For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) or "affordable growth" method presents a considered option. This method tries to find companies with good and lasting growth paths, but whose stock prices are not at extreme levels that allow for no mistake. It avoids the sharp swings of highly speculative growth stocks while also steering clear of value traps, companies that seem inexpensive but have no mechanism for future growth. By using a systematic filter for stocks with good growth marks, firm financial condition, acceptable profitability, and a sensible price, investors can create a list of possibilities that might present an attractive balance of risk and potential return. One company that appears from this kind of review is VERACYTE INC (NASDAQ:VCYT).

A Focus on Growth

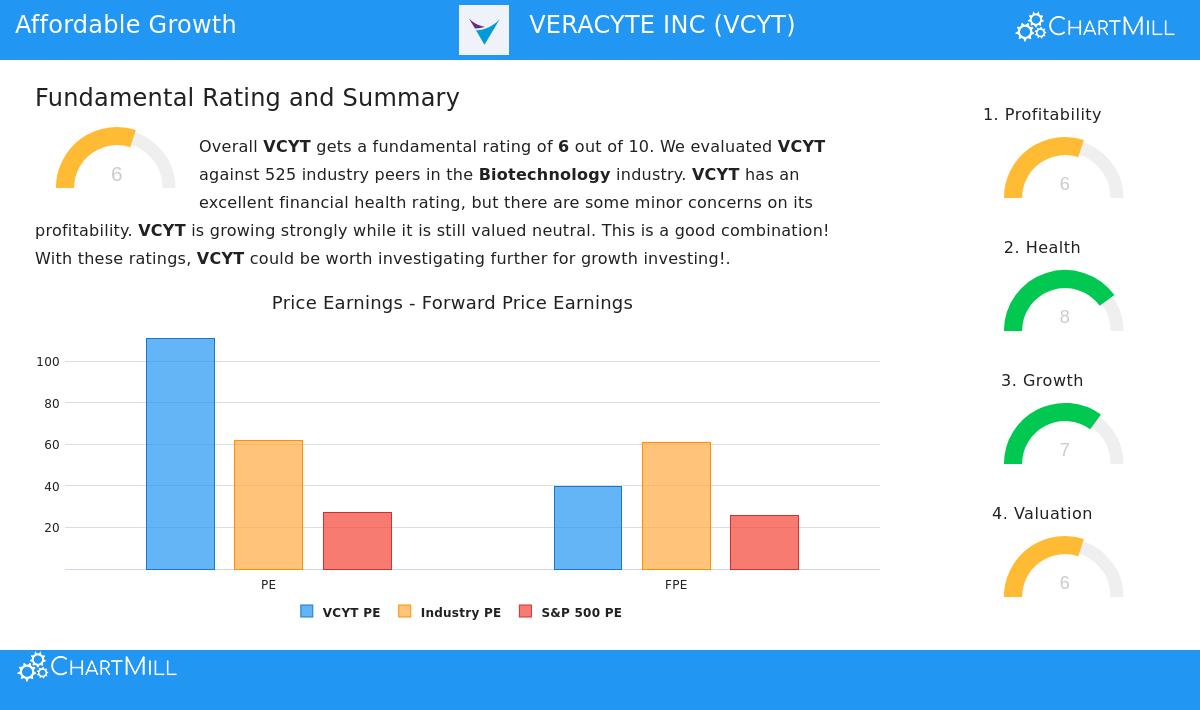

The central idea of any affordable growth method is, expectedly, growth. A company needs to show a clear capacity to increase its business, as this is the main source of future returns for shareholders. Veracyte’s basic profile indicates notable force in this part, receiving a Growth Rating of 7 out of 10 from ChartMill.

- Notable Historical Growth: The company's sales have increased at an average yearly rate of almost 30% over the last few years, a speed that is much faster than many similar companies. More lately, sales rose by 16.41% over the previous year.

- Earnings Speed-Up: Maybe more importantly, Veracyte has turned sales growth into profit results. Earnings Per Share (EPS) rose by a remarkable 353.33% in the past year, showing better operational efficiency and size.

- Good Future Projection: Analyst forecasts back the ongoing growth story. Predictions indicate average yearly EPS growth above 51% and sales growth of about 11.5% in the next years. This future direction is important, as the affordable growth method depends on what may come, not only what has happened.

Valuation in Context

A sensible price is the balancing element that describes this method. A stock with excellent growth but a very high cost holds more risk if growth slows. Veracyte shows a detailed price picture, getting a neutral Valuation Rating of 6. On initial view, standard measures like a Price-to-Earnings (P/E) ratio of 111 seem very high, particularly next to the wider S&P 500 average. Still, price must be evaluated next to a company's field and growth outlook.

- Industry-Relative Price: When measured against its Biotechnology field equals, Veracyte’s price seems much more sensible. Its P/E ratio is lower than almost 90% of the field, and its Price-to-Forward Earnings ratio is lower than over 91% of rivals. This field comparison is key for growth-phase biotech and diagnostic firms.

- Growth Adjustment: The Price/Earnings-to-Growth (PEG) ratio, which changes the P/E ratio for predicted earnings growth, points to a more even price for VCYT. The market cost seems to be considering the company's high estimated growth rate.

- Cash Flow and EBITDA Measures: Adding more support for the case of sensible price, measures like Enterprise Value to EBITDA and Price to Free Cash Flow show Veracyte is priced lower compared to a large majority of its field equals. This implies investors are not paying too much for the company's basic cash creation.

Supporting Basics: Condition and Earnings

For growth to be lasting and the price to be fair, a company must rest on a steady base. This is where financial condition and earnings become important, making sure the company can pay for its growth from within and manage economic changes.

- Outstanding Financial Condition (Rating: 8): Veracyte’s balance sheet is a strong point. The company has no debt, giving great operational freedom and protecting it from increasing interest costs. Its cash position is also firm, with a Current Ratio of 6.23 and a Quick Ratio of 5.94, showing more than enough means to meet near-term needs. A very high Altman-Z score verifies the company is not near any financial trouble.

- Acceptable and Getting Better Earnings (Rating: 6): While the company has had a varied record of yearly profits, recent patterns are good. More significantly, its profit margins are firm. Veracyte’s Gross Margin of 68.5%, Operating Margin of 9.7%, and Profit Margin of 6.1% all place in the top group of its field. This shows the company's ability to change sales into profits effectively, a main part for long-term value building.

Conclusion

Veracyte Inc. shows the kind of company an affordable growth filter aims to find. It combines clear and predicted firm growth, especially in profits, with a price that, while not low in simple terms, is sensible inside its high-growth field setting. This pairing meets the main aim of the method: looking for gain possibility without paying a speculative cost. The investment argument is made stronger by a very firm, debt-free balance sheet and field-leading profit margins, which supply the financial steadiness and operational effectiveness needed to carry out its growth plans.

For investors curious about examining other companies that fit similar standards of good growth, sensible price, and sound basics, you can see the complete Affordable Growth stock filter results. A more detailed look at Veracyte’s separate basic measures is in its full basic analysis report.

Disclaimer: This article is for information only and is not financial guidance, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own study and think about their personal financial situation and risk comfort before making any investment choices.