For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) method provides a solid middle path. This method tries to find companies showing solid and lasting growth, but whose shares are not valued at the extreme levels seen with highly speculative stocks. It looks for businesses with good basic financials, healthy balance sheets and strong profitability, to confirm the growth is supported by a stable base. One stock that recently appeared from this type of screening process is Vertiv Holdings Co-A (NYSE:VRT).

The company, an important provider in designing and servicing digital infrastructure for data centers and communication networks, seems to match the main ideas of affordable growth investing. An examination of its fundamental analysis report shows a profile noted for outstanding growth measures and good operational health, even while its valuation shows a more detailed situation.

Outstanding Growth Path

The most notable part of Vertiv's current profile is its strong growth momentum, which is a main filter in any GARP method. The company is not simply growing; it is speeding up at a notable rate.

- Strong Recent Performance: Over the last year, Vertiv's Earnings Per Share (EPS) increased by 57.85%, while Revenue grew by 28.76%. This shows the growth is meaningfully reaching the bottom line.

- Good Historical Pattern: This is not a single event. The company's average yearly EPS growth over recent years is a notable 55.36%, with Revenue growing at a good 12.57% rate.

- Positive Future View: Analysts believe this momentum will persist, with predictions for average yearly EPS growth of 26.08% and Revenue growth of 17.99% in the next few years. Importantly, the expected revenue growth rate is faster than its historical pattern.

This mix of excellent past results and a solid future view is exactly what growth-focused investors look for, offering a persuasive story for future share price gains.

A Detailed Valuation Situation

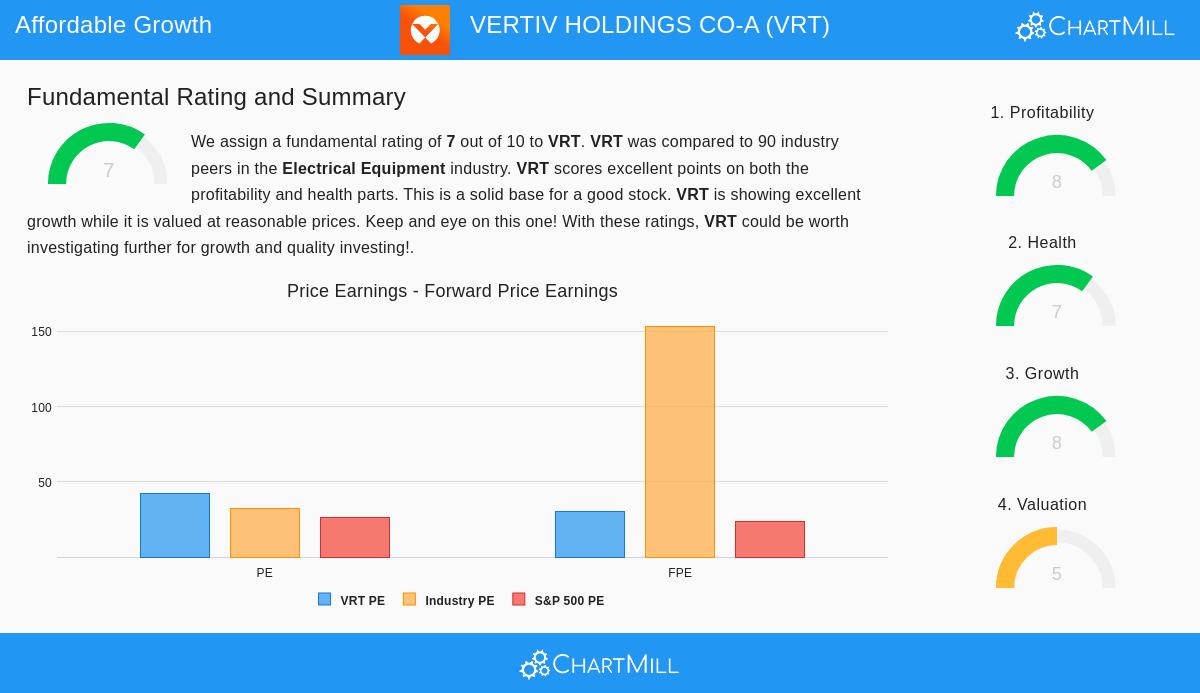

Valuation is the "reasonable price" part of the GARP formula, and here Vertiv shows a varied but finally positive case when seen through the right view. On its own, some standard measures seem high.

- The stock's Price/Earnings (P/E) ratio of 42.34 is above the current S&P 500 average, indicating a premium.

- In the same way, its Forward P/E ratio of 30.59 is also higher than the wider market average.

However, valuation is relative and must be put in context, especially for a fast-growth company. Two important factors soften these seemingly high multiples:

- Industry Comparison: Compared to similar companies in the Electrical Equipment industry, Vertiv's valuation seems much more appealing. Its P/E and Forward P/E ratios are lower than about 70% of the industry, which includes many slower-growing companies.

- Growth Adjustment: The central measure for GARP investors is often the PEG ratio, which modifies the P/E ratio for expected earnings growth. Vertiv's low PEG ratio shows the market may not be completely valuing its outstanding growth path, suggesting a possibly reasonable, or even low, valuation when growth is considered.

This context is important. The screening process deliberately searches for stocks that are "not overvalued," a judgment that thinks about relative value and growth adjustment, not only absolute P/E figures. Vertiv's valuation score mirrors this balanced view.

Supported by Health and Earnings

Lasting growth cannot happen without financial strength and earnings, which serve as risk reducers in the method. Vertiv does very well in these areas, giving assurance that its growth is high-quality.

- High Earnings: The company receives an excellent earnings rating, supported by superior margins and returns. Its Operating Margin of 18.03% and Return on Equity of 29.48% place in the top group of its industry, showing efficient and profitable operations.

- Good Financial Health: Vertiv keeps a solid balance sheet. Its Altman-Z score shows no bankruptcy risk, and an important solvency measure, the ratio of Debt to Free Cash Flow, is a good 2.14, meaning it could in theory pay off all debt in just over two years from its cash flow. This financial stability is key for supporting continued growth and handling economic changes.

Summary and Additional Study

Vertiv Holdings Co offers a persuasive example for the affordable growth investment style. It displays the model this method looks for: a company with strong, proven growth in both sales and earnings, a valuation that is sensible when compared to its industry and future possibility, and the basic strength of high earnings and a solid balance sheet. The company's place in the necessary digital infrastructure system gives a long-term boost to its growth story.

For investors wanting to examine other companies that match this profile of solid growth, sensible valuation, and sound basics, more results can be found by checking the Affordable Growth stock screen.

A detailed look at the individual measures behind this study is available in the full Fundamental Analysis Report for VRT.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion, or an offer to buy or sell any securities. Investors should do their own study and think about their personal financial situation before making any investment choices.