The search for undervalued companies with good basic business foundations is a key part of value investing. This method involves finding stocks that trade for less than their true worth, often shown by low valuation numbers, while confirming the company is financially stable and earns a profit. A "Decent Value" screen uses this idea by selecting for stocks with good valuation ratings that also show acceptable levels of earnings power, financial stability, and expansion, trying to find possible chances before the wider market sees their value.

Valuation Metrics

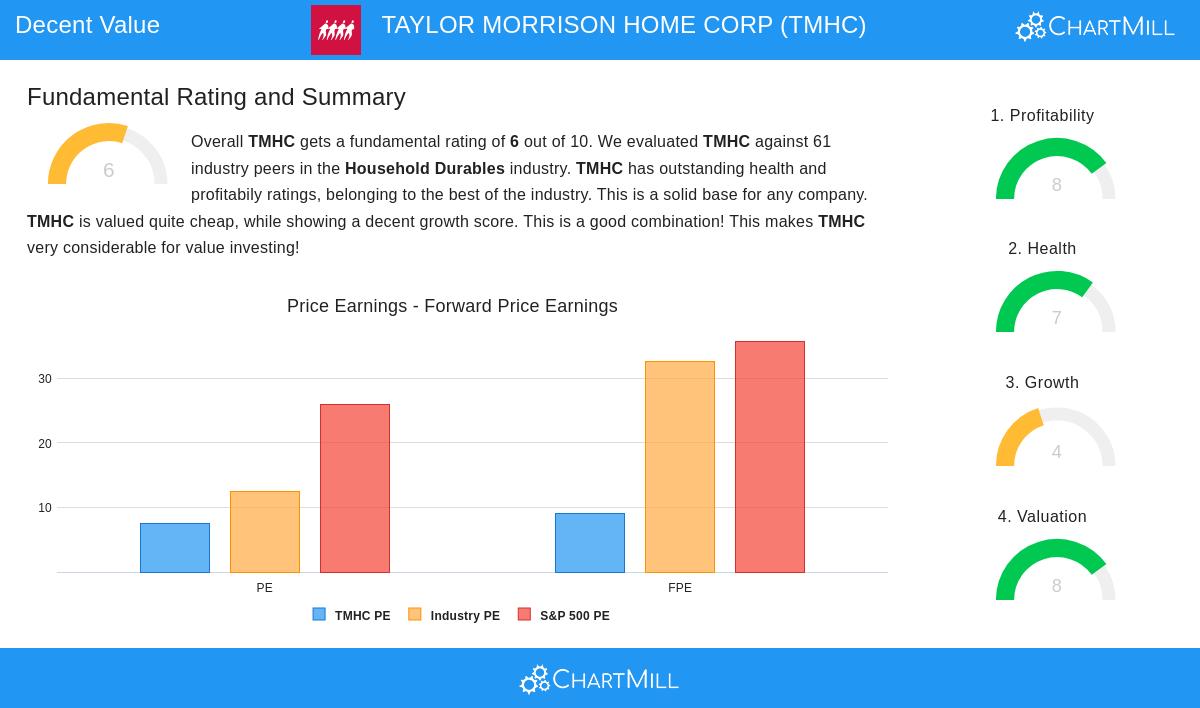

A main reason TAYLOR MORRISON HOME CORP (NYSE:TMHC) seems undervalued is its notable valuation numbers. The stock's present price-to-earnings (P/E) number is 7.50, which is much lower than the industry average and the wider S&P 500. This implies investors pay less for each dollar of profit compared to similar companies and the general market. Other important valuation measures support this view of a possibly inexpensive stock.

- The Price/Forward Earnings ratio is 9.02, showing a fair valuation and is less expensive than over 83% of its industry rivals.

- The Enterprise Value to EBITDA ratio also indicates a somewhat inexpensive valuation, doing better than 75% of the industry.

- Judging by the Price/Free Cash Flow ratio, TMHC is valued more affordably than 82% of the companies in its field.

For a value investor, these low numbers are the first sign. They suggest the market might be setting a low price on the company's profit and cash flow creation, forming a possible safety margin, a key idea of value investing that offers protection against mistakes in analysis or market declines.

Financial Health

An inexpensive valuation is not meaningful if the company carries too much debt or has payment problems. In this case, Taylor Morrison's financial condition is sound, scoring a 7 out of 10. The company keeps a good balance sheet, which is important for surviving economic changes and paying for future activities without too much danger.

- The company has an Altman-Z score of 3.82, showing financial stability and a low short-term chance of failure.

- Its Debt to Equity ratio of 0.35 displays a good mix between debt and equity funding.

- A Debt to FCF ratio of 3.84 is an indicator of high ability to pay debts, meaning it would take the company under four years of its free cash flow to repay all its obligations.

- The company has been steadily lowering its number of shares outstanding, which can be an action that benefits shareholders and raises the worth of each share that remains.

This good financial base lessens the danger for investors, making sure the company is not a "value trap", a case where a stock is inexpensive for a basic reason connected to its weak financial state.

Profitability

Besides being inexpensive and financially stable, a value pick must also be a profitable business. Taylor Morrison does well here, getting a high profitability score of 8 out of 10. The company not only makes profits but does so with notable effectiveness compared to other companies in the household durables industry.

- The company has a very good Profit Margin of 10.16% and an Operating Margin of 14.53%, doing better than 84% and 89% of its industry, in that order.

- Important effectiveness measures like Return on Assets (8.84%), Return on Equity (13.76%), and Return on Invested Capital (10.86%) all put the company in the top part of its industry.

- Importantly, these margins have been getting better over the last few years, showing positive operational movement.

For a value investor, continued and improving earnings power confirms that the business is of good quality. It gives assurance that the company's true value is backed by its capacity to create profit, strengthening the argument for undervaluation.

Growth Outlook

While the past and present are good, future possibilities are also taken into account. Taylor Morrison's expansion profile is not uniform, with a rating of 4 out of 10. The company has a very good record of expansion, but analyst forecasts for the future are more reserved.

- Past Performance: The Earnings Per Share has increased by an average of 23.42% over recent years, and Revenue has increased by 11.39% on average.

- Future Expectations: However, EPS expansion is anticipated to fall to 1.45%, and Revenue is expected to see a small drop.

This difference is significant for value investors. The excellent historical expansion helps support the company's quality, while the limited future forecasts may be a main reason the stock is now priced at such a low level. The investment idea would depend on whether the market is being too negative about the company's capacity to handle a possible housing decline.

A detailed look at all these basic factors is ready in the full fundamental analysis report for TMHC.

Conclusion

TAYLOR MORRISON HOME CORP presents a notable case for investors using a value method. The stock trades at a large discount to the market and its industry based on important valuation numbers, suggesting a possible safety margin. This inexpensive valuation is supported by good financial health, lowering failure risk, and very good profitability that highlights the quality of the basic business. While future expansion forecasts are moderate, the company's established history and financial strength make it a stock deserving of more study for those searching for undervalued chances.

For investors curious about finding other companies that match a similar outline of fair valuation together with acceptable basics, you can review more outcomes using the Decent Value Stocks screen.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The opinions expressed are based on current data and may change. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.