For investors looking for opportunities where the market price may not fully show a company's actual worth, a disciplined screening process can be a good beginning. One such method is to look for companies that seem basically priced below their worth by the market while still showing good operational health and earnings. This approach matches central value investing ideas, which concentrate on finding securities trading for less than their real value, often because of short-term negative views or sector-wide inattention. The aim is to find businesses that are not just low-priced, but are financially stable and able to produce returns, thus offering a possible "margin of safety."

RANGE RESOURCES CORP (NYSE:RRC), an independent natural gas company concentrated on the Appalachian Basin, comes from such a screen. The company's basic profile indicates it may stand for the kind of below-value opportunity value investors search for, joining a good price with firm earnings measures.

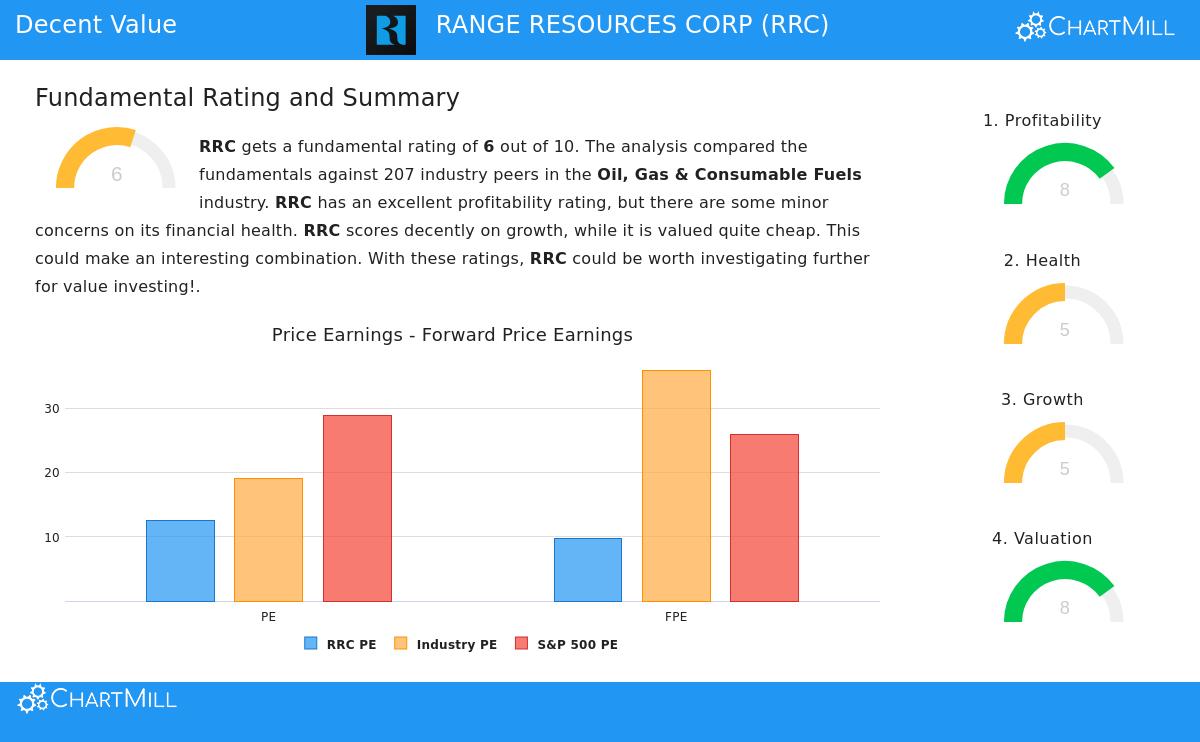

Valuation: The Center of the Opportunity

The main attraction of RRC for a value-focused screen is in its pricing measures. The company's stock seems priced carefully compared to both its present earnings and future outlook, especially when measured against wider market indexes.

- Price-to-Earnings (P/E) Ratio: At 12.46, RRC's P/E ratio is much lower than the S&P 500 average of near 28.82. This shows the market is pricing its earnings at a large reduction to the wider market.

