Investors looking for chances in the stock market frequently use a structured method to find stocks priced lower than their estimated true worth. One path focuses on finding companies with solid foundations that are also marked down. This process emphasizes a high valuation score, meaning the stock seems low-priced compared to its financial numbers, and also calls for acceptable ratings in earnings strength, balance sheet condition, and expansion. The aim is to locate firms that are not just low-priced, but low-priced without a clear cause, possibly providing a buffer for careful investors. Qorvo Inc (NASDAQ:QRVO) comes from this type of process as a name that deserves more examination.

Examining Valuation

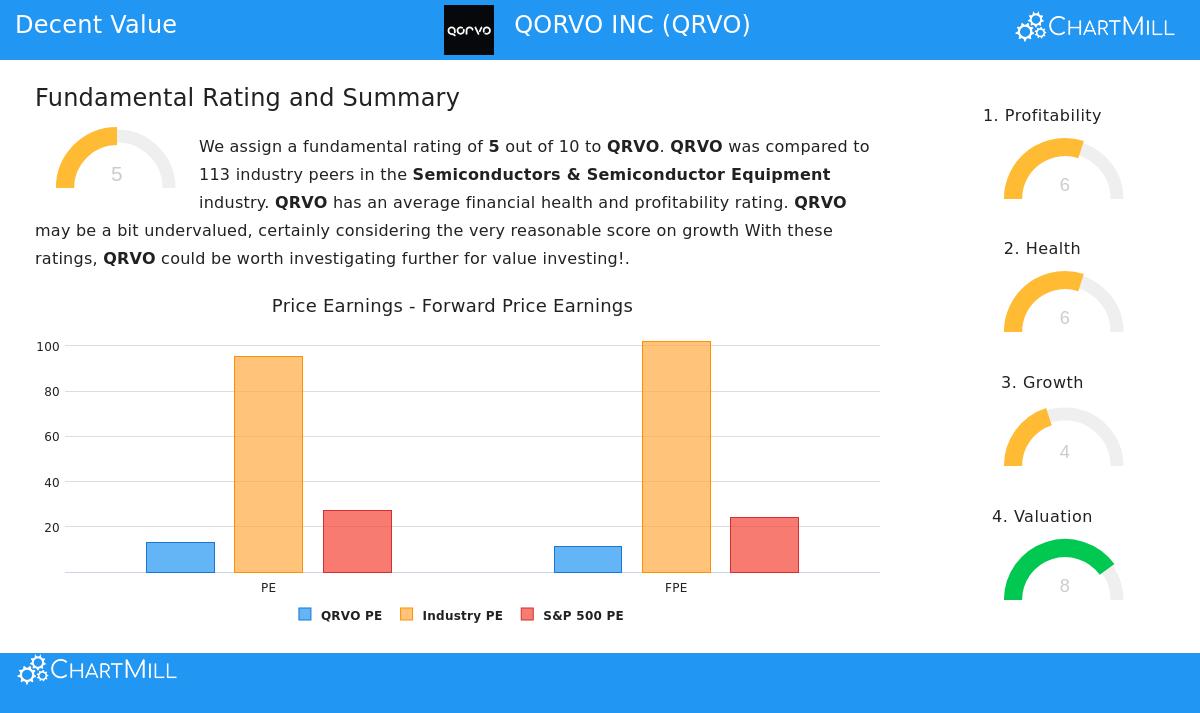

The central idea of value investing is buying an asset for less than its estimated value. Qorvo’s most notable feature is its price assessment, which gets an 8 out of 10 in ChartMill’s fundamental review. This rating comes from measures that look good next to both its sector and the wider market.

- Price-to-Earnings (P/E): At 13.12, QRVO’s P/E ratio is lower than 95.58% of similar companies in the Semiconductors & Semiconductor Equipment sector. It is also much lower than the present S&P 500 average of 27.32.

- Forward P/E: The view stays positive looking forward, with a Price/Forward Earnings ratio of 11.37. This is lower than 96.46% of sector rivals and, again, notably under the S&P 500 forward average.

- Cash Flow & EBITDA Multiples: The stock also looks low-priced based on cash flow and operating earnings, with its Enterprise Value/EBITDA and Price/Free Cash Flow ratios rated higher than about 94% of the sector.

For an investor focused on value, these numbers imply the market might be setting too low a price on Qorvo’s earnings capacity. The company’s sensible P/E ratios, particularly within a sector known for high multiples, give a numerical basis for the low-price argument. You can see the complete details in the detailed fundamental report for QRVO.

Reviewing Balance Sheet Condition and Earnings Strength

A low-priced stock is only a sound investment if the company is financially secure and able to produce earnings. This is where the "margin of safety" idea is vital; good fundamentals lower the chance that the low price is a lasting "value trap." Qorvo gets a health score of 6 and a profitability score of 6, pointing to a middling but steady standing.

- Balance Sheet Condition (Score: 6): The company shows sufficient liquidity, with a Current Ratio of 2.95 and a Quick Ratio of 2.20, meaning no near-term payment worries. Its Debt-to-Free Cash Flow ratio of 2.90 is good, indicating it could clear all its debt in less than three years using its cash flow, a mark of financial strength. While its Altman-Z score and Debt/Equity ratio are points to observe, the general liquidity and debt payment measures back a stable financial foundation.

- Earnings Strength (Score: 6): Qorvo is reliably profitable, with positive earnings and operating cash flow in recent years. Its Return on Invested Capital (ROIC) of 6.49% is better than 72.57% of its sector peers and is now above its three-year average, a good direction. Margins, however, have faced some strain. The Operating Margin of 11.86% is good compared to peers but has dropped lately, a detail for investors to note.

These scores are important for the value method. They verify that Qorvo is not a financially troubled company being sold off for basic reasons. The acceptable condition and earnings strength provide the "base" that helps support the investment case beyond the simple low-P/E point.

Expansion Potential and the Full View

Strict value choices can sometimes miss expansion, but the preferred find offers a mix of low price and a believable expansion path. Qorvo’s expansion score is a 4, showing a varied but getting better situation.

- Past Results: The company has encountered difficulties, with Revenue falling 7.22% and EPS dropping a little over the last year.

- Future Forecasts: The view ahead is more encouraging. Analysts project EPS to increase by 9% each year in the next few years, with Revenue growth rising to an estimated 3.72% per year. This predicted pickup in both earnings and sales growth is a key good point mentioned in the review.

For a value investor, this path is significant. It suggests the present low price might not include the expected earnings improvement. The method looks for low valuation, and if Qorvo can meet these expansion projections while keeping its balance sheet condition, the difference between its market price and estimated true value could narrow.

Summary

Qorvo Inc shows an example of using a structured value filter. It has a clearly low price assessment next to its sector, which is the main draw. This is joined with middling but sufficient scores in balance sheet condition and earnings strength, implying the business is stable enough to justify the investment. While past expansion has been difficult, forecasts for a return to earnings growth give a reason for the low-price argument. It represents the kind of chance value investors look for: a company with sound foundations trading at a price that seems to underestimate its future possibility.

This review of QRVO was generated from a methodical hunt for acceptable value stocks. Investors wanting to find other firms that fit similar standards of good valuation, acceptable profitability, condition, and expansion can look further using the Decent Value Stocks screen on ChartMill.

Disclaimer: This article is for information only and is not financial guidance, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own study and think about their personal money situation and risk comfort before making any investment choices.