In the search for investment opportunities, a disciplined method often produces the most encouraging candidates. One such approach is the "Decent Value" screen, which methodically finds stocks that seem priced low by the market while keeping good basic business qualities. This plan depends on the central idea of value investing: looking for companies trading below their real worth. The screen filters for stocks with a good valuation rating, meaning they are inexpensive compared to their financial numbers, while also needing acceptable scores in profitability, financial condition, and expansion. This layered review helps sidestep the typical "value trap"—a stock that is low-priced for a cause—by confirming the company is basically healthy and able to build value for shareholders. A recent screen using this process has pointed to TAYLOR MORRISON HOME CORP (NYSE:TMHC) as a possible candidate deserving more review.

A Closer Look at Valuation

The most persuasive starting point for Taylor Morrison is its valuation numbers, which appear as very reasonable, particularly within the present market setting. The company's stock trades at a notable markdown based on standard measures, a main sign for value-focused investors looking for a margin of safety.

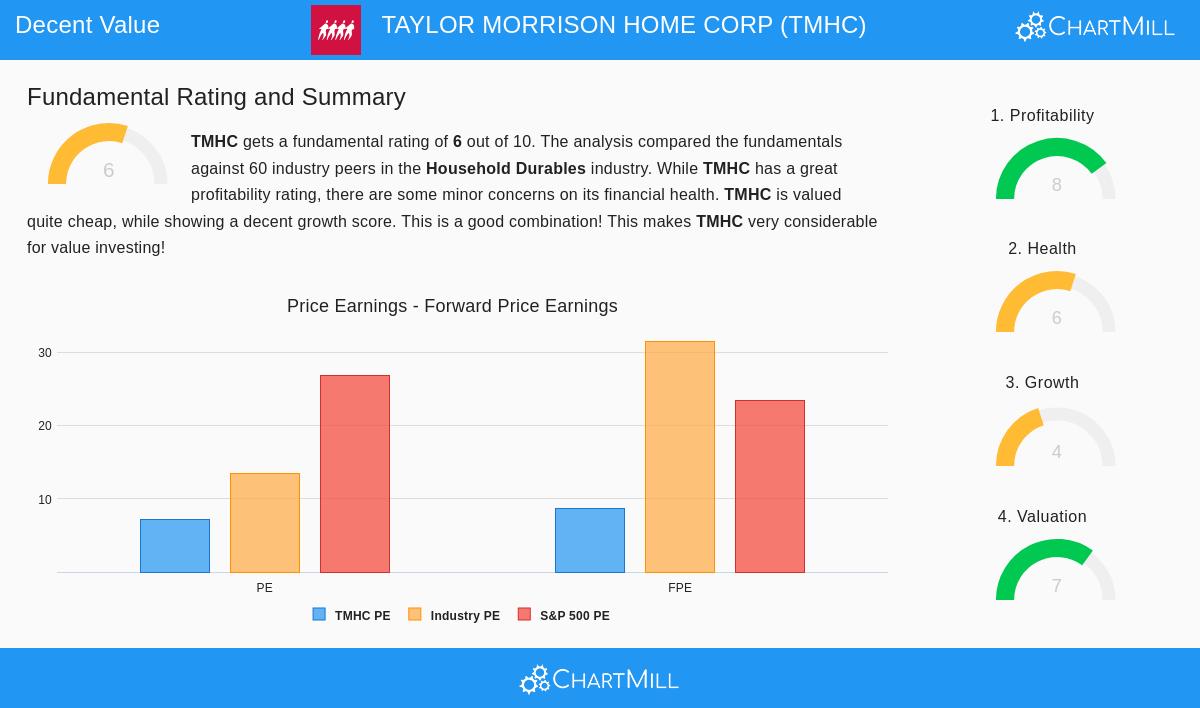

- Price-to-Earnings (P/E) Ratio: At 7.13, TMHC's P/E ratio is labeled "very cheap." This is not only much lower than the S&P 500 average of about 26.8, but it also puts the company in a good spot within its own industry. The review shows that almost 87% of its peers in the Household Durables sector are more costly on this basis.

