The search for quality companies trading at reasonable prices is a foundation of many long-term investment methods. One well-known method is the GARP, or "Growth At a Reasonable Price," strategy, which aims to find businesses with steady and maintainable earnings growth that are not overpriced by the market. This method steers clear of the extremes of pure, high-growth stocks and deep-value turnarounds, instead concentrating on financially sound companies whose stock prices have not yet completely matched their growth prospects. A standard model for this style of investing was made famous by renowned fund manager Peter Lynch, whose standards highlight profitable growth, sound financial condition, and good value.

One company that recently appeared through a filter built on these Lynch-influenced standards is ONESPAN INC (NASDAQ:OSPN). The Boston-based company supplies digital security and identity verification products, functioning in two parts: Security Solutions and Digital Agreements. Its goods are made to protect online transactions, mobile applications, and digital signing processes, serving a worldwide demand for better cybersecurity and compliance.

Match with GARP and Lynch-Style Standards

The filter uses particular checks to identify companies that show the signs of maintainable growth at a reasonable price. A detailed examination of OneSpan’s main numbers shows why it passed this first check.

- Maintainable Earnings Growth: A central Lynch principle is to find companies expanding at a consistent, manageable speed, usually between 15% and 30% each year. OneSpan’s earnings per share (EPS) have increased at an average yearly rate of about 19.4% over the last five years. This fits inside the target zone, indicating a history of growth that is solid yet not so rapid as to be possibly unstable.

- Good Value Balanced with Growth: The Price/Earnings to Growth (PEG) ratio is a key number for GARP investors, as it frames a company’s price relative to its growth speed. A PEG ratio at or under 1.0 is often seen as good. OneSpan’s PEG ratio, calculated from its past five-year growth, is a very low 0.46. This shows the market may be pricing the company’s shares cautiously relative to its historical earnings growth path.

- High Profitability and Financial Condition: Strong returns on equity (ROE) and a clear balance sheet are foundations of Lynch’s method, confirming a company is both profitable and durable. OneSpan does very well here, with an ROE of 24.4%, much higher than the 15% level often wanted. Also, the company has no debt, leading to a Debt/Equity ratio of 0. This outstanding financial situation offers notable stability and operating freedom.

- Sufficient Short-Term Cash Flow: To confirm a company can meet its immediate responsibilities, Lynch preferred a sound current ratio. OneSpan’s current ratio of 1.75 shows it has more than enough short-term assets to cover its short-term debts, passing this test of financial care.

Fundamental Condition Review: A High-Level Summary

A wider look at OneSpan’s fundamental picture supports the first filtering outcomes. The company gets a good total fundamental score, with specific high points in two areas:

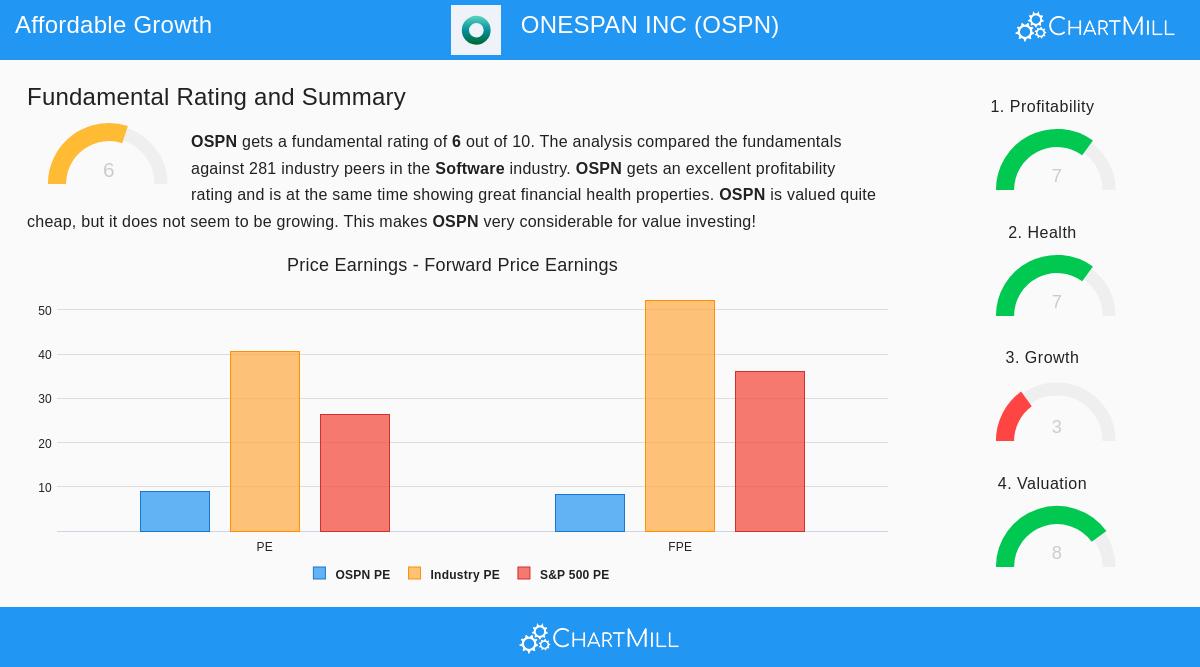

- Profitability and Value are High Points: OneSpan’s profitability numbers are sound, with profit, operating, and gross margins all displaying gain and scoring well within the competitive software field. Paired with this is a very low price; its Price-to-Earnings and Price-to-Forward-Earnings ratios are much lower than both industry competitors and the wider S&P 500 average.

- Financial Condition is Sound: The company’s ideal debt-free balance sheet and good Altman-Z score highlight a very solid financial standing with little bankruptcy danger. This offers a firm base for long-term function.

- The Growth Consideration: The main area for investor examination is future growth. While past EPS growth has been sound, recent income patterns have been level to slightly down, and analyst forecasts predict only small single-digit growth in both income and earnings over the next few years. For a GARP investor, knowing the causes for this predicted growth slowdown is a key part of the study process.

For a complete look at these numbers, you can see the full fundamental analysis report for OSPN.

Is OneSpan a Match for the Long-Term GARP Portfolio?

OneSpan offers an interesting example for investors using a Growth At a Reasonable Price method. It meets several important standards: a history of good earnings growth, first-rate profitability, excellent financial condition with no debt, and a price that seems modest. The low PEG ratio indicates the market may not be completely recognizing its historical growth record. For a long-term investor, these qualities build a solid base.

However, the method also needs belief in a company’s future. The main question for a possible investor is whether OneSpan can speed up its growth again. The company works in the necessary and growing area of digital security, which may offer a long-term benefit. Complete study would require evaluating its competitive standing, product development, and management’s plan to get back to more solid income growth.

Interested in locating other companies that meet this careful investment method? You can run the filter yourself and see the newest outcomes by going to the Peter Lynch Strategy stock screener.

,

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or an offer or request to buy or sell any securities. The information shown is based on supplied data and should not be the only base for any investment choice. Investors should do their own separate study and talk with a qualified financial advisor before making any investment.