TAYLOR MORRISON HOME CORP (NYSE:TMHC) stands out as a potential candidate for investors seeking growth at a reasonable price (GARP). The homebuilder meets key criteria from Peter Lynch’s investment strategy, balancing solid growth, profitability, and an attractive valuation. Below, we examine why TMHC fits this approach.

Key Strengths of TMHC

- Strong Earnings Growth: Over the past five years, TMHC has delivered an impressive average annual EPS growth of 23.4%, well within Lynch’s preferred range of 15-30%. This indicates sustainable expansion without excessive risk.

- Attractive Valuation: With a PEG ratio (5Y) of 0.29, the stock appears undervalued relative to its growth. A PEG below 1 suggests the market may not fully price in TMHC’s earnings potential.

- Healthy Financials: The company maintains a debt-to-equity ratio of 0.35, aligning with Lynch’s preference for conservative leverage. Its current ratio of 5.98 reflects ample liquidity to cover short-term obligations.

- Profitability: TMHC’s return on equity (ROE) of 15.2% exceeds Lynch’s 15% threshold, demonstrating efficient use of shareholder capital.

Fundamental Snapshot

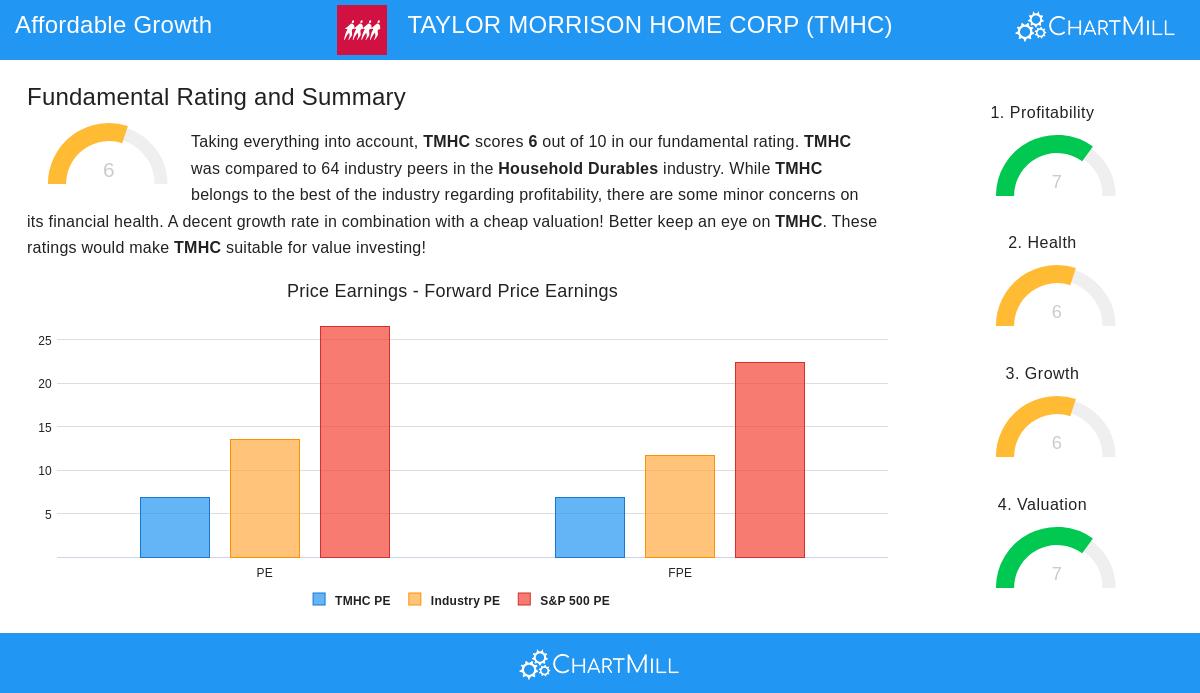

Our analysis gives TMHC a fundamental rating of 6/10, noting strengths in profitability and valuation, though with minor concerns on financial health. The stock trades at a P/E of 6.85, significantly below the S&P 500 average of 26.6, reinforcing its value appeal. Revenue growth has also been steady, averaging 11.4% annually over the past five years.

For a deeper dive, review the full fundamental report here.

Why It Fits GARP

TMHC’s combination of above-average growth, reasonable valuation, and disciplined financial management makes it a compelling option for long-term investors. While housing market cycles pose risks, the company’s focus on diversified markets and strong execution supports its resilience.

Our Peter Lynch Strategy screener lists more stocks matching these criteria, updated daily.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own research before making investment decisions.