Oil crossed back above $100 a barrel as Iran–US diplomacy showed its cracks, a climbing 10-year yield hammered the tech sector, and fresh redemption gates at two of the largest private credit funds raised uncomfortable questions about liquidity in a $1.8 trillion market. Tuesday delivered more than enough to keep investors on their toes heading into Wednesday's session.

If anyone thought Monday's diplomatic relief rally had given markets a clean bill of health, Tuesday had a very different opinion.

The optimism evaporated almost as quickly as it had arrived, oil roared back above $100, the Nasdaq slid nearly a full percent, and the bond market sent another pointed reminder that it isn't done squeezing. I'll walk you through everything that matters for your portfolio today.

Geopolitics Back in the Driver's Seat

The Iran–US standoff is refusing to fade into the background. On Monday, President Trump announced a five-day halt on strikes against Iranian energy infrastructure, claiming a diplomatic breakthrough was imminent. Markets rallied briefly.

By Tuesday, Tehran was pushing back hard, denying that any concrete negotiations had taken place, and Iranian forces conducted fresh military actions, including strikes on Tel Aviv and targets across the Gulf region. According to reporting by The Wall Street Journal, Saudi Arabia and other US allies in the region were also considering entering the fray.

The Strait of Hormuz remains effectively blocked. That is not a minor footnote, approximately 20% of the world's daily oil supply transits that narrow waterway, and with the disruption ongoing, the market is doing what markets do: pricing in fear and uncertainty.

Brent crude surged 4.6% to $104.49 a barrel, while WTI gained 4.8% to $92.35, reversing Monday's brief retreat. The olietransport disruption has created a daily deficit of some 13.5 million barrels, a figure that is extraordinarily difficult to absorb in the short term.

Citibank published a note on Tuesday that is worth paying attention to. Its analysts warned that Brent could reach at least $120 per barrel within the next month, and that if disruptions persist through the end of June, prices could theoretically climb toward $200, a scenario that, if realised, would make today's inflation concerns look modest by comparison.

I wouldn't anchor to that $200 figure as a base case, but the directional message is clear: the energy risk premium in this market is nowhere near fully priced in yet.

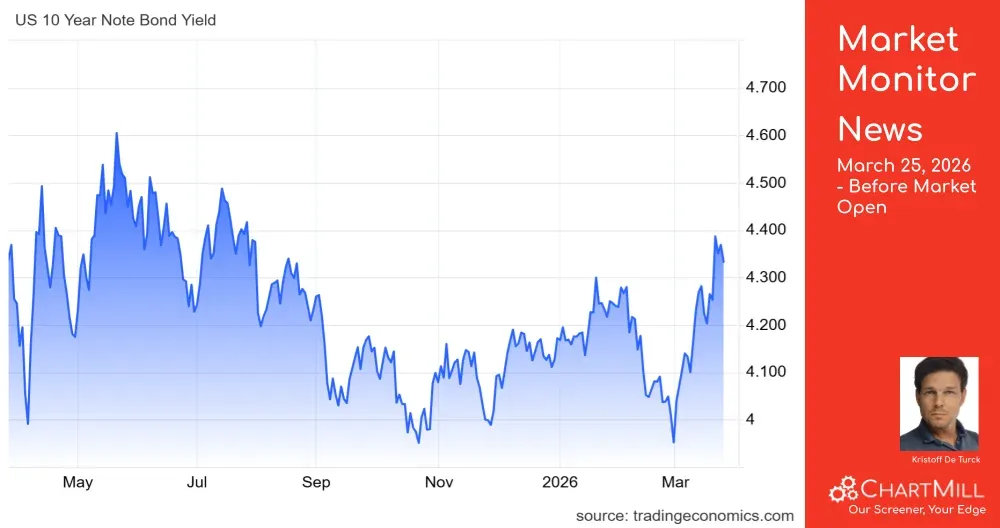

Rates Squeeze Tech Again

The geopolitical noise wasn't the only drag on Tuesday's session. The US 10-year Treasury yield ticked back up 4 basis points to 4.38% - its highest level since July 2025 - reversing Monday's brief cooling.

