Four straight weeks of losses, oil prices surging past $112 a barrel, gold posting its worst weekly drop in over four decades, and a co-founder of one of the most talked-about AI hardware companies arrested for smuggling chips to China.

Friday, March 20 was anything but dull on Wall Street.

The Week That Keeps Getting Worse

This was a rough week, and Friday's session made sure we'd feel it heading into the weekend.

The Dow Jones closed down 1 percent and the Nasdaq gave back 2 percent, capping what was already a difficult stretch. Selling pressure intensified during the final trading hour in what turned into a broad-based, risk-off exodus.

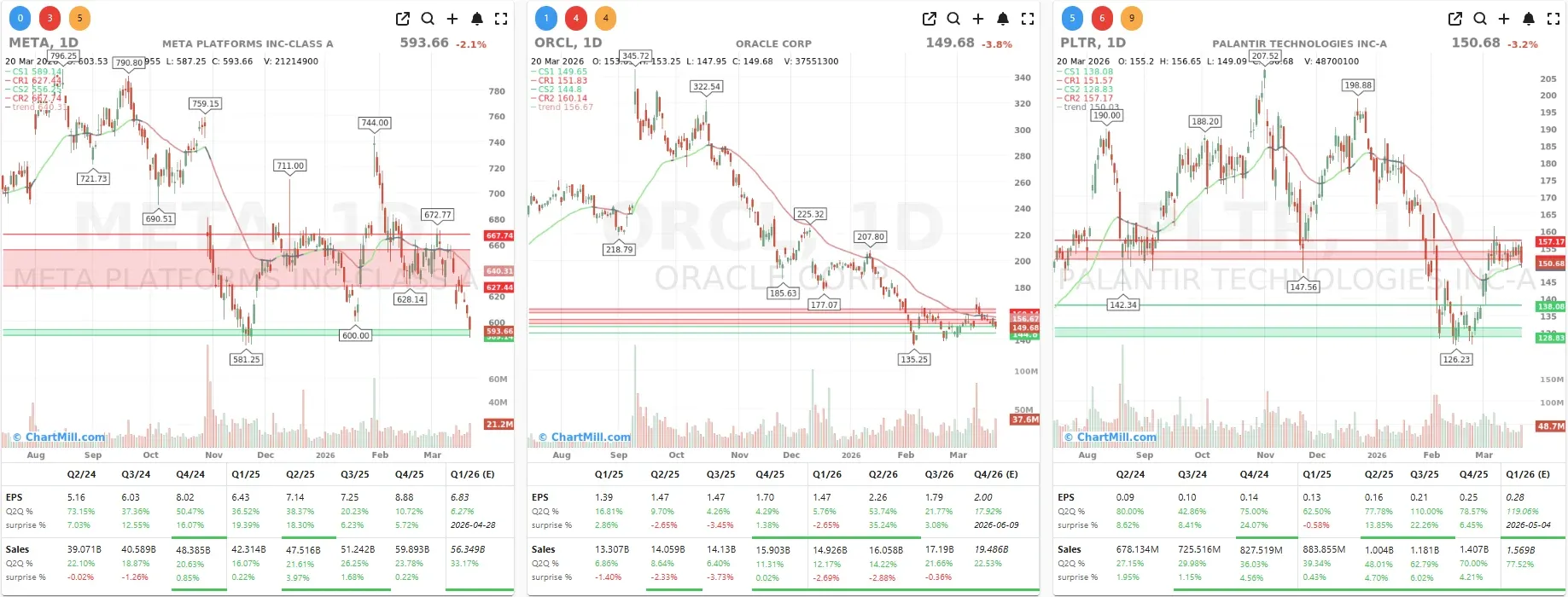

What had started as a debate about how many rate cuts the Federal Reserve would deliver this year has now flipped entirely, markets are pricing in a 50% probability that the Fed will actually raise rates by October. That's a seismic shift in expectations, and it's showing up everywhere.

The US 10-year Treasury yield shot up 14 basis points to 4.39%, delivering a clear signal of how dramatically sentiment on monetary policy has changed.

Rate-sensitive technology names bore the brunt of the repricing, with the likes of Meta Platforms (META | -2.15% | $593.66), Oracle (ORCL | -3.76% | $149.68), and Palantir (PLTR | -3.21% | $150.68) selling off sharply.

