Investors looking for expansion possibilities at fair prices frequently consider the "Affordable Growth" investment method. This plan focuses on firms showing solid development possibility while keeping good financial condition and earnings, all without requiring high price multiples. By concentrating on equities with strong growth paths that sell at reasonable multiples, investors try to capture upward possibility while reducing the dangers connected to expensive growth narratives. The process methodically assesses firms through several basic aspects to find those providing the best mix between expansion outlook and price restraint.

Vertiv Holdings Co-A (NYSE:VRT) appears as an interesting option inside this investment structure. The firm, which plans and makes important digital infrastructure technology for data centers and communication systems, shows the basic qualities that affordable growth investors usually look for. Its detailed basic examination shows a firm working from a state of advantage across several financial areas while keeping acceptable price points compared to its expansion outlook.

Growth Path

Vertiv's growth story is especially notable, with the firm showing solid past results and keeping good future movement. The growth measures show a firm in a development phase:

- Earnings Per Share rose 57.85% over the last year with a five-year average yearly growth pace of 55.36%

- Sales grew 28.76% in the latest year with a steady 12.57% yearly growth pace over several years

- Future estimates point to continued growth with EPS predicted to grow 26.08% each year and sales expected to rise 17.99% per year

This mix of solid past performance and good future expectations places Vertiv as a firm able to provide ongoing development. The quickening sales growth pace implies the firm is getting market hold and successfully using industry support in digital infrastructure.

Price Evaluation

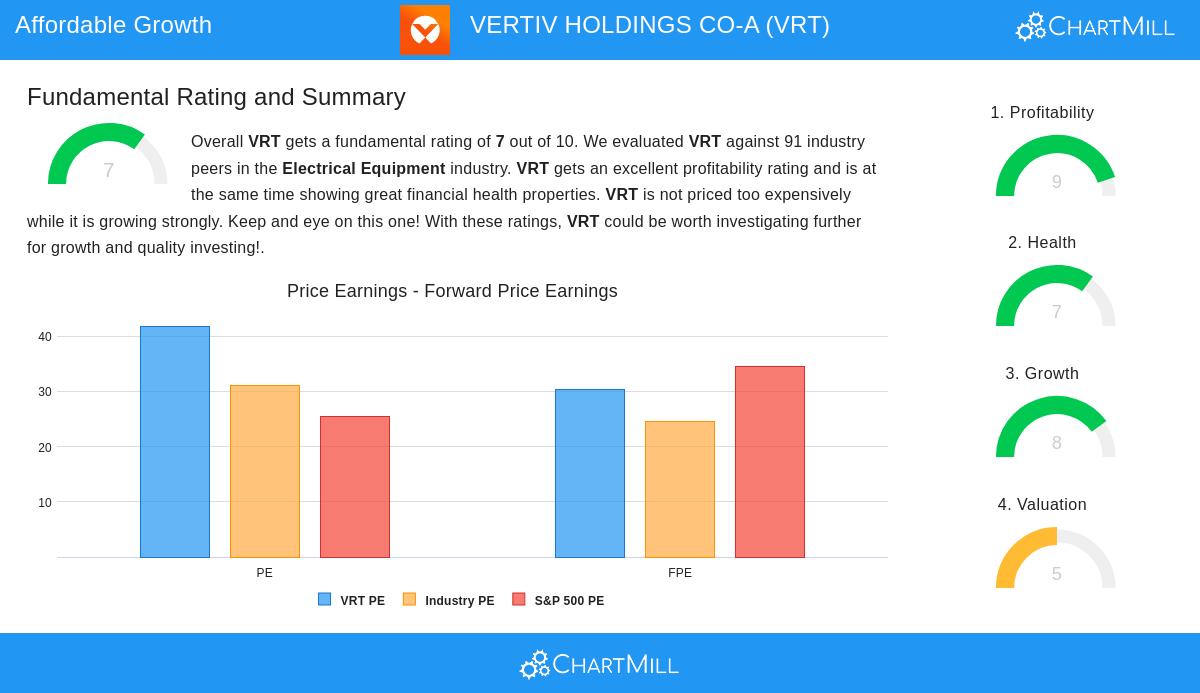

While Vertiv sells at high multiples on some measures, the price becomes more acceptable when viewed next to its growth picture and industry place. The price view shows a detailed story:

- Current P/E ratio of 41.84 looks high compared to the S&P 500 average of 25.45

- Forward P/E of 30.36 matches more nearly with market averages and stacks up well to industry similar firms

- Enterprise Value to EBITDA and Price/Free Cash Flow ratios rank lower than about 70% of industry rivals

- The small PEG ratio, which changes the P/E for growth forecasts, shows the price may be acceptable given the firm's development path

The price evaluation highlights why affordable growth plans look at several measures instead of using only standard P/E ratios. When growth paces and earnings are included in the study, Vertiv's price seems more warranted.

Earnings Ability

Vertiv's earnings picture shows excellent operational effectiveness and competitive benefits within its industry. The firm's capacity to turn sales into profits is notable across several areas:

- Return on Equity of 29.48% puts Vertiv in the top group of its industry, doing better than 96.70% of similar firms

- Return on Invested Capital of 18.23% greatly passes the firm's capital cost, showing value generation

- Operating Margin of 18.03% rates with the industry's top, exceeding 92.31% of rivals

- All main margin groups—gross, operating, and profit margins—have shown gain in recent years

This earnings ability gives important support for the affordable growth idea, as firms with good margins and returns on capital usually show lasting competitive benefits and price influence.

Financial Condition

Vertiv keeps a firm financial base that supports its expansion goals while handling risk suitably. The firm's balance sheet and cash position give steadiness:

- Altman-Z score of 6.84 shows very low failure danger and does better than 90.11% of industry similar firms

- Debt to Free Cash Flow ratio of 2.14 shows good debt handling ability

- Current and Quick ratios of 1.83 and 1.43 respectively show enough short-term cash

- Gaining debt to assets ratio shows active balance sheet care

The financial condition measures show a firm that can pay for growth projects while keeping operational steadiness, a key factor for growth investors worried about longevity.

Vertiv's mix of solid growth, excellent earnings, firm financial condition, and acceptable price relative to expansion outlook makes it worth looking at for investors using affordable growth plans. The firm works in the growing digital infrastructure market, placing it to gain from continuing technological change patterns.

Look for more affordable growth equity chances through our preset filtering process.

This article gives basic study for educational reasons only and does not form investment guidance, suggestion, or support of any security. Investors should do their own study and talk with money consultants before making investment choices. Past results do not ensure future outcomes, and all investments hold risk including possible loss of original money.