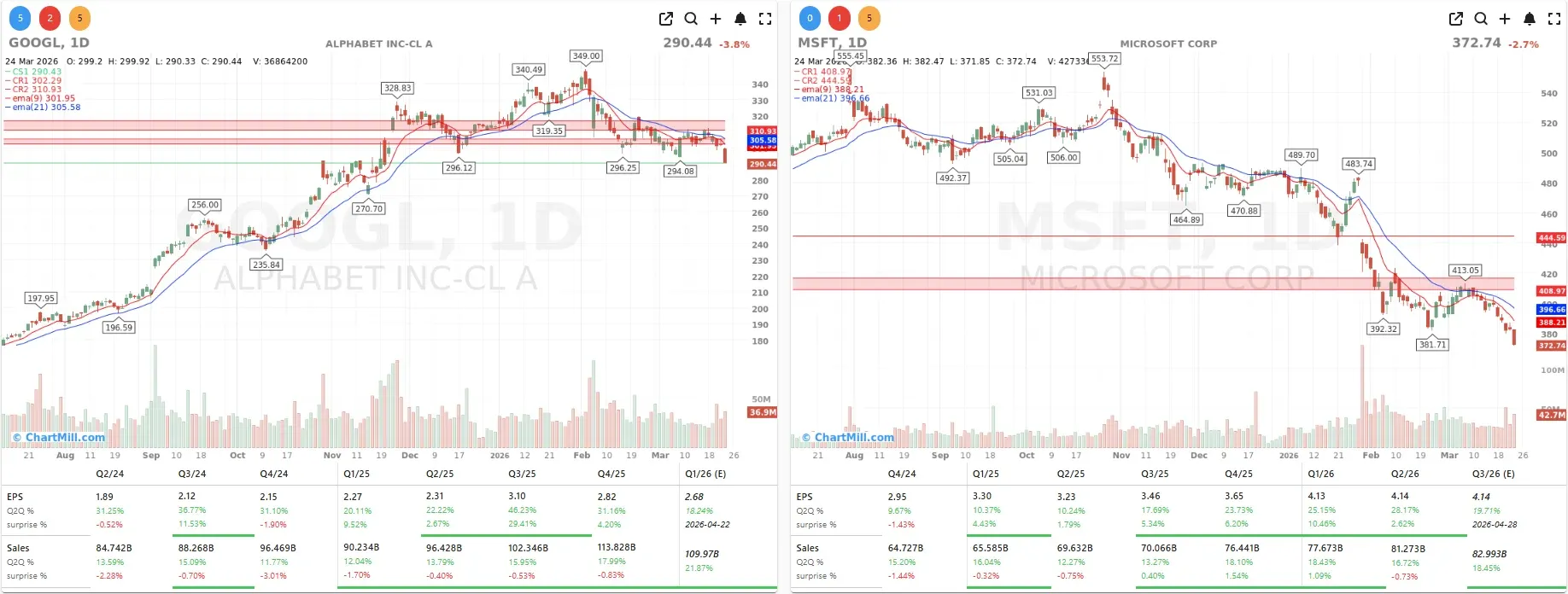

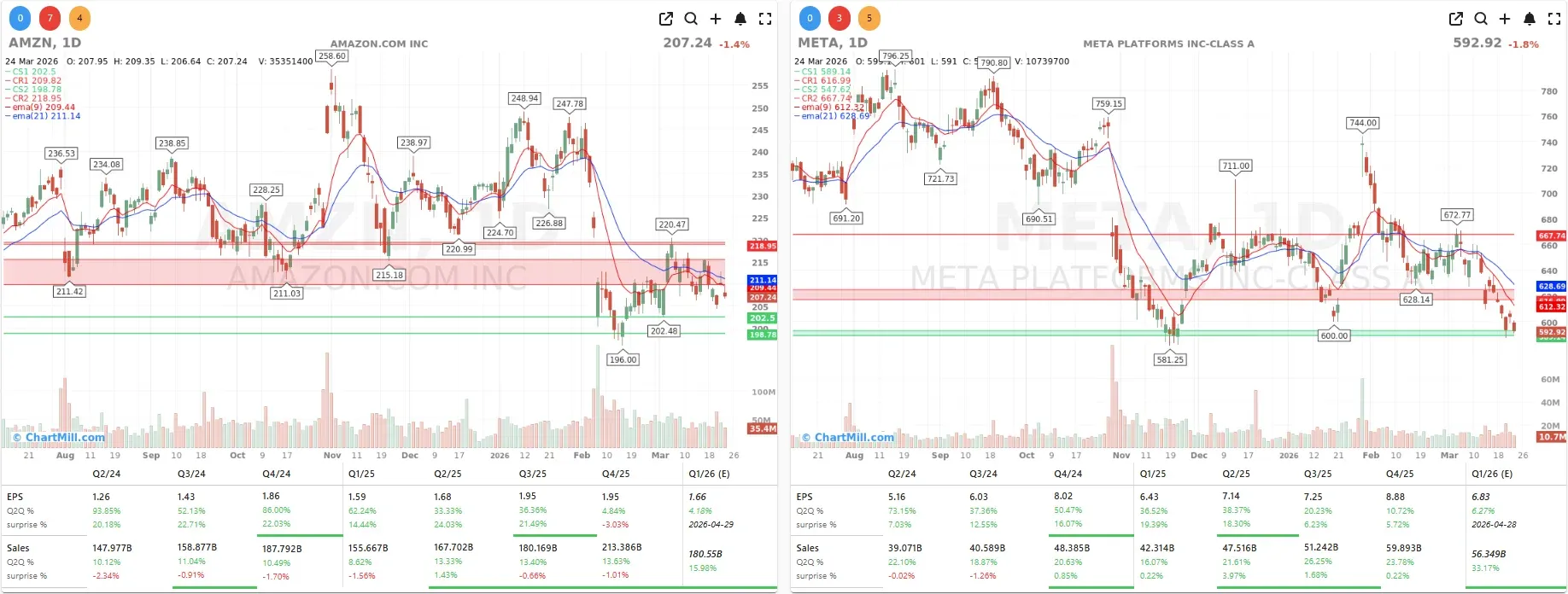

Rising long-term yields are the natural adversary of high-multiple growth stocks, and the tech sector bore the brunt.

Microsoft MSFT | ▼2.68%, Alphabet GOOGL | ▼3.85%, Amazon AMZN | ▼1.38%, and Meta Platforms META | ▼-1.84% all fell meaningfully as investors once again rotated out of the Magnificent Seven.

The pattern is familiar by now: every time there is a hint of rate relief, growth stocks breathe a little easier and every time the 10-year ticks back up, the same names take the hit.

What is harder to dismiss is the structural nature of this pressure. With oil prices putting upward stress on inflation expectations and the Fed in a tight spot, there is no obvious catalyst that will push the 10-year meaningfully lower in the near term. That's a headwind worth keeping in mind for anyone carrying heavy tech exposure.