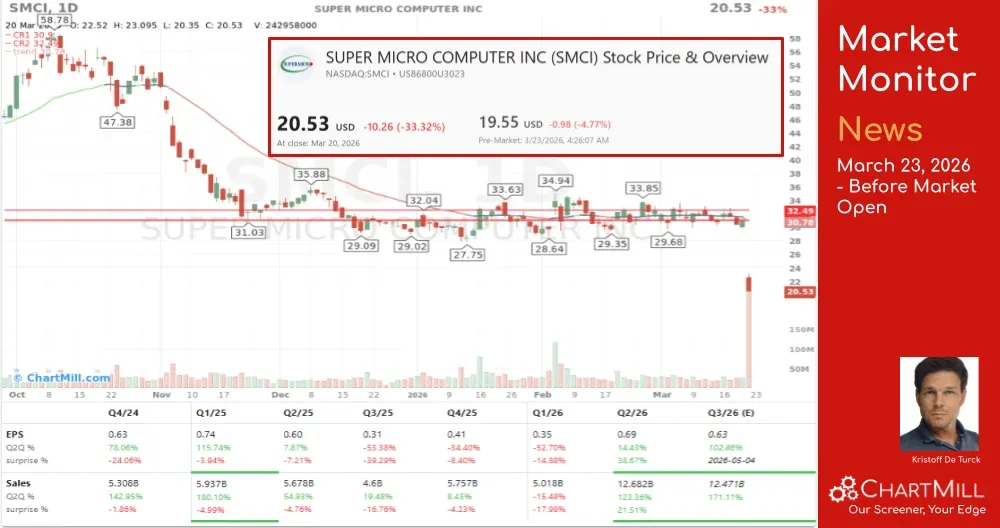

SMCI: A Third of Its Value, Gone in One Day

If there was one moment on Friday that crystallized the madness of the session, it was the collapse of Super Micro Computer (SMCI | -33.32% | $20.53).

Shares plummeted approximately 33% after the US Department of Justice unsealed charges alleging a multi-year scheme to illegally divert around $2.5 billion in AI servers - equipped with restricted Nvidia GPUs - to China, violating US export controls.

Among those charged was co-founder and board member Yih-Shyan "Wally" Liaw, who subsequently resigned from the company's board effective immediately.

The company itself was not named as a defendant, and confirmed it had cooperated with investigators, but in situations like this, the association damage is often just as painful as the legal exposure itself. Argus downgraded the stock to Hold from Buy following the indictment.

