For investors looking for a dependable source of passive income, a methodical selection process is needed to distinguish truly lasting dividend payers from those with possibly risky yields. One useful technique is to select for stocks that not only achieve a high score on a thorough dividend rating but also show good basic financial condition and earnings power. This method favors companies with the business might and cash flow reliability to keep and possibly raise their payments over time, instead of just pursuing the largest stated yields, which can frequently indicate hidden trouble.

TE CONNECTIVITY PLC (NYSE:TEL), a worldwide head in connectivity and sensor solutions, appears as a notable candidate from such a filter. The company’s basic profile indicates it fits well with the standards of a good dividend investment, mixing a reliable income payment with a firm business base.

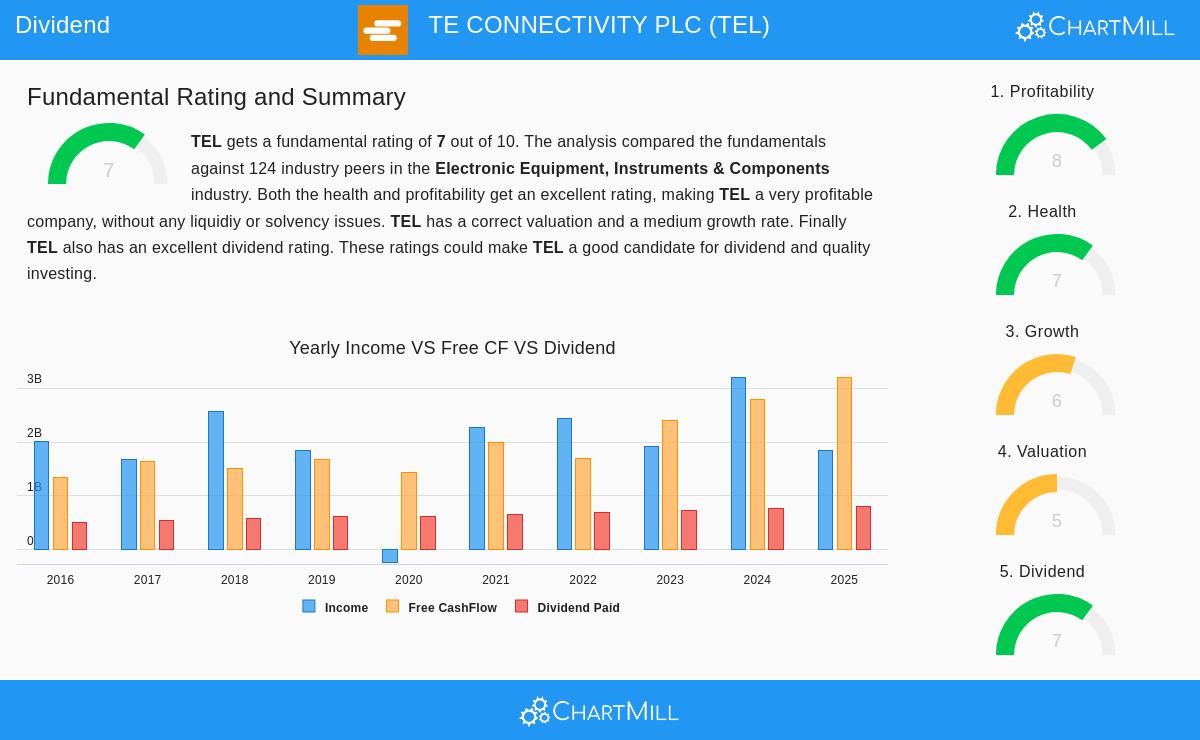

A Firm and Increasing Dividend Profile

Central to the review for TEL is its dividend, which receives a ChartMill Dividend Rating of 7 out of 10. This rating combines a number of important elements that dividend investors focus on.

- Dependable History: TEL has built a reliable record, having paid and, significantly, not reduced its dividend for a minimum of ten years. This steadiness is a sign of a management team dedicated to giving capital back to shareholders across different market periods.

- Lasting Increase: The dividend is not fixed; it has risen at a good yearly rate of 7.56% over the last five years. Importantly, this increase is backed by even greater earnings growth, showing the raises are lasting and not pressuring the company’s resources.

- Moderate Payout: The company pays out about 43.6% of its earnings as dividends. While somewhat elevated, this payout ratio is seen as acceptable, particularly given the company’s earnings power. It keeps a large part of earnings to be put back into the business for future expansion.

The present yield of 1.22% might seem low next to certain high-yield stocks, but it is over two times the average for its field (Electronic Equipment, Instruments & Components) and comes from a position of might, not trouble. This is a key difference for the selection plan, as it steers clear of the trap of high yields that are frequently not maintainable.

The Base: Earnings Power and Financial Condition

A high dividend rating by itself is insufficient; it must be supported by a firm base. This is where the selection standards for "acceptable earnings power and condition" become relevant, and TEL performs well on both counts.

Earnings Power is a clear positive, with a ChartMill Profitability Rating of 8. The company produces very good returns on its invested capital (ROIC of 13.39%), doing much better than more than 90% of its industry competitors. This high degree of capital effectiveness is a strong source of cash flow and a key signal of a lasting competitive edge. Also, TEL keeps firm operating margins of almost 20%, which have been rising in recent years.

Financial Condition is similarly good, getting a rating of 7. The company’s balance sheet is in good order, with an acceptable debt-to-equity ratio of 0.38 and an Altman-Z score firmly in the "safe" area, pointing to a very small chance of financial trouble. A especially revealing measure is the Debt to Free Cash Flow ratio of 1.78, meaning TEL could in theory clear all its debt with under two years of its present cash flow production—a signal of high solvency. While some immediate liquidity ratios are middling compared to the industry, the company’s overall very good solvency and earnings power lessen worries, as they indicate a firm ability to meet commitments.

Valuation and Expansion Setting

From a valuation viewpoint, TEL trades at a P/E ratio similar to the wider S&P 500 but at a lower price than many industry peers. More significantly, its earnings are forecast to expand at a good pace of almost 15% each year in the near future. This expansion possibility helps support its valuation and, more importantly for dividend investors, supplies the driver for future dividend raises. The steadiness between past and forecasted expansion rates indicates a maintainable path.

For a complete look at all these measures, you can examine the full ChartMill Fundamental Analysis Report for TEL.

Conclusion

TE CONNECTIVITY PLC offers an example of the kind of company a quality dividend filter seeks to find. It joins a respectable and reliably increasing dividend yield with the necessary foundation of high earnings power and firm financial condition. This combination indicates a company able to maintain its shareholder returns through its own business quality and cash-producing ability, rather than having to keep up a payment from a weakening situation. For investors whose plan focuses on lasting income and capital protection, TEL deserves further examination.

This review of TEL came from a methodical filter for quality dividend payers. If you want to investigate other companies that meet comparable standards of high dividend ratings together with acceptable earnings power and financial condition, you can execute the Best Dividend Stocks filter yourself.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The information presented is based on data provided and should not be the sole basis for an investment decision. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.