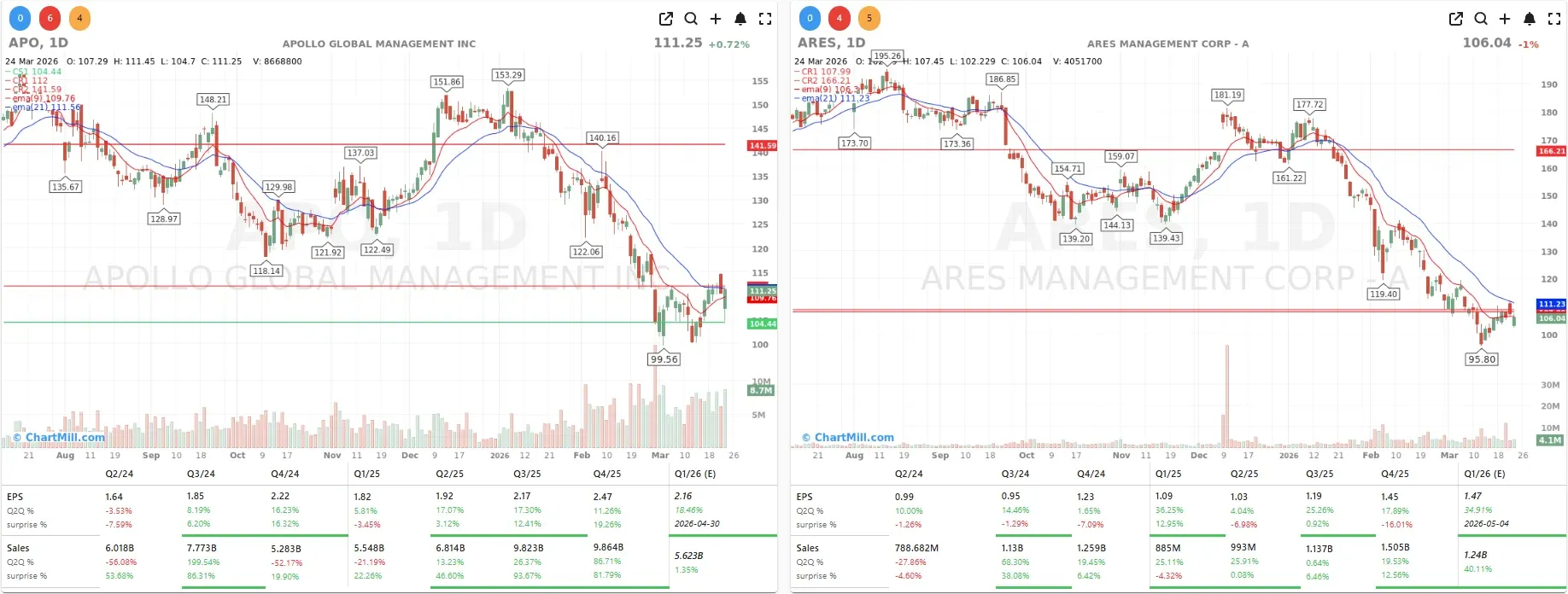

Private Credit's Pressure Valve

There is a story building quietly in the world of private credit, though Tuesday made it considerably louder. Two of the biggest names in alternative lending, Ares Management ARES | ▼1.01% and Apollo Global Management APO | ▲0.72%, were forced to cap investor redemptions from their flagship private credit funds.

Ares saw redemption requests surge to 11.6% of its $10.7 billion Strategic Income Fund, well above the 5% quarterly limit the fund is permitted to