- Forward P/E Ratio: The price becomes even more interesting looking forward. With a forward P/E of 9.71, RRC costs less than over 82% of similar companies in the Oil, Gas & Consumable Fuels industry and stays greatly reduced versus the S&P 500's forward P/E average of about 25.95.

- PEG Ratio: The Price/Earnings to Growth (PEG) ratio, which includes expected earnings growth, is low. This indicates the stock's present price does not completely account for its expected growth, a main sign for value investors looking for growth at a fair price.

For a value plan, a low price is the beginning. It gives the possible cushion, or margin of safety, that Benjamin Graham stressed. If the company's basics are good, as the screen demands, this reduction may show a pricing error the market could fix over time.

Profitability: Showing Operational Firmness

A low-cost stock is only a sound investment if the company earns money. RRC does well here, with a ChartMill Profitability Rating of 8 out of 10. This firmness is clear across several main measures:

- Return Measures: The company shows firm returns on its used capital. Its Return on Invested Capital (ROIC) of 9.41% does better than over 80% of its industry peers, showing efficient use of capital to create profits.

- Good Margins: RRC keeps strong earnings margins. An operating margin of 27.17% and a net profit margin close to 20% put it in the top half of its industry. Especially, its gross margin is over 90%, displaying the basic economics of its natural gas production.

Strong and steady earnings are essential for a careful value investment. It confirms the business model works and that the "real value" an investor is counting on is supported by actual earnings ability, not just assets on a balance sheet.

Financial Health: A Varied but Acceptable View

Financial health makes sure a company can survive economic declines and keep operating without trouble. RRC's health rating is a middle 5, giving a balanced view with clear strong points and a clear weak point.

- Solvency Strong Points: The company's balance sheet shows good signs. Its Debt-to-Equity ratio of 0.29 is acceptable and better than most industry peers. Also, its Debt-to-Free-Cash-Flow ratio of 2.46 is seen as good, meaning it could in theory pay off all debt in under two-and-a-half years using its cash flow.

- Liquidity Watch Point: The main area for care is short-term cash availability. RRC's Current and Quick ratios are both 0.56, which is low and shows possible difficulties in paying immediate debts without using future cash flow or new financing. This is a usual trait in capital-heavy industries like energy but needs investor notice.

For value investors, checking financial health is key to avoid "value traps", companies that are low-cost for a reason, often because of a worsening balance sheet. While RRC's cash availability is a point to watch, its good solvency measures and strong cash flow creation help lessen this worry.

Growth: A Steadying Path

Growth gives the reason for a price change. RRC's growth profile, rated a 5, shows a company changing with good forward-looking signs.

- Past Results: The company has a strong history of Earnings Per Share (EPS) growth, averaging close to 43% each year over recent years. However, revenue has had small drops, pointing to a focus on efficiency and margins rather than sales increase.

- Future Predictions: The view is more all positive. Experts expect a return to revenue growth (close to 13% each year) along with solid EPS growth going forward. This expected increase from past revenue trends is a good sign.

Value investing does not need fast growth, but a fair growth path supports the idea that real value will rise over time. RRC's expected move to growth in both sales and earnings could help reduce the price difference.

Conclusion and Next Steps

Based on a basic review, RANGE RESOURCES CORP presents a case that fits a disciplined value-looking plan. It trades at a clear reduction to the market and its own future earnings possibility, while showing central strong points in earnings and capital returns. The company's financial health is sufficient, though its low cash availability measures deserve attention. The expected return to revenue growth could act as a reason for change.

It is key to see this review as a beginning for more detailed research. The energy sector changes with cycles and is affected by commodity prices, rule changes, and big economic factors. Investors should think about these industry-specific risks along with the company's basics.

For investors curious about screening for similar opportunities that balance price with basic firmness, you can look at the Decent Value Stocks screen on ChartMill.

,

Disclaimer: This article is for information only and does not make financial advice, a suggestion, or an offer or request to buy or sell any securities. The review is based on data and sources thought to be dependable, but its correctness cannot be sure. Investing has risk, including the possible loss of original money. You should do your own research and talk with a qualified financial advisor before making any investment choices.