For investors looking for a dependable source of passive income, a disciplined screening process is needed to separate solid dividend payers from possible value traps. One useful method involves filtering for stocks that not only have a high dividend rating, pointing to good yield, growth, and sustainability, but also show acceptable basic profitability and financial condition. This detailed method helps find companies with the business strength to keep and possibly raise their payments over time, rather than those presenting high yields because of a falling share price or weak finances.

PPG Industries Inc (NYSE:PPG), a worldwide head in paints, coatings, and specialty materials, comes up as a candidate from this kind of screening process. The company’s basic profile suggests it deserves more examination from income-focused investors.

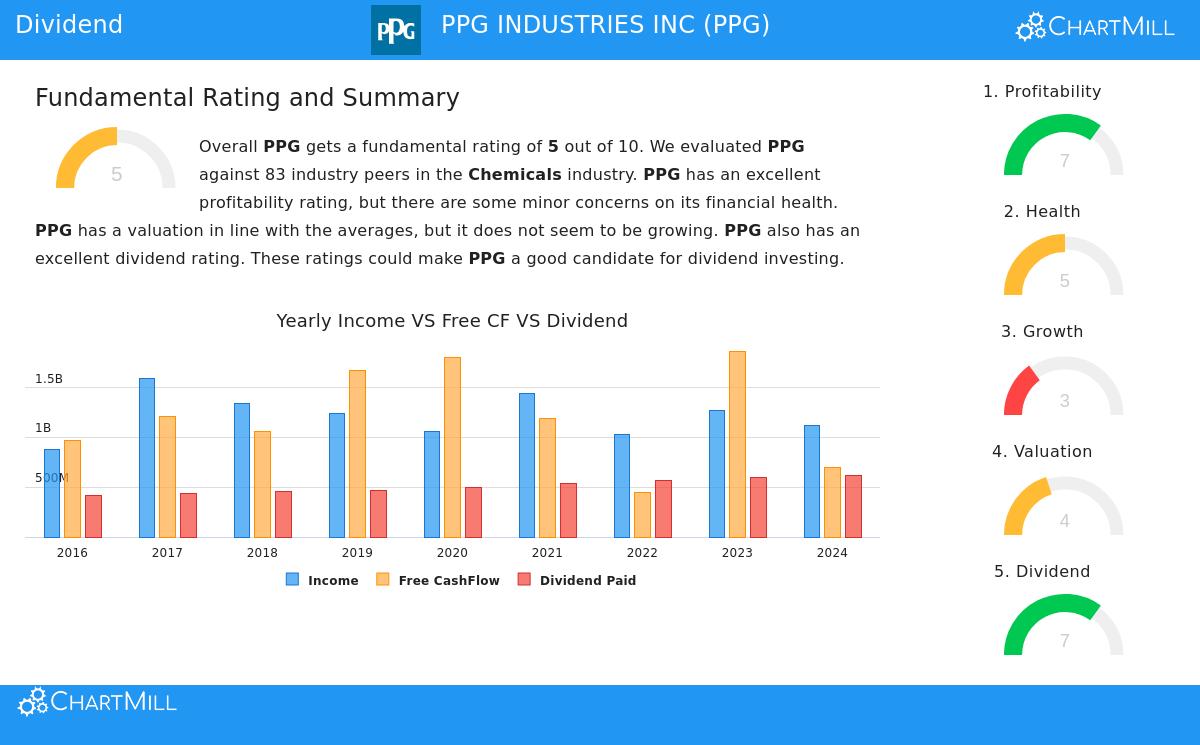

Dividend Profile: A Track Record of Reliability

The main attraction for dividend investors is PPG’s steady and increasing distribution to shareholders. The company gets a good Dividend Rating of 7 out of 10, backed by several important factors:

- Steady and Growing Payout: PPG has raised its dividend for at least 10 straight years, indicating a management dedication to giving capital back to shareholders. The dividend has increased at a good yearly rate of about 6.2% over the last five years.

- Competitive Yield: The stock now provides a dividend yield of 2.58%. This is more than the industry average of 2.23% and clearly higher than the present S&P 500 yield of near 1.82%, offering an above-market income stream.

- Future Sustainability: A key point is whether dividend growth can persist. Analysts expect PPG’s earnings per share (EPS) to increase by about 9.4% each year in the near future, which is faster than the recent dividend growth rate. This implies the company has the ability to keep financing dividend raises without pressuring its finances.

However, a point of care is needed regarding the payout ratio, which is at 62.85% of earnings. While this is not a dangerously high figure, it shows that a large part of profit is being paid out, allowing less flexibility if earnings were to fall suddenly. Investors should watch this measure, though the expected earnings growth offers some protection.

Basic Strength: Profitability and Financial Condition

A lasting dividend is only as good as the business supporting it. PPG’s screening results are strengthened by acceptable scores in profitability and financial condition, which are important for the long-term strength of its payment.

Profitability (Rating: 7/10): PPG shows solid operational efficiency. The company’s return on equity (ROE) of 12.8% and return on invested capital (ROIC) of 9.4% are better than most of its competitors in the chemicals industry. Also, its gross margin of over 40% is one of the top in the sector. This high level of profitability gives the necessary cash flow to pay for dividends, put money back into the business, and handle debt.

Financial Condition (Rating: 5/10): The health rating presents a varied but generally okay picture. On the good side, PPG has a firm Altman-Z score of 3.6, showing low short-term bankruptcy risk and placing well within its industry. The company’s debt-to-equity ratio of 0.76 matches industry standards.

The main worries relate to liquidity and cash flow compared to debt. The current and quick ratios are a bit low next to peers, and it would take about 10 years of free cash flow to settle all existing debt. While not an emergency, these elements suggest investors should observe the company’s balance sheet management, particularly when interest rates are higher.

Valuation and Growth Setting

From a valuation view, PPG seems fairly priced. Its price-to-earnings (P/E) ratio of 15 is notably less expensive than the wider S&P 500 and looks good next to its industry peers. This valuation gives some safety and adds to its good dividend yield.

Growth has been slow lately, with a small decrease in EPS over the past year. However, the forward view is better, with analyst estimates indicating a return to mid-single-digit revenue growth and high-single-digit EPS growth. This expected gain is a good sign for the dividend’s future path.

A Candidate for More Study

For dividend investors using a screen for quality and yield, PPG Industries offers a strong example. It joins a ten-year history of dividend growth with a yield that exceeds the market, all backed by good basic profitability. While the higher payout ratio and average liquidity measures need watching, the company’s industry-top margins, fair valuation, and positive earnings outlook help balance these worries.

This review of PPG came from a systematic screening process. If you want to examine other stocks that fit similar standards for dividend strength, profitability, and financial condition, you can see the complete screen results here.

Disclaimer: This article is for information only and does not make up investment advice, a suggestion, or an offer to buy or sell any security. The basic data and ratings are from past performance and analyst estimates, which are not promises of future results. Investors should do their own complete research and think about their personal money situation before making any investment choice. You can see the detailed basic analysis report for PPG here.