honour. Apollo's situation was equally constrained: the firm capped outflows at just 45% of what investors requested from its Debt Solutions fund.

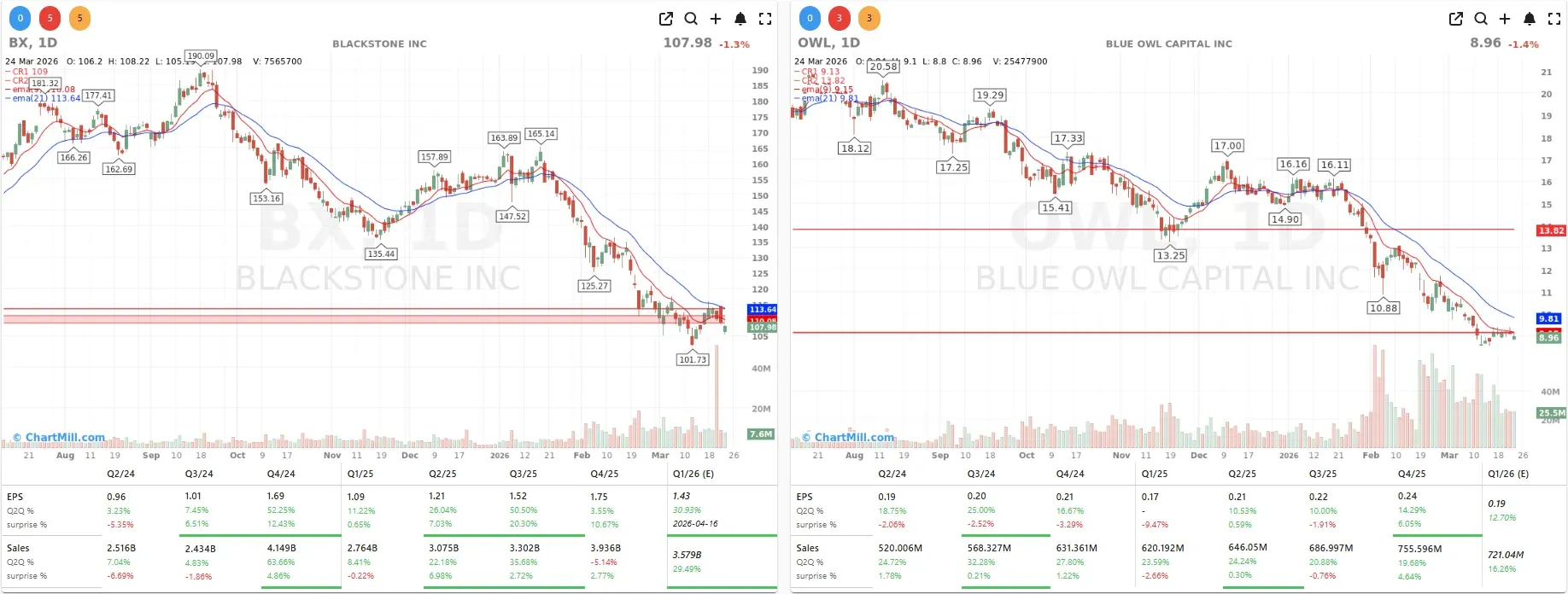

At one point during the session, this news had collectively wiped out more than $10 billion in market capitalisation across Ares, Apollo, Blackstone BX | ▼1.25%, and Blue Owl Capital OWL | ▼1.43%. The closing prices were more forgiving - Apollo even managed to finish the day in positive territory - but the underlying signal deserves attention.