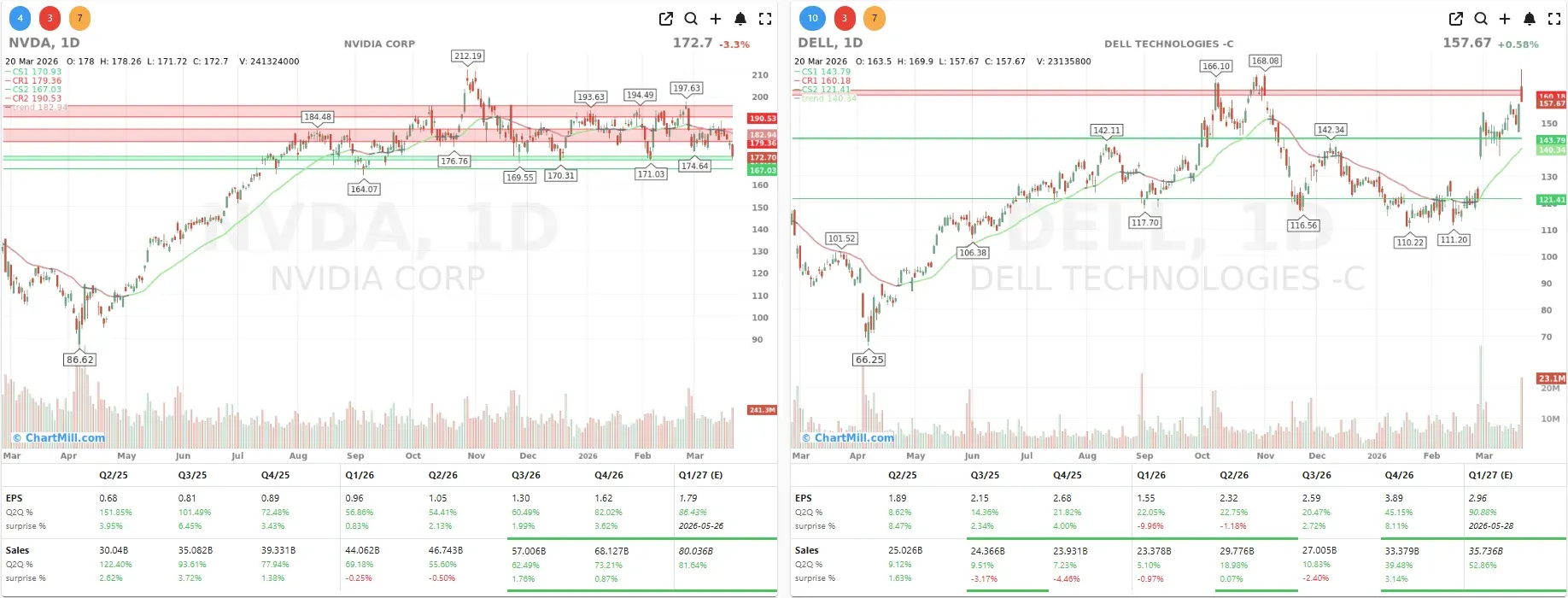

The collateral damage extended to Nvidia (NVDA | -3.28% | $172.70), given that it is one of Super Micro's primary chip suppliers, though no suspicion has been cast on the chipmaker itself.

Not everyone suffered, though. Dell Technologies (DELL | +0.58% | $157.67) experienced a surge in demand for its AI servers, driven by issues at rival Super Micro.

The stock briefly surged as much as 9% at the open before retreating with the broader market during the session, proof that in the AI infrastructure race, one company's crisis can be another's opportunity.

Dell's position as a clean, credible alternative for enterprises nervous about reputational exposure looks increasingly compelling.

The Middle East Is Rewriting the Inflation Script

The macro backdrop continues to deteriorate, and I think investors need to take this seriously. The further escalation of the US-Iran conflict triggered a fresh wave of inflation fears that are now casting a shadow over the global economy.

Oil prices briefly touched $119 a barrel on Thursday, a level that reactivates fears of 1970s-style energy-driven inflation cycles.

On Friday, a barrel of WTI crude oil rose a further 2.3%, while Brent climbed 3.3% to $112.19. Both benchmarks have now risen more than 40% since the outbreak of the conflict.

Adding to Friday's volatility was a Reuters report that Iraq invoked "force majeure" on all oil fields operated by foreign companies, temporarily suspending its delivery obligations without legal liability. That headline hit mid-session and accelerated the afternoon selloff.

The weekend brought an even sharper escalation: Trump issued a 48-hour ultimatum to Iran, threatening to attack and destroy electricity plants if the Strait of Hormuz is not fully reopened.

Iran's military command responded with threats of its own against US and Israeli infrastructure across the region. Regardless of how one reads the geopolitics, the message for markets is unambiguous: energy prices aren't going down anytime soon.

Gold's Historic Stumble

Here's something I did not expect to write this week.

Gold - the traditional safe-haven asset in times of geopolitical turmoil - is on track for its worst weekly performance since 1983, down nearly 9% to around $4,575 per troy ounce.

The logic is straightforward but counterintuitive: surging energy prices are feeding rate hike speculation, and higher rates make non-yielding assets like gold less attractive relative to bonds.

The irony of a geopolitical crisis actually hurting gold is a powerful reminder that macro dynamics can override historical correlations in a hurry.

Earnings Bright Spots: Space, Logistics, and EVs

It wasn't all gloom.

A few earnings reports managed to cut through the noise.

The commercial space sector stole some headlines. Planet Labs (PL | +25.48% | $33.83) surged on a strong quarterly report, the company posted record FY26 revenue of $307.7 million and a record backlog, while guiding for FY27 growth of approximately 39% with improving profitability.

Wedbush raised its price target to $40 and maintained its Outperform rating.

Sector peer York Space Systems (YSS | +19.17 | $21.07) also rallied sharply, suggesting the commercial space sector is starting to attract serious investor interest.

