Investors looking for expansion possibilities at fair prices often consider methods that mix development ability with economic strength. The "Affordable Growth" method focuses on companies showing good expansion paths while keeping acceptable basic wellness and earnings, all without high prices. This system helps find businesses that mix development ability with monetary responsibility, possibly presenting good risk-balanced results in different market environments. SPS Commerce Inc (NASDAQ:SPSC) recently appeared from such a filtering method, justifying a more detailed look at its basic qualities.

Growth Path

SPS Commerce shows interesting expansion qualities that build the base of its investment attractiveness. The company's past results and future outlook show a steady habit of development that fits well with affordable growth standards.

- Earnings Per Share has grown by 20.72% over the past year with an average yearly growth rate of 22.07% over recent years

- Revenue increased by 19.28% in the past year, keeping an average yearly growth of 17.97% over several years

- Forward outlooks point to expected EPS growth of 15.51% and revenue growth of 11.71% each year

This maintained expansion pattern across both top-line revenue and bottom-line earnings indicates the company has built a lasting development model. While future growth estimates show some slowing next to past rates, they stay noticeably above market averages, placing SPSC firmly in the growth stock group.

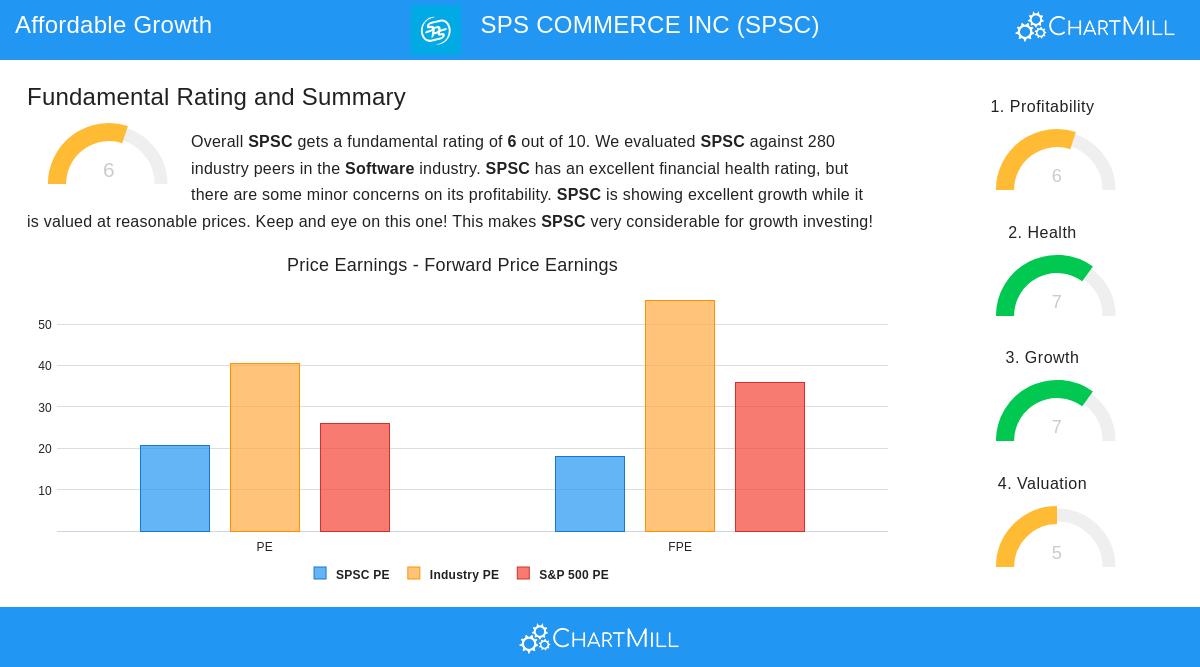

Valuation Review

The valuation view for SPS Commerce shows a varied but mostly acceptable situation relative to its expansion prospects. The company's valuation numbers sit in a noteworthy middle area that may interest growth investors aware of cost.

- Current Price/Earnings ratio of 20.67 sits below the industry average of 40.43 and the S&P 500 average of 25.98

- Price/Forward Earnings ratio of 17.92 compares well to industry and wider market benchmarks

- Enterprise Value to EBITDA and Price/Free Cash Flow ratios rank lower priced than about 80% and 77% of industry peers respectively

- PEG ratio indicates suitable valuation compensation for expected growth rates

While some absolute valuation measures might seem high, the setting of the company's expansion path and industry place indicates the extra cost may be warranted. The valuation becomes more acceptable when thinking about the company's growth expectations and earnings profile.

Financial Condition and Earnings

Beyond growth and valuation, SPS Commerce shows acceptable base qualities that support its affordable growth idea. The company keeps economic steadiness next to respectable earnings measurements.

The financial condition view shows particular force in solvency, with no remaining debt and an Altman-Z score of 11.05 showing low bankruptcy danger. Current and quick ratios around 1.97 indicate suitable cash management. However, investors should note the company has been raising shares outstanding in recent years, which is a small worry.

Earnings measurements show a company doing acceptably within its competitive field:

- Return on Assets of 7.34% does better than 79% of industry peers

- Operating Margin of 14.85% places in the top fifth of the software industry

- Profit Margin of 11.66% beats almost three-quarters of rivals

These earnings measures, while not outstanding, show the company's ability to turn growth into profits successfully. The mix of good financial condition and acceptable earnings gives a steady base for continued growth performance.

Investment Points

SPS Commerce presents an interesting case for investors following affordable growth methods. The company's steady past growth, fair valuation relative to prospects, and acceptable economic base make an attractive profile. The lack of dividend payments matches with growth-centered reinvestment of money, while the debt-free balance sheet gives operational adaptability.

The company's place in cloud-based supply chain management services represents a developing market part, possibly supporting continued expansion. However, investors should watch the speed of revenue growth relative to valuation multiples and judge whether future results warrant current pricing.

For investors curious to find similar possibilities, other affordable growth options can be found through our dedicated filtering tool. This resource allows adjustment of growth, valuation, condition, and earnings factors to find companies meeting specific investment standards.

This article presents factual information and analysis for educational purposes only and does not constitute investment advice, recommendation, or endorsement of any security. Investors should conduct their own research and consult with financial advisors before making investment decisions. Past performance does not guarantee future results, and all investments carry risk including potential loss of principal.