TAYLOR MORRISON HOME CORP (NYSE:TMHC) emerged from our Peter Lynch-inspired stock screen as a potential candidate for long-term investors seeking growth at a reasonable price. The company, a residential homebuilder operating in 12 states, demonstrates strong fundamentals while trading at an attractive valuation.

Why TMHC Fits the Peter Lynch Strategy

- Sustainable Growth: TMHC has delivered an impressive 5-year average EPS growth of 23.4%, well within Lynch’s preferred range of 15-30%. This indicates steady, manageable expansion.

- Attractive Valuation: With a PEG ratio of 0.72 (below Lynch’s threshold of 1), the stock appears undervalued relative to its growth potential. The P/E ratio of 6.8 further supports this.

- Strong Profitability: The company’s return on equity (ROE) of 15.2% exceeds Lynch’s minimum requirement of 15%, reflecting efficient use of shareholder capital.

- Healthy Balance Sheet: A debt-to-equity ratio of 0.35 and a current ratio of 5.98 suggest financial stability, with ample liquidity to meet short-term obligations.

Key Takeaways from the Fundamental Report

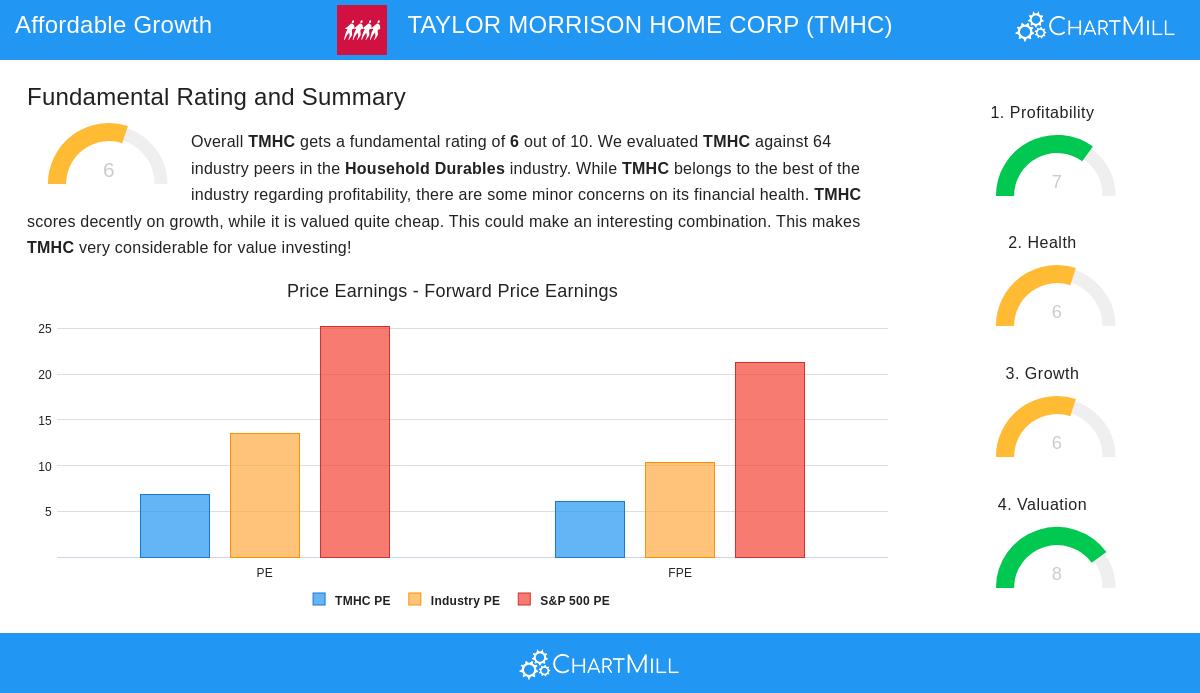

TMHC earns a solid 6/10 in our fundamental analysis, standing out in profitability and valuation within the household durables industry. While growth metrics are strong, there are minor concerns about future revenue expansion, which is expected to slow. The company’s margins and returns on capital, however, remain industry-leading.

For a deeper dive, review the full fundamental analysis of TMHC.

Our Peter Lynch Strategy screener lists more stocks that fit this approach and is updated regularly.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own research before making investment decisions.