When looking for reliable dividend-paying stocks, investors often use screening methods that consider several fundamental factors. One useful method involves finding companies with good dividend traits while also having good profitability and financial condition. This process helps steer clear of high-yield situations where payouts that cannot continue hide problems in the business. By concentrating on stocks that perform well in these areas, investors can create a portfolio of companies able to maintain and possibly increase their dividends over time.

RESMED INC (NYSE:RMD) appears as a notable candidate through this screening view, especially for investors who value dividend dependability along with business quality. The medical device company's fundamental picture shows why it is notable in dividend-focused plans.

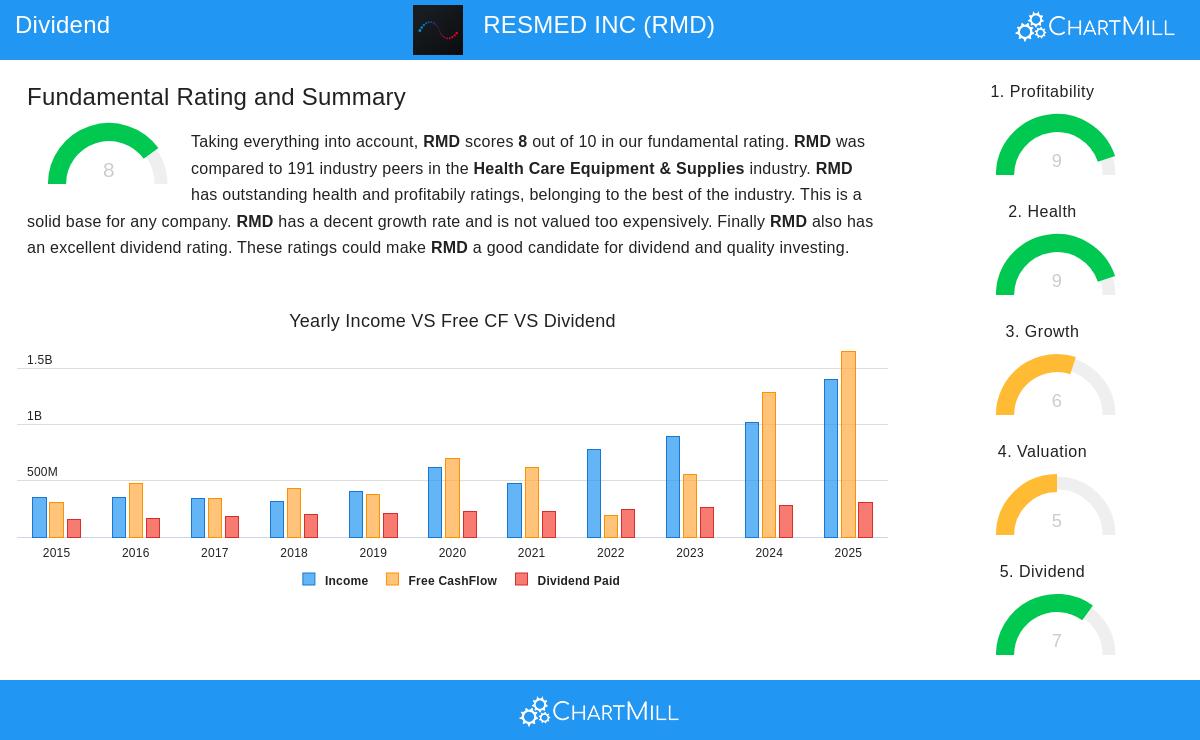

Dividend Dependability and Growth

The company's dividend traits are a central part of its attraction for investors focused on income. While the present yield of 0.86% may seem low next to some high-yield choices, the basic numbers tell a more notable story about sustainability and growth possibility.

- Steady Dividend Growth: ResMed has raised its dividend at a yearly rate of 6.33% over recent years, showing management's dedication to giving capital back to shareholders

- Established History: The company has kept up dividend payments for more than ten years without decreases, giving trust in its distribution policy

- Maintainable Payout Ratio: With only 22.19% of earnings used for dividend payments, ResMed keeps a large buffer to continue payouts during economic declines

These dividend qualities match well with screening rules that value sustainability over high yield. The company's careful method for dividend growth, along with its low payout ratio, lowers the chance of future reductions that often trouble high-yield plans.

Profitability Supporting Dividend Sustainability

ResMed's very good profitability supplies the basic engine for its dividend abilities. The company reaches returns that are much higher than industry averages, creating sufficient profits to pay for both business reinvestment and shareholder returns.

-

Better Return Measures:

- Return on Assets: 17.14% (does better than 97% of industry peers)

- Return on Equity: 23.47% (is higher than 96% of competitors)

- Return on Invested Capital: 19.35% (beats 98% of the industry)

-

Good Margin Picture:

- Operating margin of 32.76% is in the top 1% of the healthcare equipment sector

- Profit margin of 27.22% is higher than 95% of industry counterparts

- Both operating and profit margins have gotten better in recent periods

This profitability quality directly backs the screening method's focus on companies with strong earnings power. High returns show competitive benefits and operational effectiveness, which then support steady dividend payments without weakening financial condition.

Financial Condition Supporting Long-Term Payouts

ResMed's sound balance sheet and liquidity situation give extra confidence for dividend sustainability. The company keeps financial numbers that suggest very little risk to its distribution abilities even in difficult economic times.

-

Solvency Strength:

- Altman-Z score of 13.47 shows very little bankruptcy risk

- Debt-to-Equity ratio of 0.11 shows small dependence on borrowing

- Debt-to-Free-Cash-Flow ratio of 0.40 means the company could pay back all debt in under five months using present cash flow

-

Liquidity Situation:

- Current ratio of 3.44 shows good short-term financial condition

- Quick ratio of 2.53 shows enough liquid assets compared to immediate liabilities

- Both ratios are higher than about two-thirds of industry peers

The focus on financial condition in dividend screening plans is especially fitting for ResMed. Good liquidity and solvency numbers make sure the company can get through economic cycles while keeping its dividend, speaking to a main worry for income-focused investors.

Balanced Valuation Perspective

While ResMed trades at a P/E ratio of 28.27, putting it close to S&P 500 averages, several factors give valuation perspective for dividend investors. The company's valuation seems more fair when thinking about industry comparisons and future growth prospects.

- The forward P/E ratio of 24.66 is below 75% of healthcare equipment companies

- Enterprise Value to EBITDA and Price/Free Cash Flow ratios place well within the industry

- Expected EPS growth of 10.39% and revenue growth of 8.18% give basic support

For dividend investors, valuation thoughts go further than simple multiples to include the sustainability and growth possibility of payouts. ResMed's mix of fair industry-relative valuation and good growth prospects backs its case as a dividend growth candidate instead of a deep value choice.

The complete fundamental study supporting these observations can be examined in detail through ResMed's full fundamental report.

Investors looking for more candidates that fit similar dividend quality rules can look at the Best Dividend Stocks screen for more investment ideas that balance dividend strength with profitability and financial condition.

Disclaimer: This analysis is based on current fundamental data and does not constitute investment advice. Investors should conduct their own research and consider their individual financial circumstances before making investment decisions. Past performance does not guarantee future results, and dividend payments are subject to company discretion and business conditions.