For investors looking to balance the search for high-growth companies with fiscal care, the Growth At a Reasonable Price (GARP) or "affordable growth" strategy offers a practical middle path. This method tries to find companies with solid expansion potential but whose shares are not at extreme prices, aiming to reduce some risks found in pure growth investing. A useful way to apply this is by looking for stocks with strong growth ratings, along with good scores in profitability and financial soundness, while checking that the price remains fair. One stock that recently appeared from such a filter is TransMedics Group Inc (NASDAQ:TMDX).

A Snapshot of Fundamental Health

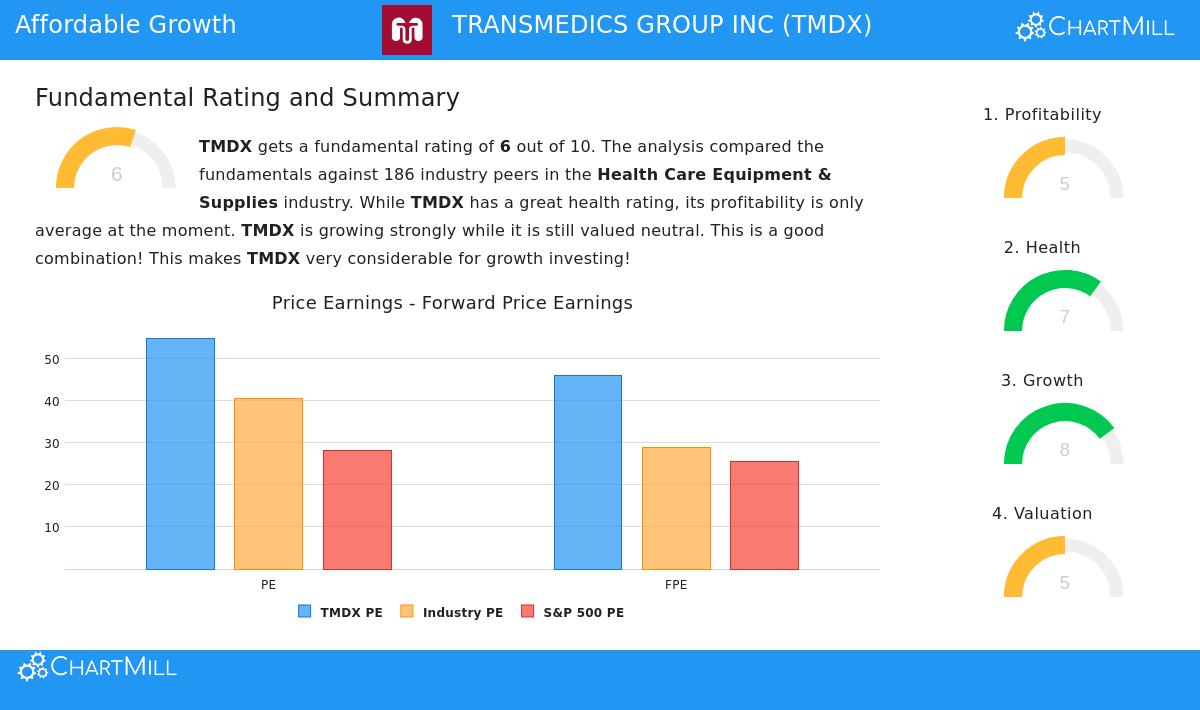

A close fundamental analysis report for TransMedics gives a full, scored look across five key areas: Growth, Valuation, Profitability, Health, and Dividend. For a GARP strategy, the relationship between the first four is especially important. TransMedics gets an overall fundamental rating of 6 out of 10. While this is a moderate score, the individual category ratings show the specific picture that makes it a notable pick for affordable growth screening.

Strong Growth Path

The foundation of any growth investment is growth. TransMedics does very well here, getting a high Growth rating of 8. The company is not only promising future expansion; it is achieving notable results now.

- Impressive Recent Performance: Over the last year, the company's Earnings Per Share (EPS) rose by a remarkable 162.77%, while Revenue increased by 41.20%.

- Continued Historical Growth: Reviewing a longer period, TransMedics has shown a very good multi-year history, with Revenue growing at an average yearly rate of 79.64%.

- Solid Future Outlook: Analyst projections indicate ongoing strong growth, with EPS expected to grow at 33.25% and Revenue at 21.23% on an average yearly basis moving ahead.

This mix of excellent past performance and a good projected growth path is what growth investors seek. It points to a company effectively growing its operations and gaining market position.

A Fair Price in Perspective

A high-growth story often has a high price. The GARP strategy requires examining that price. TransMedics receives a Valuation rating of 5, which shows a neutral position—not clearly low nor overly high. This balance is central to the "affordable" part of the screen.

- Varied Signs on Absolute Measures: On a basic level, numbers like a Price/Earnings (P/E) ratio of 54.95 seem high, particularly next to the wider S&P 500 average.

- Comparative Value Appears: However, price is best judged next to similar companies. Compared to others in the Health Care Equipment & Supplies field, TransMedics seems more fairly priced. Its P/E and Price/Forward Earnings ratios are lower than about 68% of industry rivals.

- Growth Adjustment: Maybe most key for a growth stock, the PEG ratio—which changes the P/E ratio for projected earnings growth—hints at a rather low price. This suggests the market may not completely account for the company's strong growth outlook.

This detailed price picture fits the screen's idea: the stock is not a bargain, but its cost seems acceptable relative to its field and its high growth rate, keeping it from being seen as too expensive.

Supporting Basics: Profitability and Health

For lasting growth, a company requires a stable operational base and a good balance sheet. This is why the affordable growth screen includes reviews for satisfactory Profitability and Financial Health, which serve as risk controls.

TransMedics' Profitability rating of 5 mirrors a change period. While the company has recently become profitable with very good margins (doing better than over 90% of peers on Profit Margin and over 85% on Operating Margin), its past shows variation with several years of negative earnings and cash flow. This is typical in commercial-stage medical technology companies that are growing, but it highlights the need to watch for continued improvement.

The company does well in Financial Health, with a rating of 7. It has very good liquidity, with Current and Quick ratios above 7, showing strong ability to cover short-term needs and beat most industry peers. While it has a significant debt amount (a Debt/Equity ratio of 1.43), this level is still below many competitors, and a good Altman-Z score indicates little near-term bankruptcy concern. This financial strength gives the company the space to keep funding its growth plans.

Conclusion and Next Steps

TransMedics Group Inc presents a notable example for the affordable growth approach. It shows the fast revenue and earnings growth key to the strategy, while its price—though high on a basic level—seems fair within its high-growth industry. The company's excellent liquidity and bettering profitability give fundamental backing to its growth story. This match with the main GARP ideas—strong growth, fair price, and satisfactory supporting basics—makes TMDX a stock worth more study for growth-focused portfolios.

For investors wanting to find other companies that match this careful growth model, more results are available by reviewing the Affordable Growth stock screen.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer to buy or sell any security. Investing involves risk, including the potential loss of principal. You should conduct your own research and consult with a qualified financial advisor before making any investment decisions.