Private credit, the $1.8 trillion market that has thrived in an environment of bank retrenchment, carries structural illiquidity by design. In benign times, that is a feature. In environments like this one, rising rates, geopolitical stress, and investors seeking safety, it becomes a vulnerability. I think we are only in the early innings of this conversation.

Corning's Remarkable Run Continues

Not every headline on Tuesday belonged in the red column.

Corning GLW | ▲8.43% had an exceptional session, its shares climbing sharply as the market continued to reward the company's multi-year, up to $6 billion fiber optic supply agreement with Meta Platforms META | ▼1.84%.

Announced in January, the deal - the largest in Corning's history - will see the company supply advanced fiber optic cables for Meta's aggressive AI data center buildout across the United States, anchoring a significant capacity expansion at Corning's North Carolina manufacturing facilities. The stock is now up some 65% year-to-date.

For a company that most investors would historically have placed in the "boring industrials" bucket, it has become one of the most compelling infrastructure plays in the AI era.

Company News: Winners, Losers, and a Meme Stock

Smithfield Foods SFD | ▲4.26% delivered strong quarterly results, sending its shares meaningfully higher. The packaged meat producer continues to benefit from stable consumer demand and disciplined cost management, a reassuring data point at a time when consumer staples are earning their keep as a defensive holding.

On the healthcare front, Gilead Sciences GILD | ▲0.56% announced a definitive agreement to acquire Ouro Medicines in a deal worth up to $2.18 billion. At its core is OM336 (gamgertamig), a clinical-stage T cell engager therapy targeting autoimmune diseases, which has shown early but genuinely impressive results in severe orphan conditions including autoimmune haemolytic anaemia and immune thrombocytopenia.

More intriguing is the strategic dimension: Gilead is in advanced discussions with Galapagos GLPG | ▼6.58% on a potential collaboration that would see the Belgian-Dutch biotech co-fund 50% of the acquisition cost and absorb Ouro's operating assets, while Gilead retains global commercialisation rights.

The market's reaction to Galapagos was unforgiving, uncertainty and a large capital commitment is rarely a recipe for an immediate share price pop, but the longer-term strategic logic of getting closer to Gilead's pipeline is hard to dismiss entirely.

In the EV space, two very different stories are unfolding in Europe.

Tesla TSLA | ▲0.57% improved its EU market share from 1.2% to 1.6%, with 13,740 vehicles registered in February, a 29% year-on-year improvement. A solid result.

And yet, BYD BYDDY | ▲1.7% is showing what ambition at scale actually looks like: 15,438 European registrations in February, up 185% year-on-year. The Chinese manufacturer is rewriting the competitive map of European electromobility at a pace that should demand attention from every portfolio with significant legacy auto exposure.

After market close, GameStop GME | ▼0.96% released its Q4 2025 results.

Revenue fell 14% to $1.10 billion, materially missing expectations. Core hardware, accessories, and software sales continued their structural decline, hardly a surprise. On the other hand, the EPS print of $0.49 comfortably beat the $0.37 consensus estimate, partly driven by the collectibles business (now one-third of revenue, up from 21% a year ago) and income from its substantial cash position of $6.3 billion.

The company's 4,710 Bitcoin holdings were a drag, losing approximately $150 million in value during the quarter. In after-hours trading, the stock swung between $21.78 and $23.30, which is about as orderly as GameStop gets.

Macro Footnote

On the data side, US labour productivity in Q4 rose less than the initial estimate suggested, while unit labour costs came in higher than previously reported.

It is not a market-moving print in isolation, but it adds another layer of complexity for the Federal Reserve as it tries to navigate a world of oil price shocks and stubbornly elevated services inflation.

The euro slipped 0.3% against the dollar to 1.1586, reflecting ongoing dollar demand in an environment where geopolitical risk premiums tend to flow into the greenback.

Conclusion

Markets are navigating several overlapping fault lines at once: a geopolitical crisis with the potential to fundamentally reshape global energy flows, a rate environment that remains hostile to growth valuations, and structural vulnerabilities in shadow banking that are only now being properly stress-tested.

The Corning surge and the resilient close in Apollo shares are welcome notes of colour, but they do not change the broader picture.

With oil potentially heading toward $120 or beyond, the Federal Reserve watching every data point for signs of renewed inflation, and private credit investors reaching for the exit door, this is not an environment where complacency pays.

Stay disciplined, watch the 10-year yield carefully, and don't underestimate the energy story, it has further to run.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.