- Forward P/E and Enterprise Value: The forward P/E ratio of 8.60 is also considered reasonable and less expensive than 90% of industry rivals. Also, numbers like the Enterprise Value to EBITDA and Price/Free Cash Flow ratios indicate the stock is valued at a lower price than most of its industry peers.

For a value investor, these numbers are the first attraction. A low valuation compared to earnings and cash flow gives that important buffer, the margin of safety, that Benjamin Graham stressed. It implies the market may be setting too low a price on the company's present earnings ability, offering a potential chance if that view shifts.

Reviewing Financial Condition and Profitability

An inexpensive stock is only a good investment if the company is financially steady and profitable. This is where the "Decent Value" screen's extra requirements become important, and Taylor Morrison's profile remains good.

Financial Health gets a moderate score of 6 out of 10. The company shows several positive indicators:

- A solid Altman-Z score of 3.76 shows little near-term danger of financial trouble.

- A workable Debt-to-Equity ratio of 0.35 indicates the company is not too dependent on debt financing.

- The company has been steadily lowering both its debt-to-assets ratio and its number of shares outstanding over recent years, which can add to shareholder value.

However, analysts see a small issue about liquidity, specifically a low Quick Ratio, which hints at a possible weakness in meeting very short-term duties without selling inventory. This is a point for investors to watch but is offset by the otherwise firm solvency metrics.

Profitability is where Taylor Morrison does very well, getting a high rating of 8 out of 10. The company has a steady history of producing profits and cash flow.

- Strong Margins: An Operating Margin of 14.53% and a Profit Margin of 10.16% are some of the best in its industry, doing better than over 83% of peers. These margins have also shown gain in recent years.

- Efficient Capital Use: Returns on Assets (8.84%), Equity (13.76%), and Invested Capital (10.86%) are all higher than the industry median, showing management is using capital well to produce profits.

This strong profitability is important for the value argument. A company that is both low-priced and highly profitable is often hard to find. The good returns suggest the business has a lasting competitive edge and efficient operations, supporting the case that the present low valuation may not be warranted by its earnings capacity.

Growth Path and Future Prospects

Growth is the final part, supplying the driver that could help narrow the difference between market price and real value. Taylor Morrison's growth profile is varied, getting a rating of 4, which shows a change period.

The past growth has been good. Over the last several years, the company has provided a notable average yearly Earnings Per Share (EPS) growth of 23.4% and Revenue growth of 11.4%. This past performance shows the company's ability to enlarge successfully.

The difficulty, and the reason for the lower growth rating, exists in the future view. Analysts forecast a major slowdown, with EPS expected to grow only about 1.5% yearly and Revenue possibly shrinking slightly in the coming years. This expected reduction is likely a main element adding to the stock's low valuation, as the market sets a price for a more difficult environment for homebuilders.

For a value investor, this situation is important. The plan often involves investing in sound companies during cyclical or passing downturns. The question is whether the present low price properly accounts for the forecasted growth slowdown and whether the company's strong profitability gives a base to manage the cycle.

Conclusion: A Candidate for the Value-Focused Investor

Taylor Morrison Home Corp shows a standard case for value investment review. It is a profitable company with a good balance sheet trading at a valuation that suggests notable negativity about its future. The "Decent Value" screen found it exactly because it meets the level of being basically healthy, profitable and financially sound, while being priced down by the market.

The investment idea depends on whether an investor thinks the company's high profitability and past performance can manage a weaker market, and if the present valuation, with a P/E near 7, offers an enough margin of safety against those risks. It is not a speculative growth tale, but a potential chance to buy a quality business at a reduced price.

Interested in finding other stocks that match this disciplined value method? You can run the same "Decent Value" screen yourself to look at more candidates here.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The analysis is based on data provided and fundamental ratings, which can change. Investors should conduct their own thorough research and consider their individual financial circumstances before making any investment decisions.