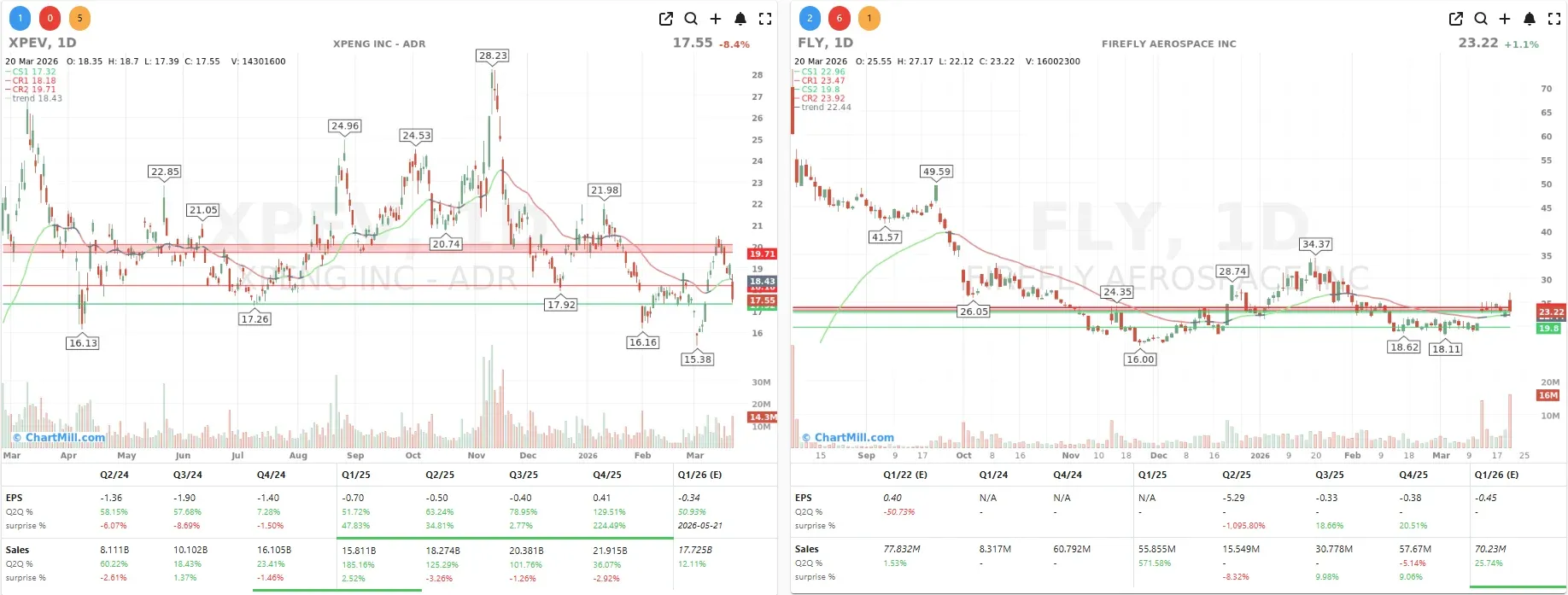

Firefly Aerospace (FLY | +1.13% | $23.22) added to the sector's momentum with better-than-expected revenue for Q4.

On the EV front, XPeng (XPEV | -8.36% | $17.55) delivered a mixed bag. The Chinese automaker posted its first-ever quarterly profit in Q4 2025, a genuine milestone.

But guidance for Q1 2026 revenue of 12.2–13.28 billion RMB fell well short of market expectations of 15.01 billion RMB, sparking renewed concerns about XPeng's growth trajectory.

In a market this risk-averse, a guidance miss of that magnitude gets punished quickly.

Quadruple Witching Adds Fuel to the Fire

Worth noting as context: Friday marked the quarterly "quadruple witching" expiration of stock options, index options, index futures, and individual stock futures, an event that typically generates elevated trading volumes and sharper intraday swings as investors rebalance or unwind positions.

This mechanical factor amplified the moves we saw across the board, particularly in the final hour of trading.

My Take

The combination of a genuine geopolitical crisis, a policy narrative that has swung 180 degrees in a matter of weeks, and headline corporate scandals makes for a deeply uncomfortable environment.

The SMCI implosion is particularly worth watching, not because of the legal proceedings themselves, but because of what it says about how the AI supply chain is under scrutiny.

Any company relying heavily on restricted GPU supply chains should expect elevated regulatory attention going forward.

With Trump's 48-hour Hormuz ultimatum and Iran giving no indication of backing down, the week ahead could be volatile before it even begins. Defensive positioning and energy exposure warrant a fresh look. Stay sharp.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.