The search for undervalued companies with good basic business qualities is a key part of value investing. This method finds stocks selling for less than their true worth, often shown by solid profit and money strength, but not seen by most of the market. One way to find these chances is by using a "Decent Value" screen, which looks for companies with high valuation scores, meaning they are priced low compared to their money numbers, while also having acceptable marks in growth, strength, and profit. This method helps find stocks that are not only low-priced but are supported by workable, improving businesses, possibly giving a safety net for investors. A recent screen has pointed to Pilgrim's Pride Corp (NASDAQ:PPC) as a candidate needing more study.

Valuation Measures

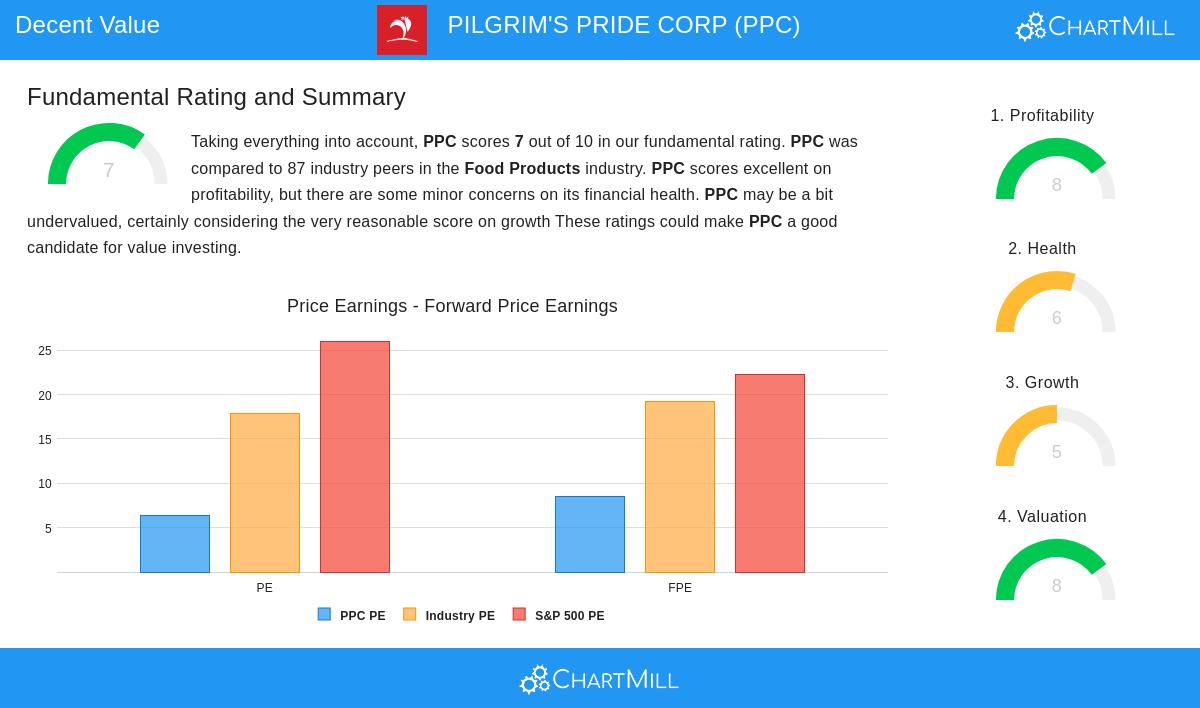

A main draw for value investors is finding a company trading well below its true worth, and PPC's valuation measures are strong. The stock seems low-cost across several important ratios, which is exactly what value screens are made to find. A low price gives that important cushion, or safety net, that Benjamin Graham stressed.

- Price-to-Earnings (P/E) Ratio: PPC's P/E ratio of 6.34 is much lower than the industry average of 17.91 and the S&P 500 average of 26.03. This shows investors are paying less for each dollar of profit compared to similar companies and the wider market.

- Forward P/E Ratio: With a forward P/E of 8.54, the company stays inexpensive relative to future profit guesses, trading below 95% of its industry rivals.

- Enterprise Value to EBITDA: This measure, which includes debt, also suggests a low price, with PPC being less costly than 85% of its industry peers.

Profitability Strength

While a low price is key, value investing needs the company to also be basically profitable. A low P/E ratio is not important if the company's profits are unsteady or falling. PPC shows good profitability, suggesting its low price is not a sign of a poor business but possibly a market mistake.

- Return on Equity (ROE): An ROE of 34.73% is excellent, doing better than almost 99% of industry peers. This points to very good use of shareholder money.

- Return on Invested Capital (ROIC): At 19.90%, the ROIC is also solid, beating 96% of the industry and showing a rise from its three-year average.

- Profit and Operating Margins: The company's profit margin of 6.70% and operating margin of 9.53% are good and have shown betterment in recent years, indicating effective cost management and operational soundness.

Financial Health Check

Financial health is vital for a value investment because it lowers the chance of the "value trap"—a case where a low-priced stock becomes cheaper due to basic money weakness. A healthy company can get through economic drops and keep working until the market sees its true value.

- Solvency: PPC has an Altman-Z score of 3.72, which points to a low short-term chance of money trouble and is better than 79% of its peers. Its Debt-to-Free-Cash-Flow ratio of 3.73 is also acceptable.

- Liquidity Concerns: The study does note a point of care with a Quick Ratio of 0.78, which suggests the company could have issues meeting its immediate debts without selling goods on hand. However, its overall Current Ratio of 1.51 is seen as sufficient.

Growth and Dividend Profile

Value investments are not without growth; in fact, a mix of value and growth can be effective. Also, a dividend can give investors income while they wait for the market to reprice the stock.

- Past Growth: PPC has a solid history, with Earnings Per Share (EPS) growing by a notable 26.18% over the past year and by an average of 27.16% each year in recent years.

- Future Guesses: Experts predict a drop in EPS growth in the next few years, which may partly account for the stock's low price. This is a point investors must consider next to the company's solid past performance and profitability.

- Dividend Yield: The company gives a large dividend yield. While the lasting-power score is low because of a short dividend history, the high present yield is an important point for total return possibility.

In summary, Pilgrim's Pride Corp presents a profile that matches key value investing ideas: it is low-priced by the numbers, very profitable, and financially healthy enough to suggest it is not a value trap. Its solid past growth and high dividend yield add more parts to the investment case. For investors using a value-focused method, PPC represents a strong candidate for more detailed study.

This study was based on the detailed Fundamental Analysis Report for PPC.

If you are interested in finding other companies that match this "Decent Value" profile, you can find more screening results here.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any securities. The content presented is based on data believed to be reliable but is not guaranteed. All investing involves risk, including the possible loss of principal. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions.