industry-specific and growth-adjusted views.

Supporting Basics: Profit and Condition

A growth case is much more durable when supported by a profitable business operation and a firm financial position. Vertiv also scores well here, with ChartMill Profit and Condition Ratings of 8 and 7, in order. These scores are important for the GARP tactic, as they help lower the risk commonly linked with high-growth companies.

- High Profit: The company has very good margins and returns on capital. Its Operating Margin of 18.03% and Return on Invested Capital (ROIC) of 18.23% put it among the best in its industry. Firm and getting better profit points to efficient operations and pricing ability.

- Firm Financial Condition: Vertiv displays a strong Altman-Z score, indicating low short-term bankruptcy risk. While it has a moderate amount of debt, its firm free cash flow production means it could pay off all its debt in slightly more than two years, a sign of high solvency.

These elements are not minor details. In an affordable growth tactic, adequate profit and condition make sure the company has the financial strength to manage economic changes and keep funding its growth plans from within.

Final Points and More Study

Vertiv Holdings Co offers a solid example for the Growth at a Reasonable Price method. It shows the strong, proven growth that pushes stock price gains, paired with a valuation that, while not low-cost, is supported relative to its industry and growth picture. This pairing is strengthened by top-level profit and a financially sound balance sheet, decreasing the speculative risk often connected to pure growth investing.

The company’s place in the needed infrastructure for data and AI supplies a long-term support for its growth story. For investors filtering for similar chances that balance trend with price carefulness, Vertiv deserves more detailed study.

Interested in finding other stocks that match the Affordable Growth description? You can use the same filter applied to find Vertiv and look at more possible choices here.

Disclaimer: This article is for information only and is not financial advice, a suggestion to buy or sell any security, or a support of any investment plan. The information given is based on data thought to be reliable but not certain. Investors should do their own complete study and think about their personal money situation and risk comfort before making any investment choices.