For investors looking to balance the search for growth with prudence, the Growth at a Reasonable Price (GARP) or "affordable growth" strategy offers a practical middle path. This method seeks to find companies with strong and sustainable growth, but whose shares are not valued at very high levels. The aim is to sidestep the large price swings common with speculative growth stocks while still gaining from meaningful appreciation. Finding these chances needs a multi-part examination of a company's basics, comparing its growth outlook with its current price, and also confirming its core financial soundness and earnings strength are good.

One stock that recently appeared from this careful screening is SANMINA CORP (NASDAQ:SANM). The company, which provides integrated manufacturing solutions and parts for markets including industrial, medical, aerospace, and cloud infrastructure, shows a basic profile that fits the affordable growth idea. A full fundamental analysis report on the stock displays a balanced set of scores, with specific strong points in areas important for this investment approach.

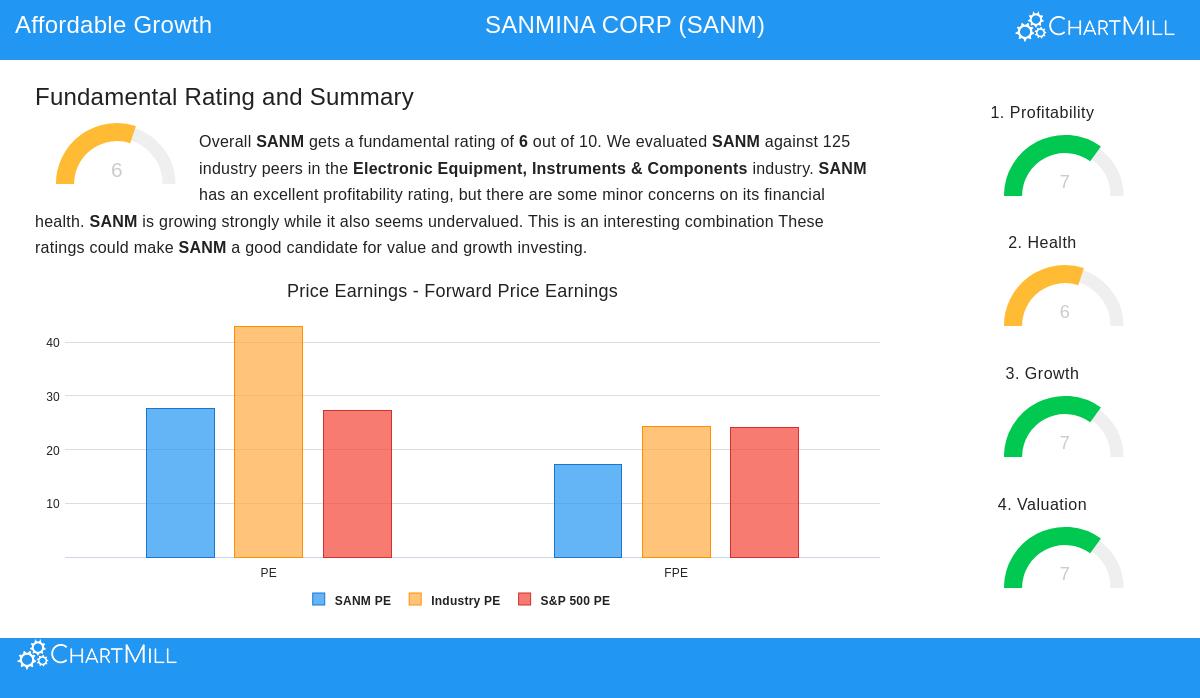

Growth: A Current and Coming Strength

The central idea of any growth plan is, expectedly, growth. Sanmina’s profile indicates strength in both its recent results and its expected future. The company’s Growth score of 7 out of 10 is supported by good past measures and especially strong expectations.

- Past Growth: In the last year, Sanmina increased its Earnings Per Share (EPS) by 14.58%, with a steady average yearly EPS growth of 14.53% over several years. Sales growth has been more moderate but stable.

- Quickening Future View: The most notable numbers are in the forward estimates. Analysts predict average yearly EPS growth of about 38.6% and sales growth of almost 40% for the next years. The report states this shows a clear quickening from past rates, a good sign for growth investors.

- Strategic Value: For an affordable growth screen, quickening future growth is a vital filter. It implies the company is seizing new possibilities or getting more efficient, supplying the basic "engine" that could push shareholder gains.

Valuation: Sensible Even With High Growth

Finding strong growth is only part of the task, paying a fair price for it is what makes the "affordable" part. Sanmina’s Valuation score of 7 suggests the market may not be completely valuing its growth path, offering a possible chance.

- Varied Traditional Measures: On first look, a P/E ratio of 27.6 seems elevated. However, context is key. This ratio is actually lower than 67% of similar companies in the Electronic Equipment, Instruments & Components field and matches the wider S&P 500 average.

- Forward and Comparative Value: More indicative is the Forward P/E ratio of 17.3, which is lower than over 81% of industry rivals and rests below the S&P 500 average. Also, measures like Enterprise Value to EBITDA and Price to Free Cash Flow show Sanmina trading at a lower level than most of its industry peers.

- Growth Adjustment: The most persuasive valuation point for a GARP investor is the PEG Ratio (NY), which modifies the P/E for expected earnings growth. Sanmina’s low PEG ratio is noted in the report as a sign of a "rather low valuation," implying the stock price has not risen with the higher growth forecasts.

Profitability and Financial Health: The Supporting Base

An affordable growth plan must check more than just growth and price to judge the quality and durability of the business. A company can grow fast but use cash poorly, or have too much debt that risks its future. Sanmina gets a 7 for Profitability and a 6 for Financial Health, giving a satisfactory base.

- Profitability Measures: The company shows steady earnings with positive profits and cash flow over the past five years. Its Return on Invested Capital (ROIC) of 9.97% is good, beating 85.6% of industry peers, showing efficient use of money to create profits. While gross margins are somewhat narrow,a trait of the manufacturing sector, both operating and profit margins have been getting better.

- Financial Health Review: The balance sheet shows little reason for concern. The company has a very low Debt/Equity ratio of 0.12 and a very good Debt to Free Cash Flow ratio of 0.63, meaning it could pay off all its debt in under a year using its cash flow. The primary point of care is in liquidity, where its Current and Quick ratios are below many industry peers, though still at levels usually seen as acceptable.

Conclusion

Sanmina Corp presents an example in the affordable growth screening idea. It joins quickening, double-digit growth forecasts in both profits and sales with a valuation that seems sensible, if not low, compared to its industry and growth profile. This pairing of a high-growth engine and a fair price is the main goal of the GARP strategy. Backed by good profitability and a largely sound balance sheet with little debt, the company’s basics indicate it is growing from a place of strength, not guesswork.

Naturally, Sanmina is only one instance that met this particular group of filters. Investors wanting to find other companies that fit similar standards of good growth, sensible valuation, and satisfactory financials can review more results using the Affordable Growth stock screen.

Disclaimer: This article is for information only and is not financial advice, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own study and think about their personal money situation and risk comfort before making any investment choices.