For investors looking for chances where a company's market price may not show its actual business condition, a systematic filtering method can point out possible choices. One way is to find stocks that have a good basic value score while also holding fair ratings in other important parts like earnings, money stability, and expansion. This technique tries to find companies that are not only low in price, but are also supported by good operating results and a firm money position, possibly giving a safety buffer for investors focused on value.

Sanmina Corp (NASDAQ:SANM) provides integrated manufacturing solutions and parts, serving fields from industrial and medical to defense, aerospace, and communications. A recent filter for "fair value" stocks, which focuses on a good value rating together with acceptable basics, has shown SANM as a company that deserves more attention. The company's detailed fundamental analysis report gives an organized review of its money situation.

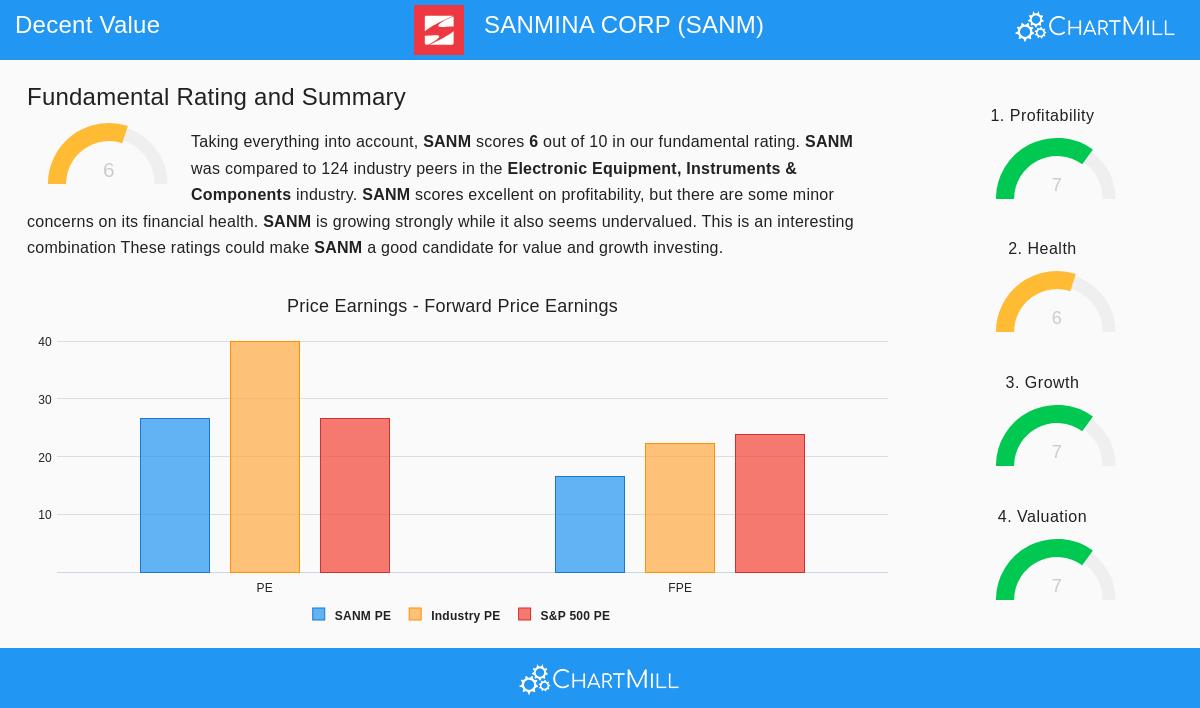

Valuation: An Interesting Entry Point

The center of any value investment idea is valuation, deciding if a stock trades for less than its real worth. SANM's valuation numbers show a varied but finally interesting view when seen in situation.

- Relative Value: While its normal Price-to-Earnings (P/E) ratio of 26.55 matches the wider S&P 500, it looks much more appealing inside its own field. SANM costs less than about 66% of similar companies in the Electronic Equipment, Instruments & Components field based on this number.

- Forward-Looking and Cash-Based Numbers: The argument gets stronger when looking at forward earnings and cash flow. The company's Price/Forward Earnings ratio of 16.60 is lower than over 81% of field rivals and is under the S&P 500 average. Also, its Price/Free Cash Flow ratio is more appealing than almost 85% of field peers, hinting the market might be setting too low a value on the cash the business produces.

- Growth Compensation: Importantly, SANM's valuation seems to overlook its firm growth path. The low PEG ratio, which changes the P/E for expected earnings growth, shows the stock may be low priced compared to its future possibility. This matching of fair price measures with good growth outlooks is a main feature wanted by value investors who think the market has not yet valued the company's getting better prospects.

Financial Health: A Steady Base

A low-priced stock is only a good investment if the company is financially stable enough to last through economic changes and carry out its plan. SANM's financial health rating of 6 out of 10 points to a mostly steady, though not outstanding, base.

- Strong Solvency: The company shows very good solvency numbers. Its debt-to-free-cash-flow ratio of 0.63 is very firm, showing it could pay all its debt in under a year using its present cash flow, doing better than 84% of its field. The Debt/Equity ratio of 0.12 also shows a careful money structure.

- Liquidity Points: The report mentions some small worries about short-term money access. Both the Current Ratio (1.72) and Quick Ratio (1.02) are lower than many field peers. While these levels are not worrying and suggest the company can meet its needs, they are an area for investors to watch, highlighting the need for a complete look beyond valuation only.

Profitability and Growth: The Driver for Value Achievement

For a value investment to succeed, the basic business must earn money and preferably be expanding. A very low stock in a lasting downturn is a "value trap," not a chance. SANM scores a 7 for both profitability and growth, showing the operating force required to possibly support a higher valuation later.

- Steady Profitability: SANM has been steadily profitable with positive earnings and operating cash flow over the last five years. Its Return on Invested Capital (ROIC) of 9.97% does better than 84% of the field, showing efficient use of money. While its Gross Margin is fairly low for the field, both its Operating Margin and Profit Margin have been getting better and are above the field middle point.

- Speeding Up Growth Picture: The growth story is especially noticeable. While past income growth has been small, earnings per share (EPS) have grown at a sound rate of over 14% each year. More importantly, outlooks for the future are much more positive. Analysts forecast average yearly EPS growth of almost 39% and income growth of nearly 40% in the coming years. The report clearly says that the growth rate is speeding up, which could be a reason for a market re-valuation if those forecasts happen.

Conclusion

Sanmina Corp shows an interesting case for investors using a systematic value filter. It is not a very low-value stock trading at very low earnings measures, but instead a company that seems fairly or lowly valued compared to its field and, most importantly, its own future growth possibility. The mix of a good valuation score, firm profitability, acceptable financial health, and a quickly speeding up growth picture hints the market may be valuing the company's prospects too low. This fits with the value investing rule of looking for a safety buffer, not only from a low price, but from a price that does not include getting better basics.

For investors wanting to look into similar chances that mix appealing valuation with firm basics, more study can start with the Decent Value Stocks screen used to find SANM.

Disclaimer: This article is for information only and does not make financial advice, a suggestion, or an offer to buy or sell any security. Investing includes risk, including the possible loss of original money. Readers should do their own complete study and think about their personal money situation and risk comfort before making any investment choices.